- Providing world class service and value for employee benefit group plans since 1987

he Patient-Centered Outcomes Research Institute (PCORI) fee is one of the smaller but more consistently mishandled compliance obligations in employer-sponsored health plan administration. It applies to virtually every self-funded and level-funded group health plan, the filing mechanics are specific, the deadlines are fixed, and the fee amount adjusts annually — making it a recurring compliance item that benefits from clear annual review rather than being handled reactively.

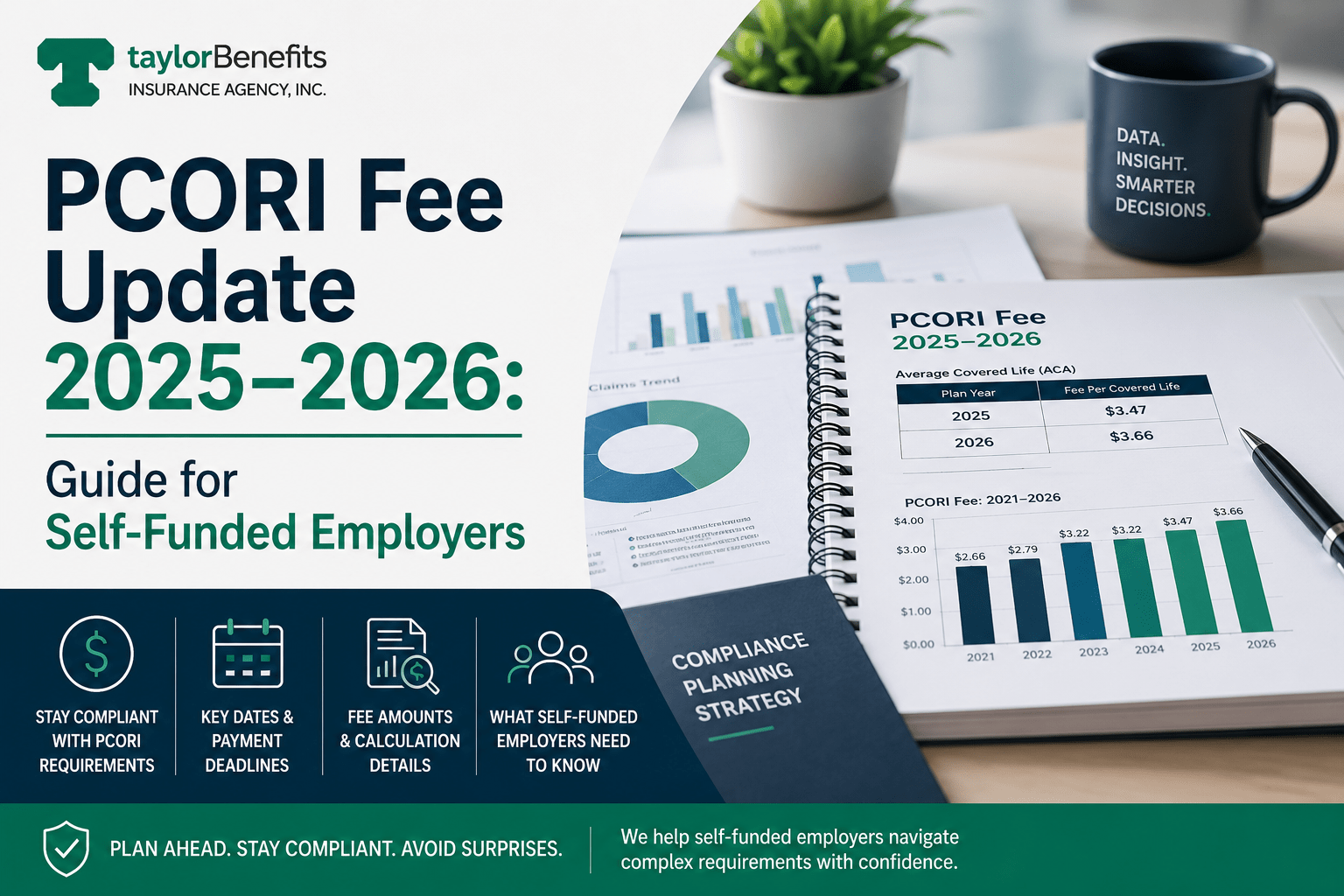

For plan years ending on or after October 1, 2025, and before October 1, 2026, the IRS has updated the PCORI fee to $3.84 per covered life under IRS Notice 2025-61. This is up from $3.47 per covered life for plan years ending October 1, 2024 through September 30, 2025, and represents the largest single-year increase to the fee since its inception. For calendar-year self-funded plans ending December 31, 2025, the $3.84 rate applies, with payment due by July 31, 2026.

This article covers what employers need to know to budget accurately, count correctly, and file on time.

The PCORI fee was established under the Affordable Care Act to fund the Patient-Centered Outcomes Research Institute, a nonprofit organization that conducts comparative clinical effectiveness research — research designed to help patients, clinicians, and employers make better-informed healthcare decisions.

The fee applies to both fully insured and self-funded group health plans, but the responsibility for filing and payment differs:

Fully insured plans: The insurance carrier pays the PCORI fee and typically recovers the cost through premiums. Employers with fully insured medical plans are not responsible for filing Form 720 or remitting the fee directly — though they effectively pay it embedded in their premium.

Self-funded and level-funded plans: The plan sponsor — the employer — is responsible for calculating, reporting, and paying the PCORI fee directly to the IRS each year. This applies to self-funded medical plans, level-funded plans, and Health Reimbursement Arrangements (HRAs).

Exception for integrated HRAs: If an employer sponsors both a self-funded medical plan and an HRA with the same plan sponsor and the same plan year, covered lives are counted only once — there is no separate PCORI fee for the HRA. However, if the employer has a fully insured medical plan combined with a self-funded HRA, the employer must pay the PCORI fee for the HRA separately (using the one-life-per-participant rule for the HRA count only).

