- Providing world class service and value for employee benefit group plans since 1987

Small business health insurance plays a critical role in employee recruitment, retention, and financial security, yet it remains one of the most challenging benefits for employers with 1–50 employees to provide. Entering 2026, rising premium costs, workforce expectations, and regulatory complexity continue to shape how small businesses approach health coverage.

While large employers almost universally offer health insurance, small businesses face a more fragmented landscape in which cost sensitivity and workforce composition heavily influence benefit decisions. As a result, health insurance coverage among small employers varies significantly by company size, industry, and wage structure.

Key overview statistics for small business health insurance in the U.S.:

Only about half of U.S. small businesses offer health insurance, and the offer rate drops sharply among firms with fewer than 10 employees.

Micro businesses (1–9 employees) are the least likely to provide coverage, while offer rates increase steadily among firms with 10–49 employees.

Cost is the primary barrier to offering health insurance, cited by a majority of small business owners who do not provide coverage.

Small businesses that offer health insurance typically cover a smaller share of employee premiums than large employers, increasing employee cost exposure.

Despite lower offer rates, most U.S. workers are employed at firms that offer health insurance, reflecting the outsized role of larger employers in total employment.

Among small businesses that do offer coverage, employee participation rates vary widely, often influenced by premium affordability and plan design.

The likelihood that a small business offers health insurance increases sharply with company size, making workforce scale one of the strongest predictors of coverage availability. As of 2026, most very small employers continue to operate without a formal health plan, while coverage becomes far more common once a business reaches double-digit headcount.

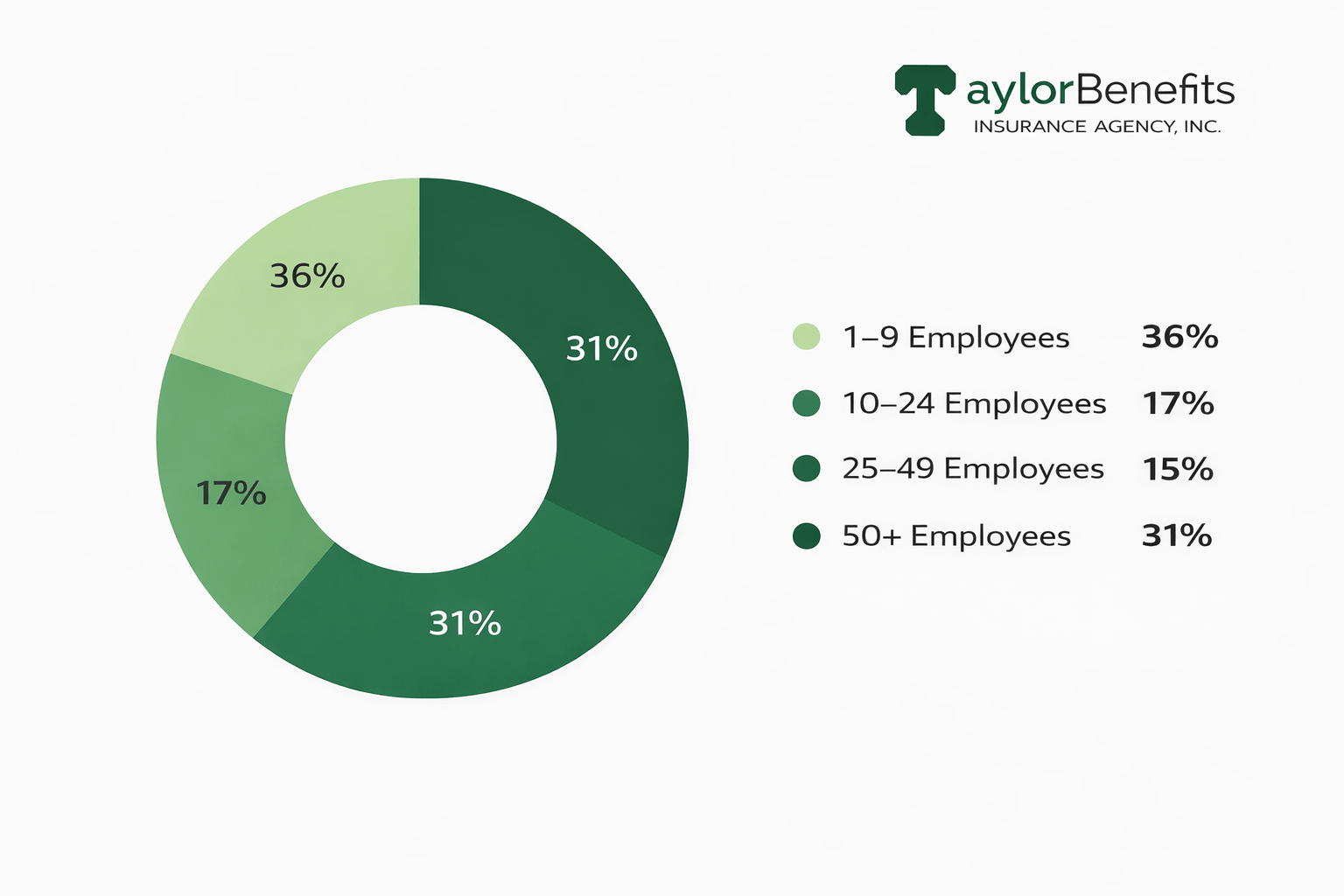

National employer benefits data shows a clear divide between micro businesses (1–9 employees) and larger small firms, reflecting differences in financial capacity, administrative resources, and workforce expectations.

