- Providing world class service and value for employee benefit group plans since 1987

For small employers shopping for group health coverage in 2026, the decision between the Affordable Care Act’s Small Business Health Options Program (SHOP) and the private small group market is rarely the first question that comes up — and it should be. The choice between these two purchasing channels affects what carriers you can access, what plans you can offer, whether you qualify for the Small Business Health Care Tax Credit, and how much administrative complexity you’ll absorb in setting up and renewing coverage.

The two channels aren’t competitors in the traditional sense. They’re parallel paths to the same destination — ACA-compliant group health coverage for small employers — with different rules, different financial mechanics, and different practical tradeoffs. Knowing which path fits your situation is a 30-minute analysis that can save thousands of dollars annually and dozens of hours in administrative friction.

Here is what each channel actually is in 2026, what has changed since SHOP’s original 2014 launch, and the framework small employers should use to choose between them.

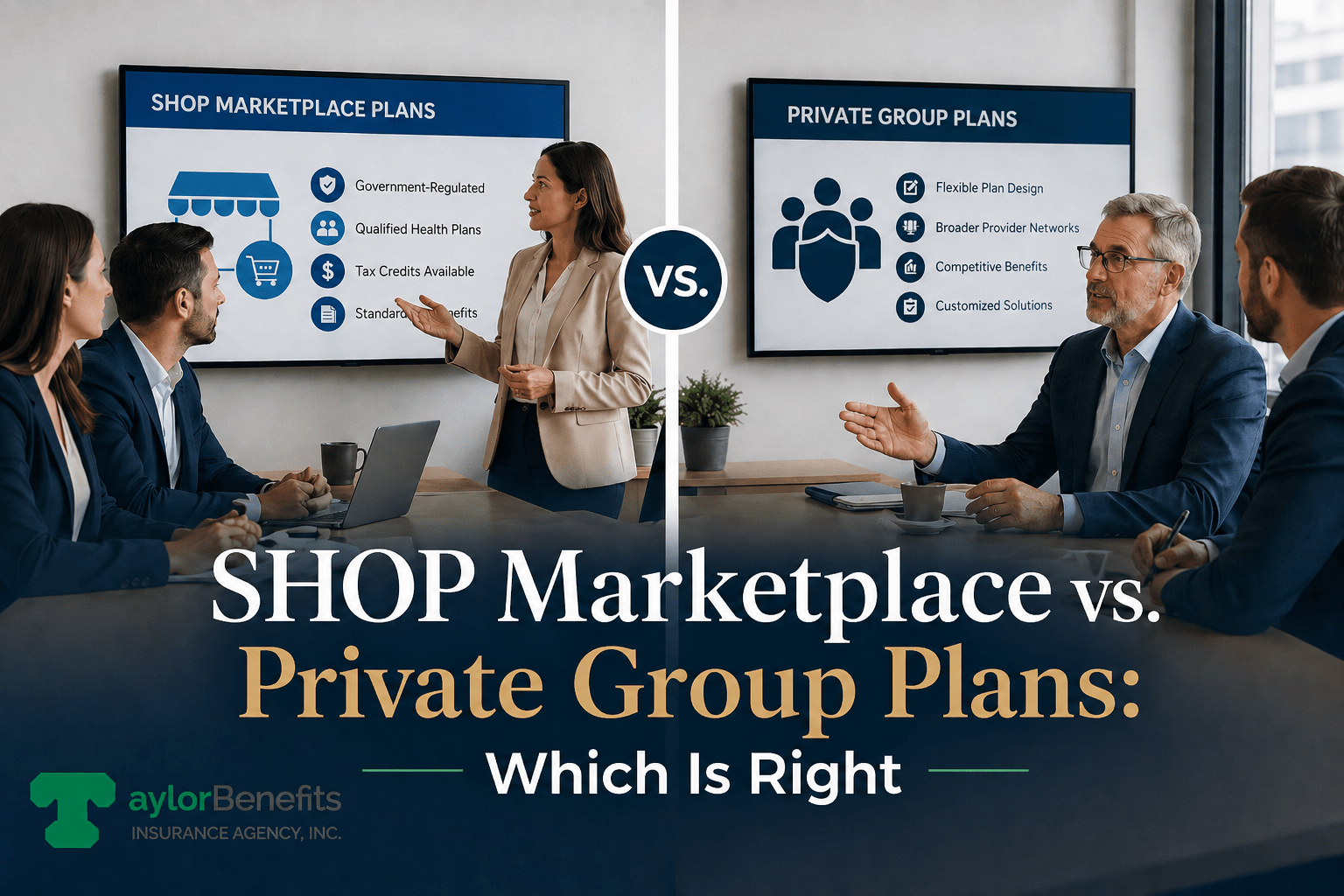

The SHOP Marketplace was created under the Affordable Care Act to give small employers (those with 1 to 50 employees in most states, 1 to 100 in some) a centralized purchasing channel for group health insurance, modeled loosely on the individual ACA exchanges. The original SHOP design promised employee choice across multiple carriers, simplified enrollment, and access to the Small Business Health Care Tax Credit.

