- Providing world class service and value for employee benefit group plans since 1987

A growing number of U.S. employers operate with workforces that include both W-2 employees and 1099 independent contractors. A consulting firm with a core team of full-time staff and a roster of independent specialists they engage on project work. A creative agency with employed designers and freelance contractors. A technology company with engineers on payroll and developers on contract. A manufacturing company with permanent operations staff and contracted technicians for specialized maintenance. The mixed-workforce model has become standard practice across many industries — and it has created a benefits structure question that doesn’t have an obvious answer.

The instinct of many employers in this position is to extend their benefits programs to include 1099 contractors — out of fairness, out of competitive recruitment pressure, or out of a sense that contractors who work alongside employees should receive comparable support. The instinct is understandable. The execution, however, runs into legal, tax, and regulatory frameworks that were largely designed around a clear distinction between employees and contractors and that don’t accommodate well-intentioned blurring of that distinction.

This article covers what employers can actually do to support 1099 contractors with benefits-like offerings, what they can’t do without creating significant legal risk, and how to structure benefits programs that serve mixed workforces appropriately.

Before getting to benefits structures, it’s essential to understand the foundation that constrains the conversation. Worker classification — whether someone is properly an employee or an independent contractor — is determined by the substance of the working relationship under various federal, state, and tax law tests. The most important federal tests include:

The factor that connects worker classification to the benefits question directly: providing benefits to a worker is one of the factors that can be used to establish that the worker is actually an employee, not a contractor. This isn’t speculation — it’s explicit in IRS and DOL guidance and in court decisions interpreting worker classification standards.

If an employer provides health insurance, retirement benefits, paid time off, or similar traditional employment benefits to a 1099 contractor, that fact will be considered by a regulator or court evaluating whether the worker should have been classified as an employee. The benefits provision may not be determinative on its own, but it weighs against the contractor classification — and combined with other factors that often coexist with mixed-workforce arrangements, it can be the factor that tips a worker classification analysis from contractor to employee.

The consequences of misclassification are substantial: back wages and overtime, payroll tax liability with penalties and interest, ACA penalties for failure to offer coverage to misclassified employees, retirement plan compliance failures if the worker should have been included in plan participation, and state-level penalties that vary by jurisdiction. Misclassification cases can produce liability running into millions of dollars for employers with significant misclassified populations.

This is the framework that constrains what employers can and cannot do for 1099 contractors. Understanding it is foundational to designing a defensible mixed-workforce benefits approach.

