- Providing world class service and value for employee benefit group plans since 1987

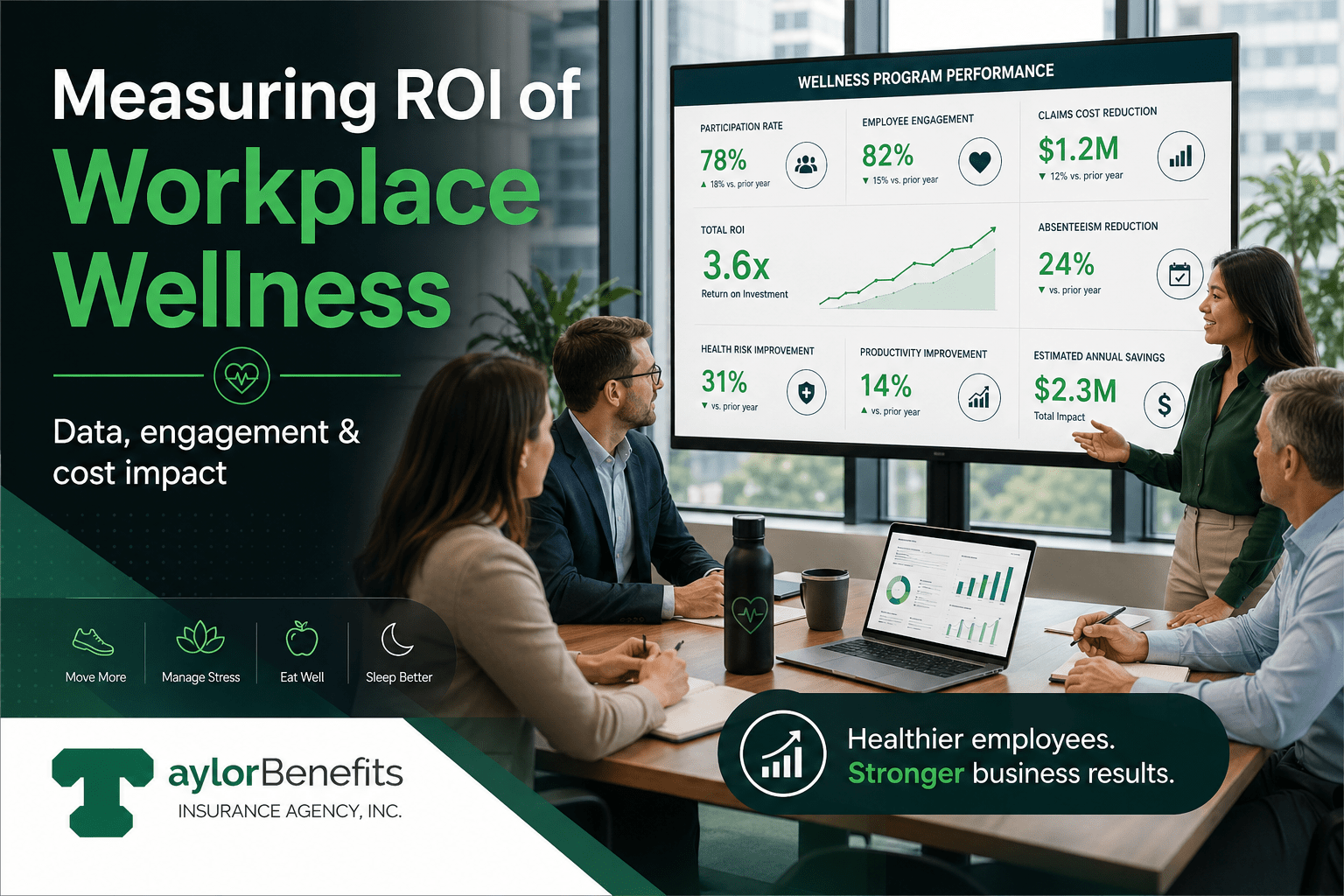

The conversation about workplace wellness ROI has matured significantly over the past decade, and not in a way that flatters most existing programs. The early era of wellness — anchored in claims that every dollar invested returned three to six dollars in healthcare savings — produced numbers that didn't survive serious academic scrutiny. The peer-reviewed literature, including landmark studies from the University of Chicago and Harvard, has consistently found that the dramatic ROI claims of the 2000s and early

Read Full Article Here

The benefits package designed for a salaried knowledge worker behind a laptop fails predictably when delivered to a warehouse associate, a CNA in a long-term care facility, a delivery driver, a construction worker, or a hospitality worker on a variable schedule. The plan structure, the enrollment process, the communication channels, the claims experience, and the assumptions about how employees access care are all built for a workforce that lives on email, has predictable hours, can take a phone