That design has changed substantially. As of 2018, the federal SHOP marketplace at HealthCare.gov no longer provides online enrollment functionality. Instead, small employers in states using the federal SHOP work directly with SHOP-registered insurance carriers and SHOP-registered agents and brokers to enroll in qualifying plans. The “marketplace” function has been substantially decentralized — the SHOP designation now serves primarily as the gateway to tax credit eligibility rather than as a comparison-shopping platform.

A handful of states operate their own state-based SHOP exchanges with more functionality — California’s Covered California for Small Business, for example, retains a more centralized purchasing experience with employee choice features. The state-by-state variation matters: SHOP in California is a meaningfully different product than SHOP in Texas or Florida.

What hasn’t changed is the core financial benefit that drives most SHOP decisions: the Small Business Health Care Tax Credit is available only to employers who purchase coverage through SHOP. For employers who qualify, that credit can be substantial enough to make SHOP the obvious financial choice. For employers who don’t qualify, the SHOP designation provides little benefit relative to the private market.

The Small Business Health Care Tax Credit, codified in IRS Code Section 45R, provides eligible small employers with a tax credit of up to 50 percent of their employer-paid health insurance premiums (35 percent for tax-exempt employers). The credit is available for two consecutive taxable years and applies only to coverage purchased through SHOP.

To qualify for the credit, an employer must meet all of the following:

The credit’s value scales inversely with both employer size and average wages. Maximum credit amounts go to the smallest employers with the lowest wages — essentially, the businesses where premium costs represent the most significant share of operating expenses. For employers approaching 25 FTEs or with average wages near the upper threshold, the actual credit may be a small fraction of the headline 50 percent rate.

The practical implication: small employers should run the actual credit calculation — including the FTE count, average wage calculation, and applicable phaseout — before assuming SHOP is the right choice. For a 22-FTE employer with average wages of $58,000, the credit may be modest enough that the broader plan selection and competitive pricing in the private market outweigh the SHOP-only credit benefit. For a 12-FTE employer with average wages of $35,000, the credit may be substantial enough that SHOP is clearly the right choice regardless of plan variety.

The IRS provides a credit calculator and Form 8941 for claiming the credit. Run the numbers — or have your broker or accountant run them — before making a channel decision.

The private small group market — coverage purchased directly from carriers or through a broker, outside the SHOP designation — is where the majority of small employers ultimately purchase health coverage in 2026, even those who could theoretically use SHOP. The reasons are practical rather than ideological.

The private small group market in most states includes the full range of carriers offering small group coverage, including national carriers (United, Aetna, Cigna, Anthem) and regional carriers, and the full range of plan designs each carrier offers. SHOP-registered plans are typically a subset of each carrier’s small group portfolio — meaning a SHOP-restricted shopping process may exclude plan designs that would otherwise be available in the private market.

For employers whose employees have specific network preferences, who want access to particular plan structures (such as carrier-specific HDHP designs paired with carrier-administered HSAs), or who are evaluating level-funded products, the private market typically offers materially more options.

The private market operates through standard broker-carrier relationships that have been the small group infrastructure for decades. Brokers have direct quoting access, established renewal workflows, and ongoing carrier service relationships. This infrastructure is generally more responsive to mid-year service issues, claim disputes, and renewal negotiations than the SHOP-specific process — which routes some interactions through SHOP-registered intermediaries that add steps without adding value.

Both SHOP and private small group plans are fully ACA-compliant. Both must offer the ten essential health benefits, comply with rating restrictions, provide preventive services without cost-sharing, and meet all other ACA requirements. There is no compliance advantage to SHOP — the regulatory framework applies equally to both channels.

The private market is the only channel through which small employers can access level-funded health plans, traditional self-funded plans, and various hybrid funding arrangements. SHOP is structured around fully insured products. For small employers in the 25 to 100 employee range who are evaluating level-funded options as an alternative to community-rated fully insured coverage — a strategy covered in detail in Taylor Benefits‘ companion article on level-funded plan structures — the private market is the only practical path.

For small employers evaluating SHOP versus private group coverage in 2026, the choice comes down to five questions answered in sequence:

This is the threshold question, and it determines everything that follows.

If you have fewer than 25 FTEs, average wages below the applicable threshold, and you contribute at least 50 percent of employee-only premium, you qualify. Run the actual credit calculation against your projected premium costs. If the credit is large enough to materially change your benefits cost — typically the case for very small employers (under 15 FTEs) with lower average wages — SHOP becomes the strong default choice.

If you don’t qualify, or if the credit is modest enough that the broader plan selection in the private market outweighs the credit value, the private market becomes the default.

If your group size and claims profile make level-funded plans a serious consideration, the private market is the only channel that supports that evaluation. SHOP plans are fully insured products.

