- Providing world class service and value for employee benefit group plans since 1987

Choosing a health plan during open enrollment is one of the most consequential financial decisions employees make each year. The average annual premium for employer-sponsored family coverage has climbed to nearly $27,000, with employees now contributing approximately $6,850 out of pocket. A poor plan choice can mean thousands of dollars in unnecessary costs, limited access to the providers an employee depends on, or inadequate coverage at the moment it’s most needed.

Despite the stakes, most employees approach open enrollment with limited time, limited information, and limited guidance. Research by WorldatWork found that roughly 50 percent of employees spend less than an hour choosing their health plan — and many misunderstand key cost drivers including prescription coverage and out-of-pocket maximums. The result is predictable: employees default to the plan they had last year, the plan with the lowest premium (which may not be the most cost-effective for their situation), or the plan that sounds most comprehensive even when a more targeted option would serve them better.

For HR teams and benefits leaders, employees making poor plan selections isn’t just a wellbeing concern. It generates a flood of mid-year benefits questions, erodes employee trust in their benefits program, and reduces the perceived value of benefits the employer is investing in. The good news is that this problem has a practical and increasingly accessible solution: decision-support tools built specifically to help employees make informed, personalized plan choices.

The challenge isn’t that employees are disengaged from their benefits — it’s that the decision is genuinely difficult without personalized support.

Deductibles, coinsurance, out-of-pocket maximums, HSA eligibility, in-network requirements — these terms have specific, consequential meanings that many employees don’t fully understand. Even employees who have had health insurance for years may not accurately define coinsurance or know what triggers their out-of-pocket maximum.

Comparing two health plans requires estimating future healthcare utilization, calculating total annual cost under each plan across multiple scenarios, and evaluating the financial tradeoffs between lower premiums and higher cost-sharing. Most employees don’t do this analysis — and without tools to support it, expecting them to is unrealistic.

When employees evaluate plans without support, they consistently over-weight monthly premium and under-weight total annual cost. An HDHP with a $200 lower monthly premium can be significantly more expensive in total cost for a family with moderate healthcare utilization — but without scenario modeling, that math is invisible.

Most enrollment platforms allow employees to roll over prior-year elections without active decision-making. For employees who found the decision difficult the first time, defaulting to prior coverage removes the friction — even when their situation has changed materially.

Open enrollment meetings, benefits guides, and plan comparison tables explain how plans work. They don’t tell an individual employee which plan is right for their specific healthcare usage, family composition, financial situation, and risk tolerance. The education gap is real, but generic education can’t close it.

Decision-support tools bridge the gap between general benefits education and the personalized guidance employees actually need to make good choices.

At their core, these tools work by asking employees questions about their personal circumstances and using the answers to model how each available plan option would perform for them over the course of the plan year. Instead of asking employees to interpret plan design documents on their own, the tool does the relevant math and surfaces the results in plain language.

A well-designed decision-support tool typically guides employees through questions about:

