- Providing world class service and value for employee benefit group plans since 1987

The benefits renewal conversation that most employers have with their broker is reactive: the broker presents renewal rates from the incumbent carrier, the employer asks how the rates compare to the prior year, and the conversation focuses on whether to accept the renewal or shop the market. This pattern produces predictable outcomes — modest year-over-year adjustments to a benefits program that drifts slowly from market norms, with limited strategic input beyond carrier negotiation.

A more productive renewal conversation looks different. It is initiated by the employer rather than the broker. It is framed around the employer’s strategic objectives rather than around the carrier’s renewal proposal. And it asks specific questions designed to surface information the broker has but typically doesn’t volunteer — about market alternatives, plan performance, emerging risks, and opportunities the current program may be missing.

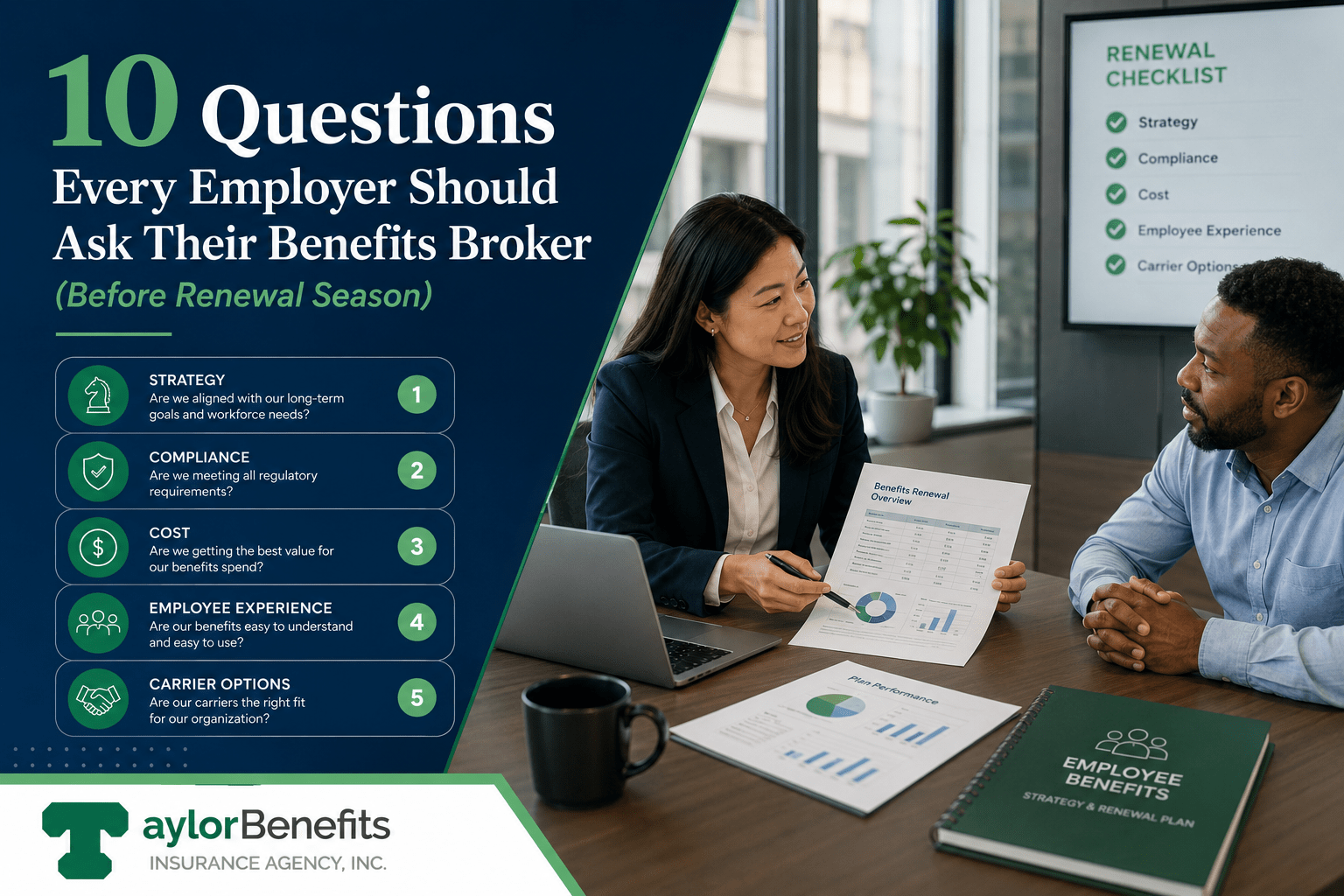

This article covers the 10 questions every employer should ask their benefits broker before renewal season begins. Asking them well in advance — typically 90 to 120 days out — produces materially better outcomes than asking them during the renewal cycle itself.

This is the foundation. Before evaluating any renewal proposal, the employer should understand what the plan’s actual performance has been. The broker should be able to provide:

A broker who can’t produce this analysis — or who produces only a high-level summary without underlying detail — is signaling either limited carrier data access or limited analytical capability. Either is a meaningful concern.

For fully insured employers, claims data access is more limited than for self-funded employers, but most carriers will provide aggregate utilization reports upon broker request. The broker should know what data is available and have requested it.