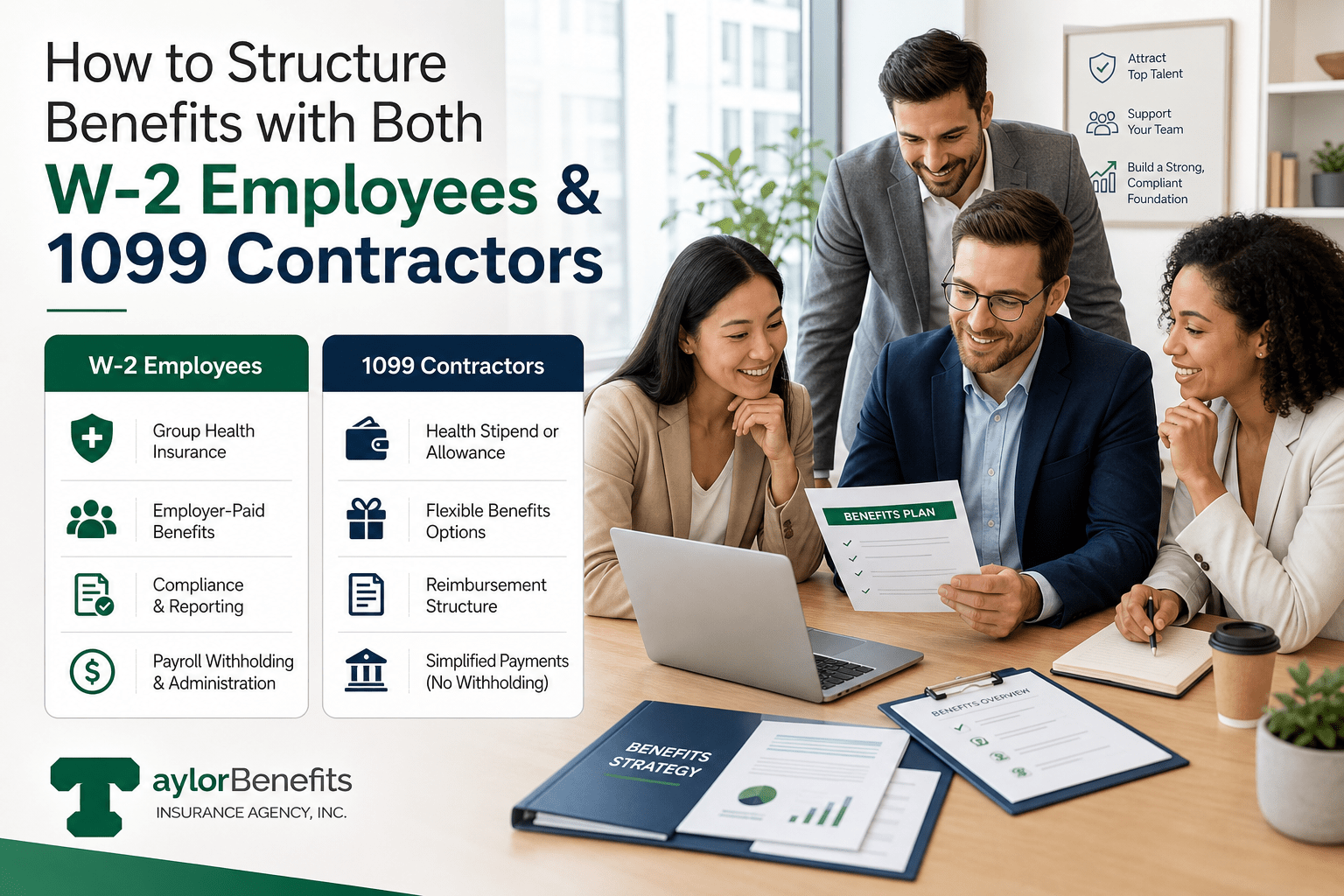

What Can Be Offered to W-2 Employees Only

What Can Be Offered to W-2 Employees OnlyThe starting point is being clear about what the standard employer benefits program is — and being deliberate that it is offered exclusively to W-2 employees, not extended to 1099 contractors regardless of how integrated the contractors are with the employed workforce.

The benefits in this category include:

The principle: anything that is structurally tied to the employer-employee relationship through ERISA, the tax code, or insurance contract terms is limited to W-2 employees. Attempting to extend these to 1099 contractors creates legal risk that materially exceeds any benefits-design value.

There are categories of support that can legitimately be offered to both employees and contractors without creating worker classification risk — provided they are structured appropriately. The key principles: the offering should be available to the contractor in their capacity as a service provider rather than as an employee, should not duplicate the structure of traditional employee benefits, and should not be tied to ongoing duration of the relationship in ways that suggest employment.

The pattern: offerings that are practical, work-related, or community-based can typically be inclusive. Offerings that mirror traditional employment benefits should not be.

Rather than trying to extend traditional employment benefits to 1099 contractors, the more legally defensible and practically useful approach is to structure contractor compensation in ways that explicitly recognize the absence of benefits.

The standard practice for sophisticated organizations engaging 1099 contractors is to pay rates that are explicitly higher than what comparable W-2 employees earn — with the differential reflecting the cost of benefits the contractor must provide for themselves.

