- Providing world class service and value for employee benefit group plans since 1987

Employee benefits like paid vacation, dental and vision, life insurance, tuition reimbursement, and retirement plans can be powerful recruiting tools, but they’re usually optional. Separate from those “voluntary” perks are statutory (mandatory) benefits, which are required under federal and/or state law and often funded through payroll taxes, insurance coverage rules, or compliance obligations.

The tricky part: your obligations can change based on where you operate and how many employees you have. That’s why understanding mandatory benefits is the first step to building a compliant benefits strategy that also supports retention and culture.

Below is a practical breakdown of the core statutory benefits employers should understand, plus where requirements often vary.

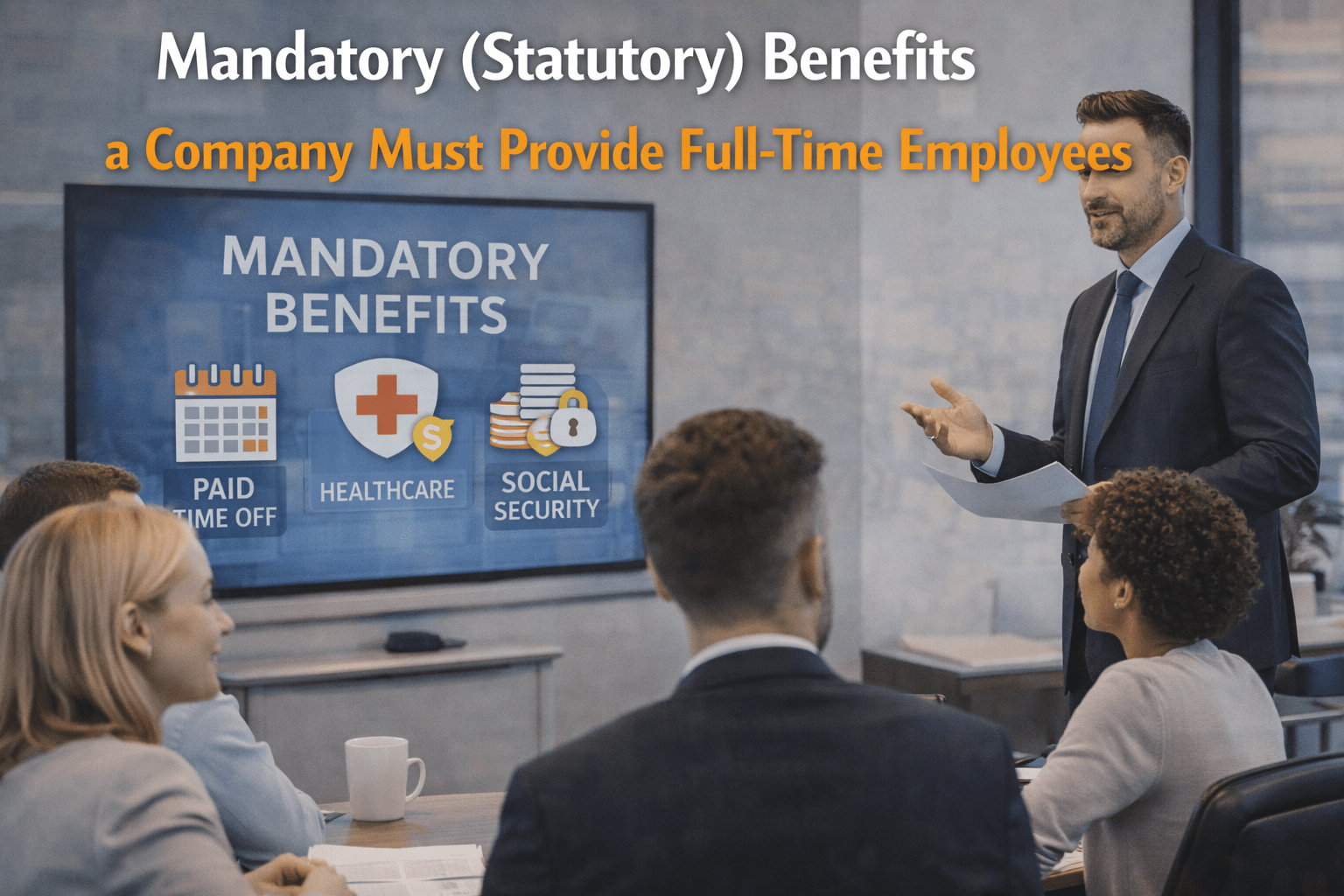

Statutory benefits are benefits (or benefit-like protections) that employers are legally required to provide or facilitate. In many cases, these aren’t “benefits you choose from a menu,” but rather programs you fund through payroll taxes or required insurance coverage.

In general, mandatory benefits fall into a few buckets:

Payroll tax programs (e.g., Social Security and Medicare)

Insurance programs (e.g., unemployment insurance, workers’ comp)

Job-protection leave requirements (e.g., FMLA)

State-required programs (e.g., state disability insurance in certain jurisdictions)

Because rules vary widely, employers should review federal, state, and local requirements (and consult counsel where appropriate).

Under the Federal Insurance Contributions Act (FICA), employers are responsible for withholding and paying payroll taxes that fund Social Security and Medicare.