Read Full Article Here

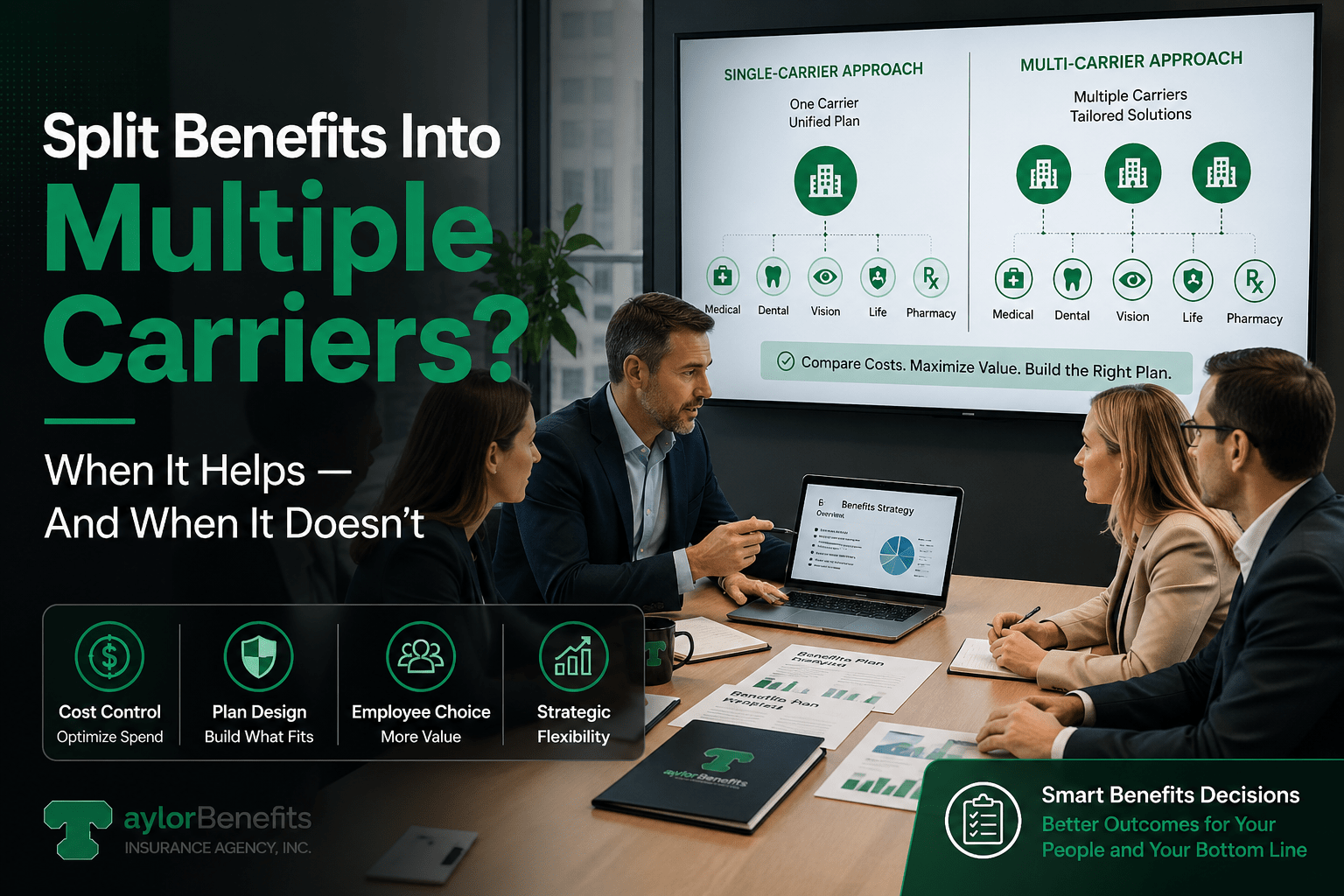

The default assumption among many small and mid-size employers is that bundling all benefits with a single carrier is simpler, cheaper, and easier to manage. The single-carrier model — medical, dental, vision, life, and disability all from the same insurer — has been the standard offering of national carrier sales teams for decades, and the convenience case for it is real. The cost case is less convincing than it appears. The carrier with the most competitive medical pricing in your