The PCORI fee is currently authorized through plan years ending before October 1, 2029, under the Further Consolidated Appropriations Act of 2020, which extended the original ACA fee obligation by 10 years.

The applicable rate depends on when your plan year ends — not when it begins.

| Plan Year End Date | Fee Per Covered Life | Payment Due |

|---|---|---|

| January 1 – September 30, 2025 | $3.47 | July 31, 2025 |

| October 1, 2025 – December 31, 2025 | $3.84 | July 31, 2026 |

| January 1, 2026 – September 30, 2026 | $3.84 | July 31, 2027 |

Short plan years — plans that cover fewer than 12 months due to a plan start or mid-year transition — still owe the full fee based on average covered lives during the short year. There is no pro-rating for short plan years.

Calculating the PCORI fee requires determining the average number of covered lives under the plan during the plan year. The IRS permits three methods for self-insured plans.

Add the total number of lives covered under the plan on each day of the plan year, then divide by the number of days in the plan year. This produces the most precise number but requires daily tracking, which most employers don’t maintain in a readily accessible format.

Add the total lives covered on one date in each quarter of the plan year (e.g., the first day of each quarter, or the same date in each quarter), then divide by four. This is the most commonly used method for employers without daily enrollment tracking systems.

For employers who file Form 5500 for their health plan, a formula based on Form 5500 participant counts can be used. Specifically: add the number of participants at the beginning of the plan year plus the number at the end, then divide by two. This method has specific applicability conditions and produces less precise results than snapshot counting for most plans.

Who counts as a covered life?

The count includes employees, covered dependents, COBRA beneficiaries, and retirees covered under the plan. Every individual covered — not just employees — must be counted.

For HRA-only coverage: When counting covered lives for a standalone HRA (not integrated with a self-funded medical plan), only one covered life is counted per participant, regardless of dependent coverage.

