- Providing world class service and value for employee benefit group plans since 1987

Small business owners shopping for group health insurance frequently encounter two distinct paths: working with a Professional Employer Organization (PEO) or working with an independent benefits broker. Both promise to simplify benefits for small employers. Both offer access to competitive coverage. And both are widely used.

They are, however, fundamentally different arrangements — different in how they work, what they cost, what control they give the employer, and what happens when the relationship changes. Understanding those differences is essential to making the right choice, because the trade-offs aren’t always visible at the point of sale.

This article explains how each model works, the key differences between them, and the circumstances in which each tends to make more sense for small employers.

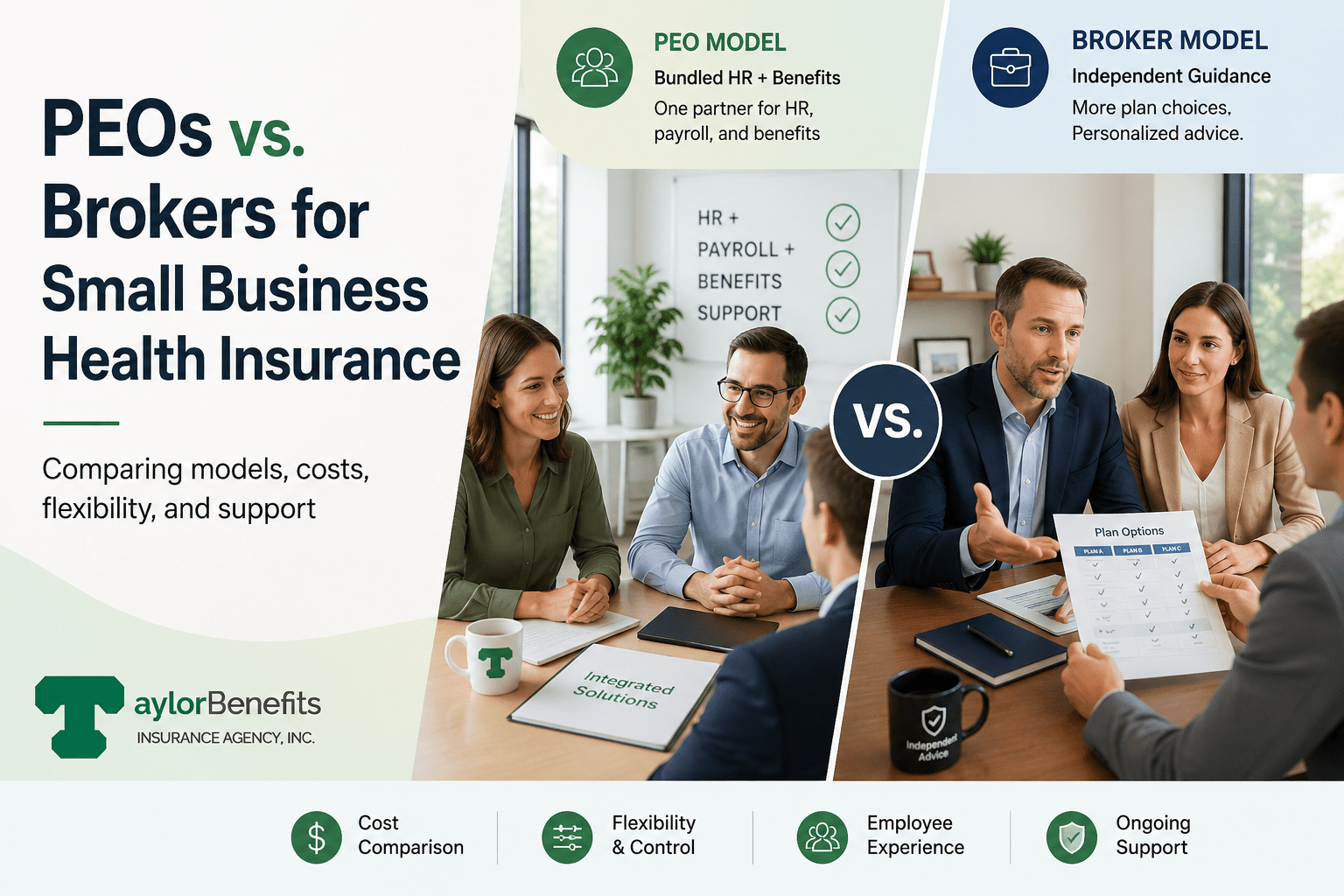

A Professional Employer Organization is a company that enters into a co-employment arrangement with a client business. Under this arrangement, the PEO becomes the employer of record for the client’s employees — handling payroll processing, payroll taxes, HR administration, workers’ compensation, and benefits.

For health insurance specifically, the PEO pools its clients’ employees into a single large group and obtains health coverage for the combined pool. Because the PEO aggregates employees from many small businesses, it can access pricing and plan options typically reserved for larger employer groups. This is the core value proposition: a small business gets access to the PEO’s health plan, which benefits from large-group economics.

From the employee’s perspective, the employer’s name on the health insurance may be the PEO’s name rather than the small business’s name. From the business owner’s perspective, the PEO manages payroll taxes under the PEO’s employer identification number (in most arrangements), files W-2s under the PEO’s EIN, and takes on certain employer-side compliance obligations.

PEOs typically charge for their services through one of two fee structures: a percentage of total payroll (often 2 to 12 percent) or a flat per-employee per-month fee. Health insurance costs are typically bundled into or alongside the PEO fee.

An independent benefits broker works directly with the employer to design, source, and manage the employer’s group health insurance and broader benefits program. The broker represents the employer’s interests in the marketplace — soliciting quotes from multiple carriers, presenting options, making recommendations, and managing the enrollment, renewal, and service relationship on an ongoing basis.