Read Full Article Here

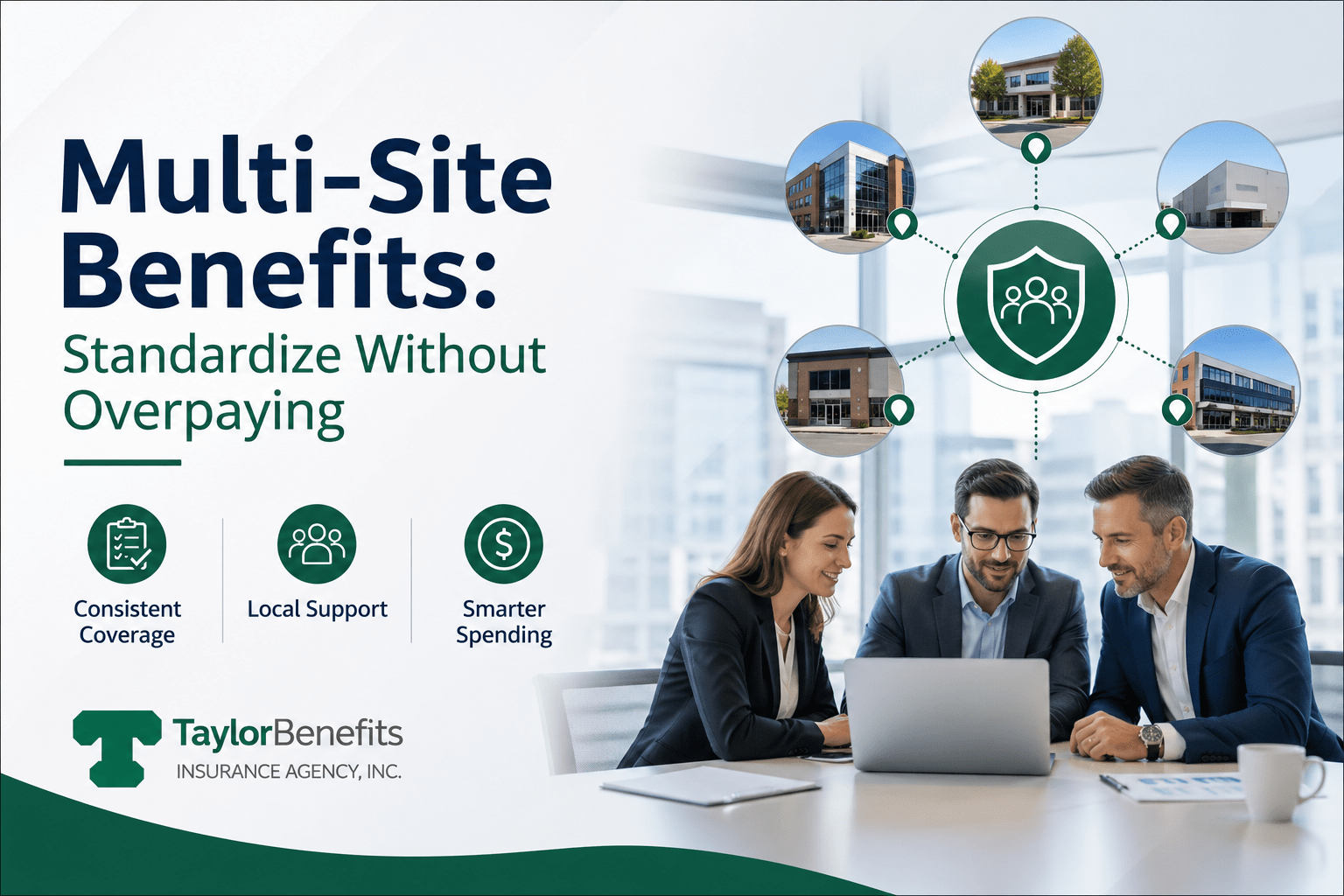

A 350-employee company with locations in Atlanta, Phoenix, Boston, and Denver has a problem that doesn't show up on any single line of the income statement but quietly drives material cost and complexity into the benefits program: every market it operates in has different healthcare pricing, different network adequacy, different state insurance regulations, and different employee expectations about what a competitive benefits package looks like. The HR team wants standardized benefits — for fairness, for