Key points employers should know:

Social Security tax: 6.2% withheld from employee wages and 6.2% matched by the employer, up to the annual wage base limit.

The Social Security wage base is $176,100 for 2025 and $184,500 for 2026.

Medicare tax: 1.45% withheld and 1.45% matched by the employer, with no wage base cap.

Additional Medicare tax: employees may owe an additional 0.9% over certain thresholds; employers generally withhold the additional 0.9% once an employee’s wages exceed $200,000 (regardless of filing status). (Confirm mechanics with payroll/tax counsel if you have highly compensated employees.)

Why it matters: FICA compliance is foundational. Errors here can cascade into W-2 issues, amended filings, and penalties.

Employers fund unemployment insurance through federal and state payroll taxes, but states administer the benefits. Whether a former employee qualifies depends on state eligibility rules, but employer participation and contributions are a core compliance requirement.

What employers should keep in mind:

Your state unemployment tax rate may vary based on your “experience rating” (claims history).

UI requirements and taxable wage bases vary by state, so multi-state employers often need more careful setup and monitoring.

Why it matters: UI is both a compliance item and a cost-control area. Claims management and documentation processes matter.

In most states, employers must carry workers’ compensation coverage to protect employees who experience a work-related injury or illness. Requirements, thresholds, and exemptions vary by state.

Common ways employers satisfy workers’ comp rules include:

Purchasing coverage through a private carrier

Using a state-run program (where applicable)

Qualifying for self-insurance (typically requires approvals and financial capacity)

Why it matters: Workers’ comp is one of the fastest ways to incur serious penalties if ignored, and it’s also critical for risk management.

Not every employer is required to offer health coverage. But under the Affordable Care Act (ACA), Applicable Large Employers (ALEs) generally face penalties if they don’t offer affordable, minimum-value coverage to full-time employees (and dependents), and at least one full-time employee receives a premium tax credit.

Two key concepts:

ALE status: generally an employer averaging 50+ full-time employees (including full-time equivalents) in the prior calendar year.

Full-time definition for ACA: generally 30+ hours/week or 130 hours/month on average.

The affordability percentage is indexed annually. For plan years beginning in calendar year 2026, the IRS set the required contribution percentage at 9.96%.

Why it matters: Employers frequently get tripped up not by “offering coverage,” but by affordability testing, measurement methods, dependents, and reporting.

The FMLA provides eligible employees of covered employers with unpaid, job-protected leave for qualifying family and medical reasons.

In general:

Covered employers include many private employers with 50+ employees, public agencies, and schools.

Eligible employees can take up to 12 weeks of unpaid, job-protected leave in a 12-month period for qualifying events.

There is also military caregiver leave that can extend up to 26 workweeks in a single 12-month period for eligible situations.

Important: FMLA is a job-protection law and does not require wage replacement. However, some states and localities require paid family/medical leave or paid sick leave that can interact with FMLA.

A handful of jurisdictions require employers to provide (or participate in) short-term disability wage replacement programs. Rules vary by state regarding:

Funding (employer-paid, employee-paid, or shared)

Waiting periods and eligibility rules

Approved carriers or state programs

If you operate in multiple states, disability requirements are a common “gotcha,” especially when you hire remote employees.

Statutory benefits are required and generally tied to taxes, insurance rules, and job-protection laws.

Voluntary benefits are offered at the employer’s discretion and may include:

Paid vacation/holidays (beyond what’s required by state/local law)

Retirement plan matches and profit sharing

Life and disability (where not mandated)

Dental/vision

Tuition assistance

Wellness programs

Childcare support

Voluntary benefits still have important compliance considerations (tax treatment, nondiscrimination rules, plan documents, ERISA applicability), but the “must offer” decision is usually yours.

Sometimes. This is where employers need to be careful: “part-time” is not always “excluded.” Depending on the benefit and the law:

Workers’ compensation and unemployment rules often apply broadly to employees on payroll.

Under the ACA, employees averaging 30+ hours/week may be full-time for employer mandate purposes even if you call them part-time.

Retirement plan eligibility can be triggered by service thresholds (and additional long-term part-time rules may apply depending on plan type and year).

Bottom line: eligibility should be defined clearly in your policies and plan documents — and aligned with federal/state rules.

Compliance is only the baseline. The real opportunity is building a benefits strategy that:

Meets statutory obligations cleanly

Supports retention and recruiting

Aligns with your budget and workforce demographics

Reduces administrative friction and reporting risk

Taylor Benefits Insurance Agency can help you evaluate your legal obligations, identify gaps, compare plan structures, and build a compliant, modern benefits package that employees actually value.

Certain statutory benefits apply to all employees regardless of hours worked. Programs such as Social Security, Medicare, and workers’ compensation typically require employer participation for both full time and part time staff. However, some laws that apply specifically to health coverage or family leave may use minimum hour thresholds to determine eligibility. Employers must check the rules tied to each program to understand where part time workers qualify.

In most cases, no. Statutory benefits are legally required protections and cannot simply be replaced with cash. Employers must comply by providing the actual benefit, such as insurance or paid leave, as defined by law rather than offering an alternative payout.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066