The math is straightforward. A W-2 employee earning $100,000 in annual salary typically receives $25,000 to $35,000 in additional benefits and employer payroll taxes, making the total cost of employment approximately $125,000 to $135,000. A comparable 1099 contractor performing similar work should be compensated at a rate that captures the full economic value of the role — typically annualized to $130,000 or more — with the contractor responsible for purchasing their own health insurance, funding their own retirement, paying their own self-employment taxes, and absorbing the absence of paid time off.

This approach respects the contractor’s status as an independent service provider while ensuring they’re compensated at a level that reflects the genuine economic value of the work. Many sophisticated contractors actively seek out organizations that compensate this way precisely because the higher cash compensation gives them flexibility to structure their own benefits situation.

For organizations engaging contractors at meaningful scale, communicating the compensation logic explicitly — through contract terms that reference the loaded-rate concept, through onboarding materials that explain the approach, and through ongoing dialogue — has practical benefits. It signals that the organization understands and respects the contractor’s economic reality, and it pre-empts conversations about benefits parity that arise when contractors feel they’re being underpaid relative to comparable employees.

The compensation structure for contractors also affects worker classification analysis. Hourly compensation for ongoing work tied to a regular schedule looks more employment-like than project-based compensation for defined deliverables. Where the work and the relationship support it, project-based compensation structures support the contractor classification more strongly than hourly arrangements.

Beyond compensation structure, employers can support 1099 contractors in their independent benefits decisions through information and access — without crossing into providing benefits directly.

Independent contractors typically purchase individual health insurance through the ACA Marketplace, through professional association group purchasing arrangements, or through specialized contractor insurance programs. Employers can support contractors with informational resources about these options without providing the insurance directly.

Practical approaches:

This kind of informational support is valuable to contractors and creates no worker classification concern — the employer is providing information, not benefits.

Independent contractors have access to retirement savings vehicles specifically designed for self-employed individuals — Solo 401(k) plans, SEP-IRAs, and SIMPLE IRAs (in some structures). These vehicles often have higher contribution limits than traditional employee 401(k) plans and provide significant tax advantages for high-earning contractors.

Employers can provide informational resources about these options and direct contractors toward financial advisors who specialize in self-employment retirement planning, without providing retirement benefits directly.

The administrative burden of self-employment — quarterly estimated tax payments, self-employment tax calculations, business expense tracking, retirement plan administration — can be significant for contractors who are new to the structure. Employers can provide informational resources about these obligations or partner with services that specialize in supporting independent contractors, without creating worker classification concerns.

In some industries, professional associations offer group purchasing for health insurance, retirement plans, professional liability insurance, and other benefits-like products for member contractors. Employers can encourage contractors to evaluate these options and may provide modest support (such as paying for professional association membership as part of the contractor agreement) without crossing into employee benefits territory.

Several specific scenarios within the mixed-workforce category create distinct considerations.

The highest-risk situation in mixed workforces is the long-term 1099 contractor whose working relationship looks substantially like employment — multi-year continuous engagement, full-time hours, single client, work directed by the client, integrated into the client’s operations. These workers are at significant risk of being reclassified as employees by the IRS, DOL, or state regulators, regardless of how the relationship is documented.

For these workers, the appropriate response is typically to convert them to employee status — which then makes them eligible for employee benefits — rather than to attempt to extend benefits while maintaining contractor status. The conversion may have meaningful cost and administrative implications, but it resolves the misclassification risk that would otherwise compound over time.

When contractors are engaged through staffing agencies, professional employer organizations (PEOs), or other intermediaries, the benefits relationship is typically with the intermediary rather than with the client company. The staffing agency or PEO may provide benefits to the workers (treating them as employees of the agency), and the client company is paying a marked-up rate that reflects those benefits costs.

This structure can be operationally simpler for client companies that need contractor flexibility but are concerned about classification risk. The cost is typically higher than direct contractor engagement (because the intermediary captures margin), but the legal certainty about classification is materially stronger.