Unlike the PEO, the broker does not become a co-employer. The business remains the employer of record for all employees. The health insurance is purchased by the business from the carrier of the employer’s choice, with the broker as the intermediary.

Broker compensation is typically paid by the insurance carrier — through commissions embedded in the premium — rather than directly by the employer. Under CAA 2021, brokers servicing ERISA-governed plans are required to disclose the full amount and sources of their compensation.

The employer retains full control over plan design, carrier selection, contribution structures, and benefits strategy. The broker advises, sources, and manages — but the employer owns the benefits program.

With a PEO, the employer is typically joining the PEO’s existing group health plan rather than designing a plan from scratch. The PEO determines which carriers are available, which plan options are offered, and what the underlying plan structure is. The employer selects from the PEO’s available menu.

With a broker, the employer chooses the carrier, the plan design, the contribution structure, the ancillary benefits, and every other dimension of the benefits program. The broker sources the market on the employer’s behalf based on the employer’s specific requirements. The flexibility is substantially greater.

For small businesses with standard benefits needs, the PEO’s menu may be perfectly adequate. For small businesses with specific plan requirements — particular networks, specific pharmacy needs, a workforce in multiple states, or a desire to explore level-funded options — broker flexibility matters.

PEO pricing bundles health insurance costs with payroll administration, HR services, and other PEO functions. The all-in cost can be competitive for very small employers — particularly those under 20 employees who lack the purchasing power for competitive group rates individually — but the bundled pricing makes it difficult to assess what the employer is actually paying for health insurance specifically versus the other PEO services.

Broker-arranged coverage is priced transparently: the employer sees the carrier’s premium quote, the employer’s contribution structure, and the broker’s disclosed compensation. The cost of health insurance is visible and separable from other services.

One specific consideration: health insurance costs in a PEO arrangement are governed by the PEO’s rates, which reflect the overall claims experience of the PEO’s pooled population — not just the specific employer’s employees. If the employer’s employees are healthier than the PEO’s average pool, the employer may effectively be subsidizing less healthy clients in the PEO’s book. There’s no mechanism to capture the financial benefit of favorable workforce health within the PEO model.

With broker-arranged coverage, particularly for self-funded or level-funded plans available above approximately 25 to 30 employees, a group with favorable health experience can directly benefit from lower cost-adjusted premiums or year-end surplus returns.

When a small employer joins a PEO, the health insurance relationship is between the PEO and the carrier — not between the employer and the carrier. If the employer later leaves the PEO, the employees typically lose access to the PEO-sponsored health plan and must transition to new coverage. This transition creates disruption for employees who may need to change providers, and may occur at a time not of the employer’s choosing.

With broker-arranged coverage, the insurance contract is between the employer (as plan sponsor) and the carrier. If the employer changes brokers, the coverage continues. If the employer decides to change carriers at renewal, the broker manages that process. The employer’s relationship with the benefits program is continuous and portable regardless of what happens to the broker relationship.

In a PEO arrangement, the PEO takes on certain HR and payroll compliance obligations as co-employer — including payroll tax filings, workers’ compensation, and some employment law compliance. ERISA compliance for the health plan, however, may or may not be fully transferred depending on the PEO structure and contract terms. Employers should specifically confirm what compliance obligations they retain in a PEO arrangement.

With a broker, the employer retains full employer responsibility for compliance — payroll, employment law, ERISA, ACA reporting, and everything else. The broker advises on benefits-related compliance and may coordinate with compliance vendors, but the employer owns the compliance obligations. For employers who want to retain control and understand what they’re responsible for, this clarity is an advantage.

One argument in favor of PEOs for very small employers is the bundled HR services — payroll processing, HR technology, employee handbooks, HR helplines, and related services — that come alongside the health insurance in the PEO package. For employers with no internal HR capacity, this bundle can be genuinely valuable.

This comparison is valid but should be evaluated on its own terms. HR services available through a PEO are increasingly available through standalone HRIS platforms, payroll processors, and HR services providers — often at competitive cost and without the co-employment arrangement.

PEOs are most compelling for employers in specific circumstances:

For these employers, the PEO’s value proposition can be genuine and the trade-offs may be acceptable.

For most small businesses — particularly those above 15 to 20 employees who can access competitive small group pricing or level-funded options — a broker relationship delivers advantages that a PEO cannot match:

If you are evaluating a PEO, important considerations include the PEO’s financial stability (PEO failures have left small employers responsible for unpaid benefit claims), the specific health plan options available, the exact fee structure and total cost versus going independently, what compliance obligations you retain versus transfer, and what the exit process looks like if you decide to leave.

The PEO model involves handing significant administrative and compliance infrastructure to a third party. Understanding exactly what you are and aren’t receiving before signing a multi-year agreement is essential.

Both PEOs and brokers provide small businesses with access to group health insurance. The difference is in control, cost transparency, portability, and long-term flexibility.

For most small businesses above 15 to 20 employees, working with an experienced independent benefits broker delivers greater flexibility, better cost transparency, and a benefits program that grows with the business — without the co-employment structure, bundled pricing, and carrier menu constraints that come with a PEO.

For the smallest employers who genuinely cannot access competitive group rates independently, a PEO may bridge the gap until the business is large enough for a standalone approach to be competitive.

The right question isn’t “which is cheaper right now” — it’s “which arrangement gives my business the right foundation as we grow.”

Taylor Benefits Insurance Agency has helped small businesses across industries design competitive group health programs since 1987. If you’d like to compare your current or potential PEO arrangement against what an independent broker can offer your specific business, contact our team for a no-obligation consultation.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066