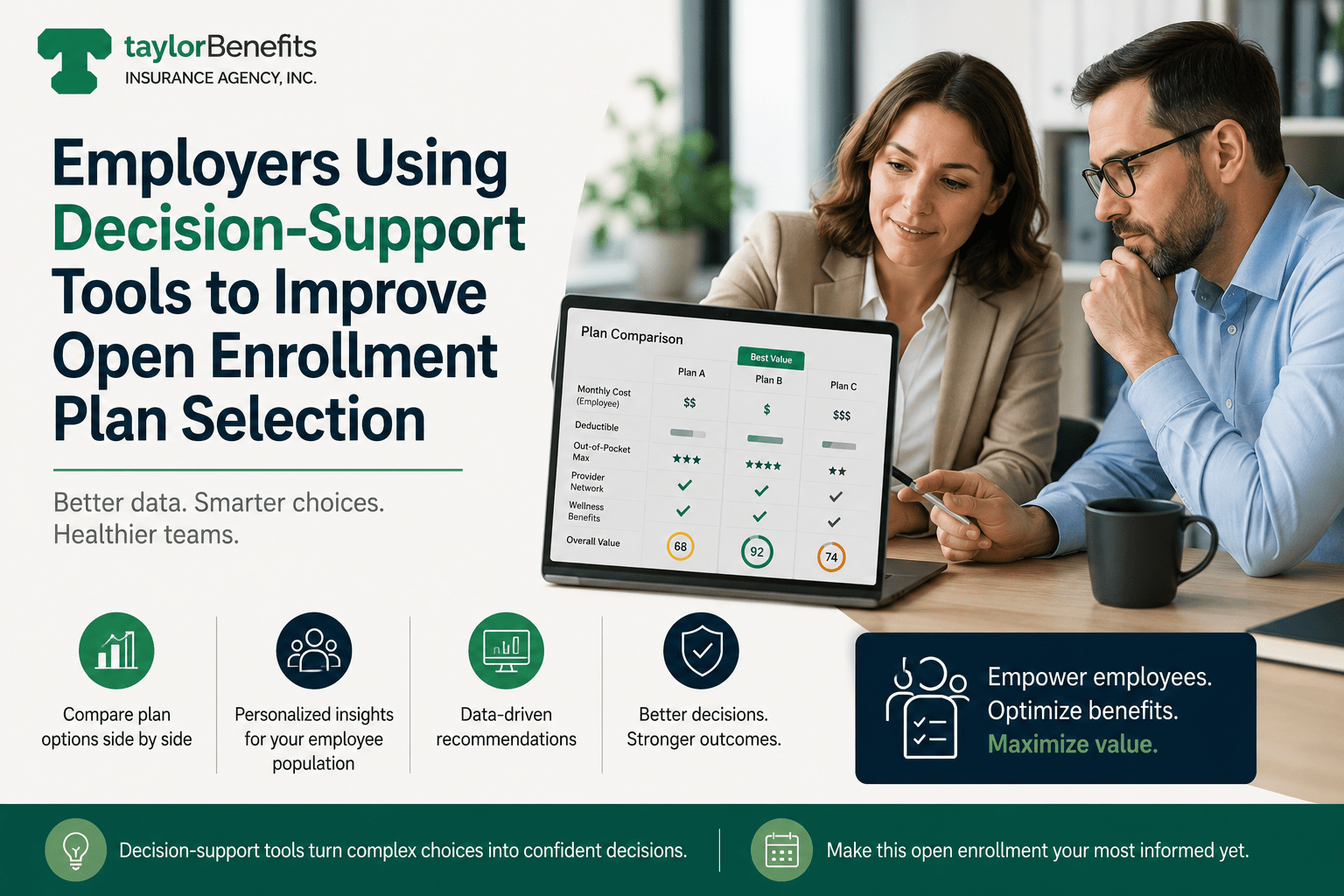

Based on these inputs, the tool models each plan option’s likely total annual cost — combining premium, expected deductible exposure, estimated copays and coinsurance, and out-of-pocket maximums — for the employee’s specific situation. It then presents plan options ranked or highlighted based on estimated total cost and coverage fit, in plain language the employee can understand.

The result shifts the employee’s decision from “which plan sounds best” to “here’s what each plan would actually mean for me financially and clinically this year.”

The quality of decision-support tools varies substantially across the market. The characteristics that distinguish effective tools:

Surface-level decision support asks about family size and produces a basic recommendation. Deep decision support incorporates actual prescription drug information, anticipated specialist care, provider network verification, and financial risk tolerance. The deeper the personalization, the more accurate the recommendation.

The tool should model estimated total annual cost under each plan — not just compare monthly premiums. This is the single most important feature because it corrects the premium bias that drives most poor plan selections.

Employees who don’t understand the inputs can’t evaluate the outputs. Decision-support tools that output plan recommendations in insurance terminology miss the communication point. The best tools translate everything into plain language: “Based on your expected healthcare usage this year, Plan B would likely cost you about $1,400 less than Plan A.”

For employees with established specialists or primary care providers they want to keep, network verification — confirming that specific providers are in-network for each plan option — is a critical decision input. Tools that include provider lookup as part of the decision process serve employees far better than those that require a separate lookup.

For employees evaluating HDHP options with HSA eligibility, decision support should include HSA modeling — showing how employer HSA contributions and employee contribution potential affect the net cost comparison between the HDHP and other options. This is often the piece of the HDHP value proposition that employees miss without specific guidance.

Decision support that requires desktop access and 20 minutes of focused attention will not reach employees who most need it. Mobile-first tools with streamlined question flows produce substantially higher engagement than desktop-only alternatives.

For HR teams and benefits leaders, the case for implementing decision-support tools extends beyond employee wellbeing into program performance.

A decision-support tool is most effective when it’s embedded into the enrollment experience rather than offered as a separate resource employees have to seek out. Practical integration points:

Employers who implement decision-support tools should track whether they’re actually improving plan selection quality. Useful metrics:

Decision-support tool utilization rate. What percentage of eligible employees engaged with the tool during open enrollment? Low utilization suggests communication or access barriers that need to be addressed.

Plan switching rates among tool users vs. non-users. Employees who engage with decision support should have higher plan switching rates (indicating active decision-making) than those who don’t — though this depends on how well-matched prior year enrollment was.

Post-enrollment survey scores. Brief post-enrollment surveys that ask employees whether they felt informed and confident about their plan choice provide direct signal on whether decision support is improving employee experience.

Mid-year benefits question volume. Over time, better-informed plan selection should reduce the volume of mid-year questions to HR related to unexpected costs, coverage misunderstandings, and network issues.

Open enrollment will never be simple. But it doesn’t need to produce the mismatched plan selections and financial surprises that currently affect a significant share of employees every year. Decision-support tools give employees what generic benefits education can’t: personalized guidance based on their specific situation that translates complex plan tradeoffs into clear, actionable recommendations.

For employers who have invested in good health plan options and competitive contribution structures, decision support is what makes that investment visible and valuable to employees. For HR teams managing enrollment complexity, it’s the tool that reduces mid-year dissatisfaction and benefits questions.

In 2026, decision support is increasingly standard at competitive employers. For those who haven’t yet implemented it, the gap between what employees are experiencing and what they could be experiencing is increasingly visible — and increasingly addressable.

Taylor Benefits Insurance Agency helps employers evaluate and implement decision-support tools as part of a comprehensive open enrollment strategy. If your current enrollment process produces the passive default patterns and post-enrollment confusion described in this article, contact our team to discuss what better enrollment support looks like.

Decision-support tool capabilities, integration options, and pricing vary by vendor and benefits administration platform. The WorldatWork data cited in this article reflects published research findings. Specific outcomes vary by workforce characteristics and implementation approach.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066