For small employers with 25 to 75 employees and a healthier-than-average workforce, the long-term cost advantage of level-funding may exceed the value of the SHOP tax credit even when the credit applies. Run both scenarios — SHOP fully insured with credit, private market level-funded without credit — before committing to a channel.

If your employees have established provider relationships across multiple carrier networks, or if your benefits strategy depends on access to specific plan designs that may not be in your state’s SHOP plan portfolio, the private market’s broader selection has real practical value.

If your workforce is concentrated geographically, has limited carrier preferences, and would be well-served by any major carrier’s standard plan offerings, SHOP’s narrower selection is unlikely to be a meaningful constraint.

SHOP is not a single product. The federal SHOP at HealthCare.gov, state-based SHOPs in states like California and DC, and SHOP availability in states with limited carrier participation each function differently.

In states with robust state-based SHOP exchanges and broad carrier participation, SHOP can offer a comparable experience to the private market with the added tax credit benefit. In states where federal SHOP operates with minimal infrastructure and limited carrier participation, the practical SHOP experience is closer to “private market with tax credit attached” — which is fine for tax credit eligibility but doesn’t deliver the centralized marketplace value the program was originally designed for.

Confirm with your broker how SHOP actually functions in your state before making the decision.

Both channels have annual renewal cycles, both require ACA-compliant employee notifications, and both involve broker coordination. The difference is in workflow specifics — particularly around plan changes, carrier transitions, and tax credit reapplication for employers who continue to qualify.

For employers with limited HR capacity, the smoother and more familiar process is generally the private market broker-administered model. For employers whose primary administrative concern is ensuring tax credit eligibility is properly documented and claimed, SHOP’s structured process can actually be simpler — assuming the broker is SHOP-experienced.

Synthesizing the framework above, here are the employer profiles where each channel typically delivers the strongest value:

Several outdated or partially accurate beliefs about SHOP continue to influence small employer decisions. The current reality:

“SHOP is a marketplace where I can compare plans online.” This was the original design but is no longer accurate for federal SHOP. Most SHOP enrollment in 2026 occurs through brokers and direct carrier engagement, with HealthCare.gov serving primarily as an information resource rather than a transactional platform. State-based SHOP exchanges retain more of the original marketplace functionality.

“SHOP plans are cheaper than private market plans.” They are not, structurally. SHOP and private market plans are subject to the same ACA rating rules. The financial advantage of SHOP comes entirely from the tax credit for eligible employers — not from premium pricing differences.

“SHOP gives my employees more plan choices than a single-carrier private plan.” Employee choice features within SHOP vary significantly by state. Federal SHOP and most state-based SHOP exchanges allow employers to offer either a single plan or multiple plans across one or multiple carriers — but the same flexibility exists in the private market through multi-carrier broker arrangements. Employee choice is not a SHOP-exclusive feature.

“I have to use SHOP if I want ACA-compliant coverage.” Untrue. All small group plans sold by ACA-licensed carriers are ACA-compliant, regardless of whether they’re sold through SHOP or the private market.

For most small employers in 2026, the SHOP versus private group decision reduces to one financial question: does the Small Business Health Care Tax Credit apply to your situation, and is it material enough to outweigh the broader plan selection and operational simplicity of the private market?

For employers under 15 FTEs with average wages well below the phase-out threshold, the credit is typically substantial enough that SHOP is the right answer. For employers approaching 25 FTEs or evaluating funding alternatives like level-funded plans, the private market typically offers more value. For the middle range — small employers who qualify for a partial credit but also have meaningful interest in plan flexibility — the analysis requires comparing actual numbers under both scenarios.

What hasn’t changed in 2026 is the importance of running the comparison rather than defaulting to either channel based on assumption. The right answer depends on your specific FTE count, wage profile, workforce health, state of operation, and benefits strategy — not on a general preference for one model or the other.

Taylor Benefits Insurance Agency works with small employers across both SHOP and private group market channels, including running side-by-side financial comparisons that capture both premium costs and applicable tax credits. If you’d like an analysis of which channel makes the most sense for your specific situation in 2026, contact our team for a no-obligation consultation.

* This content is for informational purposes only and does not constitute tax or legal advice. The Small Business Health Care Tax Credit is governed by IRS Code Section 45R, and eligibility, calculation, and documentation requirements are subject to IRS rules and applicable annual inflation adjustments. Consult a qualified tax advisor regarding your specific situation.

Employees usually cannot switch health coverage freely during the year unless they experience a qualifying life event such as marriage, job change, or loss of coverage. Most plans follow strict enrollment periods, so timing is important. Employers should explain options clearly during onboarding to avoid confusion and ensure employees stay continuously covered.

Annual renewal is often the best time to compare SHOP Marketplace and private group plans. Reviewing costs, provider networks, and coverage options helps employers choose the best fit for their business.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066