The incumbent carrier’s renewal rate is one data point. The relevant question is how that rate compares to what other carriers would offer for the same coverage on the same risk profile.

Most brokers will quote the market periodically — typically every two to three years — to validate that the incumbent pricing remains competitive. Employers should specifically ask:

Annual market quoting is generally not necessary and can create disruption costs that exceed potential savings. But market quoting that’s too infrequent allows incumbent pricing to drift from market norms. The right cadence depends on employer size, market dynamics, and incumbent performance.

A capable broker brings strategic input on plan design — not just renewal arithmetic. Questions worth asking include:

Brokers who treat plan design as the employer’s responsibility — rather than as an area where they bring analytical input — provide limited strategic value beyond carrier procurement.

Pharmacy is the fastest-growing component of healthcare costs for most employer plans, driven by specialty drugs, GLP-1 medications, and other high-cost categories. Questions to ask:

For self-funded and level-funded employers above 200 employees, pharmacy strategy is among the highest-leverage areas of cost management. A broker who can’t engage substantively on pharmacy is missing one of the most important conversations for employer cost management.

The regulatory environment for employer benefits is complex and evolving. Specific compliance areas worth confirming:

A broker who has not proactively raised compliance items with the employer in the past 12 months is likely behind on emerging requirements. Compliance reactivity exposes employers to risks that proactive guidance would prevent.

Under CAA 2021 Section 408(b)(2), brokers servicing ERISA-governed group health plans are required to disclose their compensation — both direct and indirect — to plan sponsors. Employers should:

This question often surfaces information employers didn’t have visibility into and can drive compensation structure discussions that benefit the employer. It is also a fiduciary obligation under ERISA — not an optional inquiry.

The benefits administration platform — whether provided by the broker, by a separate vendor, or built into HRIS — significantly affects employee experience and HR efficiency. Questions worth asking:

Platform issues often persist because no one is actively driving resolution. The renewal-season conversation is a natural moment to identify and address them.

Many employer benefits programs include components with substantially below-potential utilization — EAPs at 5%, voluntary benefits with low enrollment, telehealth with limited use, wellness programs without engagement. Questions:

A broker who treats utilization data as a vendor responsibility rather than a strategic concern is missing one of the largest sources of unrealized benefits program value.

Benefits communication often produces the gap between offered benefits and recognized employee value. Questions:

Communication strategy is often outside the broker’s direct execution responsibility, but a capable broker should engage with it as part of overall benefits program effectiveness.

The most important strategic question, and the one most often skipped in renewal conversations. Renewals are best evaluated against a multi-year strategy rather than as isolated annual decisions. Questions:

Brokers who can engage on multi-year strategy bring substantially more value than those who only handle annual renewal mechanics.

Timing matters as much as content. Asking these questions during the renewal cycle — when the broker is focused on processing the renewal — produces shallower engagement than asking them 90 to 120 days in advance.

The practical sequence:

Schedule a strategic review with the broker. Provide these questions in advance so the broker can prepare substantive responses.

Review the responses and identify areas requiring deeper analysis — claims data review, market quoting, plan design evaluation, compliance follow-up, or other strategic work.

Complete strategic analysis and decide on plan design and structural decisions to inform the renewal process.

Execute the renewal with carrier negotiation informed by the strategic decisions already made.

Document the strategic decisions, set objectives for the next year, and schedule the corresponding strategic review 120 days before the next renewal.

This cadence converts renewal from a transactional event into a strategic discipline. The questions are the structural starting point; the multi-year benefit comes from making the conversation routine.

How the broker responds to these questions reveals a great deal about the relationship’s strategic value.

Brokers who engage substantively across all 10 questions — bringing data, analysis, recommendations, and multi-year perspective — are operating as strategic advisors. Brokers who can engage on some questions but not others have gaps that may or may not be material depending on what matters most to the employer. Brokers who consistently treat these questions as outside their scope are operating as transactional intermediaries.

None of these patterns is inherently wrong. Some employers want strategic advisory relationships; others want efficient transactional intermediaries. The mismatch between what the employer needs and what the broker provides is the problem, not either model in isolation.

For employers whose broker relationship is not delivering strategic value at the level the benefits program warrants, the response is either to elevate the relationship — sharing these questions and the expectation of substantive engagement — or to consider whether a different broker would better fit the strategic role.

The renewal conversation is the most important benefits decision moment of the year. Treating it as a transactional event focused on rate negotiation captures a fraction of its potential value. Treating it as a strategic discipline anchored in substantive questions and multi-year perspective converts it into one of the most leveraged moments in benefits program management.

The 10 questions in this article are not exotic — they are basic strategic questions that capable brokers should be prepared to engage with. Asking them deliberately, in advance, and across multiple years produces better benefits outcomes than the reactive renewal conversation that most employers default to.

Taylor Benefits Insurance Agency operates as a strategic advisor to employer clients, engaging substantively on the questions in this article as part of standard renewal preparation. If your current broker relationship is not delivering this level of strategic engagement, contact our team for a conversation about what a different relationship could look like.

Broker compensation disclosure requirements referenced in this article are governed by ERISA Section 408(b)(2) as amended by the Consolidated Appropriations Act of 2021.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066