Read Full Article Here

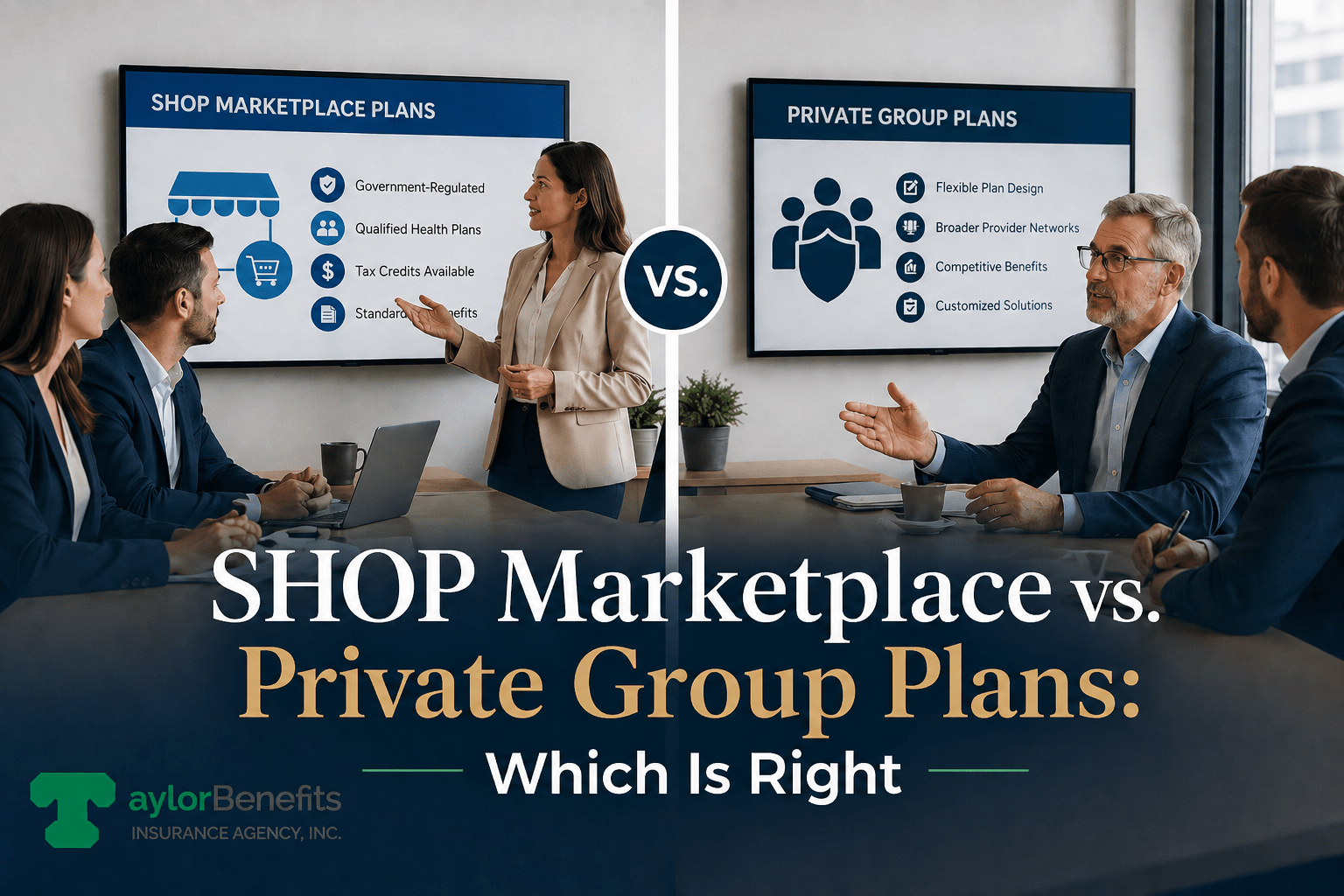

For small employers shopping for group health coverage in 2026, the decision between the Affordable Care Act's Small Business Health Options Program (SHOP) and the private small group market is rarely the first question that comes up — and it should be. The choice between these two purchasing channels affects what carriers you can access, what plans you can offer, whether you qualify for the Small Business Health Care Tax Credit, and how much administrative complexity you'll absorb in

Read Full Article Here

A 25-person software company competing for the same developer talent as a 5,000-person enterprise does not have the same benefits budget. It rarely has the same HR infrastructure, the same carrier leverage, or the same purchasing power at renewal. What it does have — and what larger employers often don't — is flexibility, speed, and the ability to design a benefits package from scratch rather than defend a legacy structure that nobody particularly likes but everyone is afraid to

Read Full Article Here

Most employers receive some version of a claims report from their carrier or TPA at least once a year. A significant number of those reports get reviewed once, briefly, and filed. That's an expensive habit. Claims data is the most direct window into what is actually driving your health plan's costs — not what you budgeted, not what your carrier

Read Full Article Here

The pitch for level-funded health plans is compelling on its face: pay a fixed monthly amount like a fully insured plan, but get access to your claims data, potentially share in the surplus if your employees stay healthy, and avoid the community-rated premium increases that punish well-managed groups on the fully insured market. For the right employer, that pitch is accurate. For the wrong employer, it's a way to take on self-funding risk without fully understanding what that risk means

