- Providing world class service and value for employee benefit group plans since 1987

In today’s competitive tech market, small businesses need to balance employee benefits with financial sustainability. That was the challenge faced by CloudBright*, a 35-employee SaaS company based in Austin, Texas. With health insurance premiums rising every year and employee satisfaction starting to dip, they partnered with Taylor Benefits Insurance to find a smarter, more sustainable group health insurance strategy. Here is how we helped them find the best group health and employee benefits plan, so that all their current and upcoming employees are fully covered and satisfied with benefits.

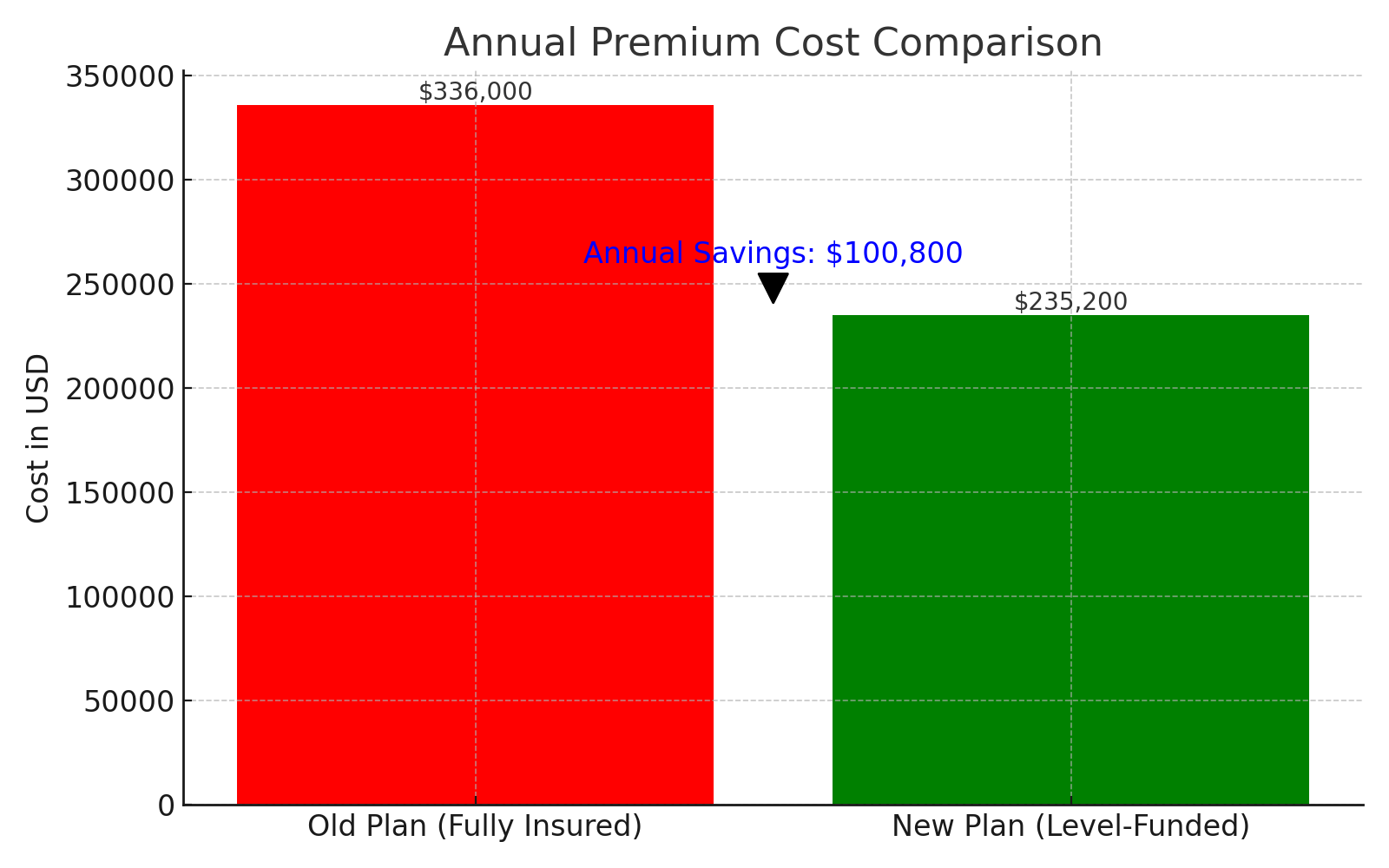

CloudBright was offering a standard fully insured PPO plan through a national carrier. While the network was broad, the monthly premiums were soaring—costing the company nearly $28,000 per month. At the same time, employees were dissatisfied with high out-of-pocket costs and limited plan flexibility.

Key pain points:

CloudBright’s HR director had heard of Taylor Benefits through a referral and scheduled a consultation. Within 48 hours, our team:

We provided a comprehensive plan redesign proposal tailored to CloudBright’s employee demographics, usage patterns, and risk tolerance.

Instead of staying with a traditional fully insured model, we recommended transitioning to a level-funded plan:

We also introduced a dual-option offering:

Additional enhancements:

If you’re a small or mid-sized business looking to reduce costs while enhancing coverage, we can help. Book a free strategy call with Taylor Benefits Insurance today and discover what’s possible for your team.

*Disclaimer: Client name has been changed to CloudBright for privacy. All data and outcomes are based on actual client performance and verified reporting metrics.

No, employees with higher medical needs are still protected. Level funded plans include stop loss coverage that handles large claims, so individuals are not exposed to extra costs. Coverage options, networks, and benefits remain similar to a traditional plan. Employers gain more control over plan design and can offer programs that support all employees while keeping costs predictable.

Startups should review benefits annually or whenever significant changes occur in workforce size or health trends. Regular reviews help identify cost-saving opportunities and ensure offerings remain competitive and compliant.

Wellness programs encourage preventive care and healthier habits among employees. When participation increases, companies often see fewer high cost claims and better long term health outcomes. In some cases, strong engagement in wellness initiatives also improves employee satisfaction with their benefits.

Even without claims history, insurers can offer better pricing if the company shows strong risk management practices.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066