Contractors who work through their own LLCs, S-Corps, or other business entities — with appropriate business infrastructure (separate bank accounts, business insurance, multiple clients, employees of their own) — generally present lower classification risk than individual contractors operating as sole proprietors. The business-to-business relationship is structurally different from the more ambiguous individual-to-employer relationship.

For mixed workforces that include both individual contractors and contractor business entities, the benefits-related considerations differ. Business entities are typically not eligible for or interested in individual benefits anyway, simplifying the conversation considerably.

Equity compensation for 1099 contractors — stock options, restricted stock, or profit-sharing arrangements — can be structured legally but requires careful execution. The tax treatment for non-employees differs from employee equity (typically requiring inclusion of the equity value as income at grant or vesting), and the documentation must explicitly recognize the contractor relationship.

For organizations engaging strategic long-term contractors who would benefit from equity participation, working with counsel to structure appropriate non-employee equity arrangements is the right approach — rather than trying to extend employee equity plans to contractors.

Beyond the specific benefits decisions, the mixed-workforce question has broader implications for how organizations think about workforce composition and strategy.

The legal framework for worker classification effectively forces organizations to make a fundamental decision about each role: is this work that should be performed by an employee (with all the benefits, payroll tax obligations, and ongoing employment relationship that entails), or is this work that should be performed by an independent contractor (with the higher cash compensation, lack of benefits, and project-based or term-limited relationship that entails)?

The temptation to have it both ways — engaging workers as contractors to avoid the cost and administrative complexity of employment while extending some benefits to maintain recruitment competitiveness — is what produces the misclassification risk. The legally defensible approaches require choosing one path:

For roles that are genuinely contractor work — defined deliverables, multiple potential clients, contractor-controlled work methods, project-based or term-limited engagement — engage as 1099 contractors with loaded rates that reflect the absence of benefits, and provide informational resources without providing benefits directly.

For roles that are genuinely employee work — ongoing engagement, integrated into operations, employer-directed work methods, full-time or substantial-time commitment — engage as W-2 employees and provide the standard benefits program. Don’t try to engage these as contractors to save on benefits cost; the misclassification risk substantially exceeds the savings.

For roles in the genuine middle — there are some — consider structures that accommodate the ambiguity, such as engagement through staffing agencies, PEO arrangements, or carefully structured part-time employment. These structures provide legal clarity at modest cost premium over pure contractor engagement.

The mixed-workforce benefits question doesn’t have an aggressive solution that captures the upside of treating contractors well without the legal risk. The framework constraining benefits design for contractors is real, the misclassification consequences are substantial, and the practical answers are more conservative than many employers would like.

What employers can do effectively: structure W-2 employee benefits programs that are competitive and well-designed, compensate 1099 contractors at loaded rates that genuinely reflect the absence of benefits, provide informational resources that help contractors structure their own benefits situation, and be deliberate about which workers belong in which classification rather than letting ambiguity persist.

What they should avoid: extending traditional employment benefits to 1099 contractors regardless of intent, allowing long-term contractor relationships to operate in ways that look like employment without converting the workers to employee status, and treating worker classification as a documentation question rather than a substantive one.

Mixed workforces are the modern reality for many organizations. Managing them well — both for legal compliance and for genuine workforce competitiveness — requires accepting the framework rather than trying to work around it.

Taylor Benefits Insurance Agency works with employers on benefits strategy across mixed workforces — including W-2 employee program design, contractor compensation structuring, and the specific resources that can be made available to non-employees without creating classification risk. If you’re navigating the benefits implications of a mixed workforce, contact our team for a consultation.

In most cases, contractors should not be added to employee benefit programs, even on a temporary basis. Doing so can blur the legal distinction between employees and independent contractors, which may create compliance risks. Instead, companies usually support contractors through higher pay rates or project-based perks rather than structured benefits. If long-term support is needed, it is safer to convert the contractor into a W-2 employee.

Misclassifying workers or offering identical benefits without reviewing legal requirements can create compliance issues. A well-defined benefits strategy helps reduce risk while supporting both employees and eligible contractors.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066