Practical Examples

Practical ExamplesExample 1: Mid-size self-funded employer, calendar year plan

An employer with 300 employees on a self-funded calendar-year plan covering employees and their dependents conducts a snapshot count on the first day of each quarter and determines average covered lives of 485 (including employees and dependents).

Fee calculation: 485 × $3.84 = $1,862.40, due July 31, 2026.

Example 2: Level-funded plan with HRA

An employer with a level-funded medical plan (same plan year as an integrated HRA, same plan sponsor) has average covered lives of 120. Because the HRA shares the same plan year and sponsor as the medical plan, covered lives are counted once.

Fee calculation: 120 × $3.84 = $460.80, due July 31, 2026.

Example 3: Fully insured medical with self-funded HRA

An employer has a fully insured medical plan (carrier pays PCORI for the medical plan) plus a self-funded HRA with 80 enrolled participants. The HRA PCORI obligation falls on the employer, counted using the one-life-per-participant rule (no dependent counting for the HRA).

Fee calculation: 80 × $3.84 = $307.20, due July 31, 2026.

PCORI fees are reported and paid on IRS Form 720, Quarterly Federal Excise Tax Return. Despite the form being a quarterly return, PCORI fees are reported only once per year — on the second quarter Form 720 filing.

Specific lines on Form 720:

Payment mechanics: The PCORI fee can be paid via the IRS Electronic Federal Tax Payment System (EFTPS) or by check with the Form 720 submission.

Filing deadline: Form 720 with PCORI reporting is due by July 31 of the year following the plan year end. For calendar-year plans ending December 31, 2025, the deadline is July 31, 2026.

The PCORI fee is deductible. The IRS permits plan sponsors of self-insured health plans to deduct PCORI fees as an ordinary and necessary business expense under Internal Revenue Code Section 162(a). This partially offsets the net cost.

Several recurring errors in PCORI fee administration produce either overpayment or underpayment — and underpayment creates IRS penalty exposure.

For employers with self-funded or level-funded plans, the PCORI fee obligation should be a standing item on the annual compliance calendar — not a surprise in mid-July.

Build it into the benefits budget. At 300 covered lives (a mid-size employer group including dependents), the 2026 PCORI fee at $3.84 is approximately $1,152 to $1,920 depending on covered life count. At 1,000 covered lives, the fee is approximately $3,840. Not a budget-breaking number, but a predictable one worth planning for.

Assign ownership clearly. Either the employer’s finance team (because it is a tax filing) or the benefits team (because it relates to plan administration) should own the PCORI obligation. The ambiguity between these two functions is a common source of missed filings. Document which team is responsible.

Confirm the TPA’s role. Many TPAs assist with PCORI fee calculation and count verification, but most do not file Form 720 on the employer’s behalf. Confirm specifically whether your TPA is providing calculation support, filing the return, or neither. The employer remains legally responsible regardless of what the TPA does or doesn’t do.

Work with your CPA or tax advisor on the filing. Since Form 720 is a federal excise tax return, CPA involvement in the filing is appropriate and common. Ensure your CPA is aware of the updated rate and deadline well in advance of July 31.

The PCORI fee is not complex, but it requires accurate count methodology, correct rate application, and timely filing. The updated $3.84 rate for plan years ending October 2025 through September 2026 — including the most common calendar-year plan ending December 31, 2025 — is now confirmed under IRS Notice 2025-61, and the July 31, 2026 deadline for calendar-year plans is fixed.

Self-funded and level-funded employers who build the PCORI obligation into their annual compliance calendar, confirm their counting methodology, assign clear filing ownership, and coordinate with their TPA and CPA will handle this straightforwardly. Those who treat it as an afterthought routinely discover the oversight at the point when it creates compliance exposure.

Taylor Benefits Insurance Agency works with self-funded and level-funded employer clients on plan compliance including PCORI fee obligations, annual plan reviews, and coordination with TPAs and tax advisors. Contact our team if you have questions about your plan’s filing obligations

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066