Read Full Article Here

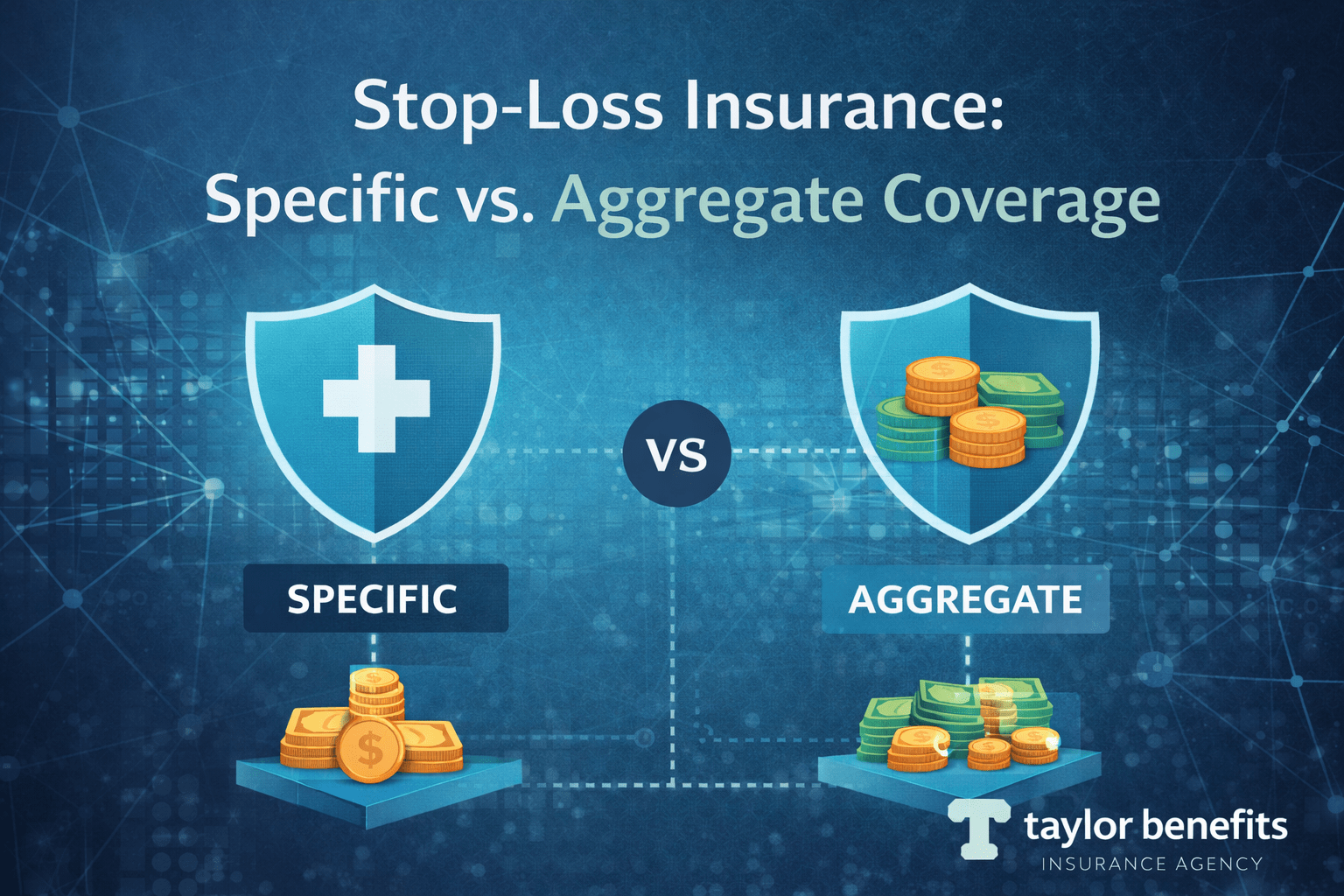

Self-funding a group health plan puts an employer in the position of insurer — responsible for paying claims as they come in, with direct exposure to every high-cost event that hits the plan. For most employers, that exposure is manageable across the predictable middle of the claims distribution: routine office visits, generic prescriptions, standard outpatient procedures. What it is not designed to absorb without protection is the outlier — the premature infant in the NICU for four months, the

Read Full Article Here

Consider a scenario most HR teams have seen play out more than once: an employee shows up to the emergency room with a sinus infection because they didn't know how to find an urgent care clinic in their network. Or a worker schedules an MRI at a hospital outpatient facility — at three times the cost of an independent imaging center — because nobody told them there was a lower-cost alternative. Or a plan member proceeds with a surgery

Read Full Article Here

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066