Key statistics on health insurance offer rates among U.S. small businesses:

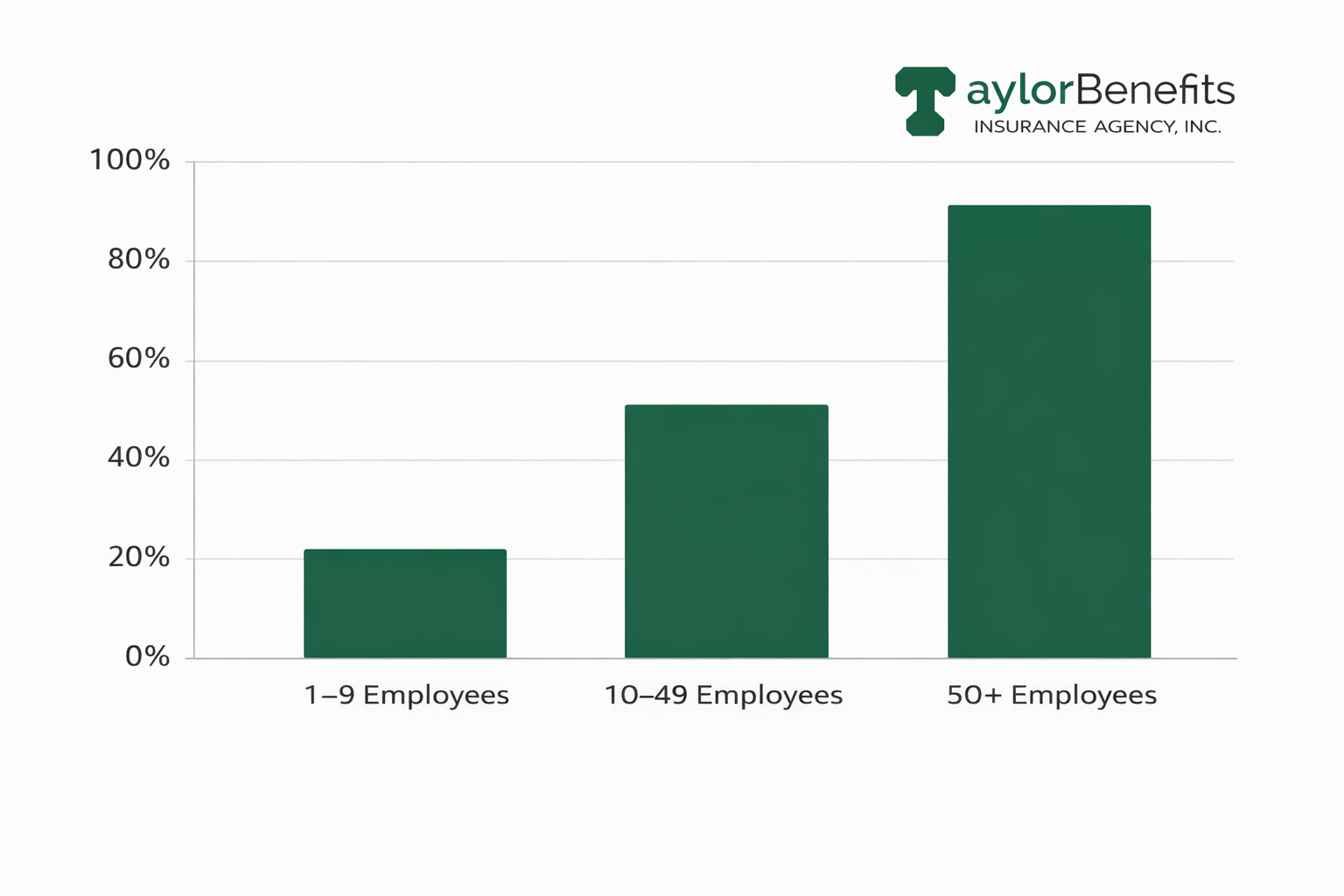

Only around one-third to two-fifths of businesses with 1–9 employees offer health insurance to workers.

Among firms with 10–24 employees, offer rates rise substantially, approaching two-thirds of employers.

Businesses with 25–49 employees show even higher adoption, with roughly three-quarters providing health coverage.

Once a business reaches 50 or more employees, health insurance becomes the norm, with more than 90% of employers offering a plan.

Across all firm sizes combined, just over half of U.S. businesses offer health insurance, reflecting the heavy concentration of very small employers nationwide.

Despite lower offer rates among micro businesses, most U.S. workers are employed at companies that do offer health insurance, due to higher employment concentration in larger firms.

Cost remains the most critical factor influencing whether small businesses offer health insurance. For employers with 1–50 employees, health coverage represents a significant and often volatile operating expense, particularly as premium growth continues to outpace general inflation.

By 26, small-business health insurance costs will reflect a combination of rising medical utilization, higher prescription drug spending, and risk-pooling challenges inherent to smaller groups. As a result, small employers typically face higher per-employee costs than large firms and shift a greater share of expenses to workers.

Key cost benchmarks for small business health insurance in the U.S.:

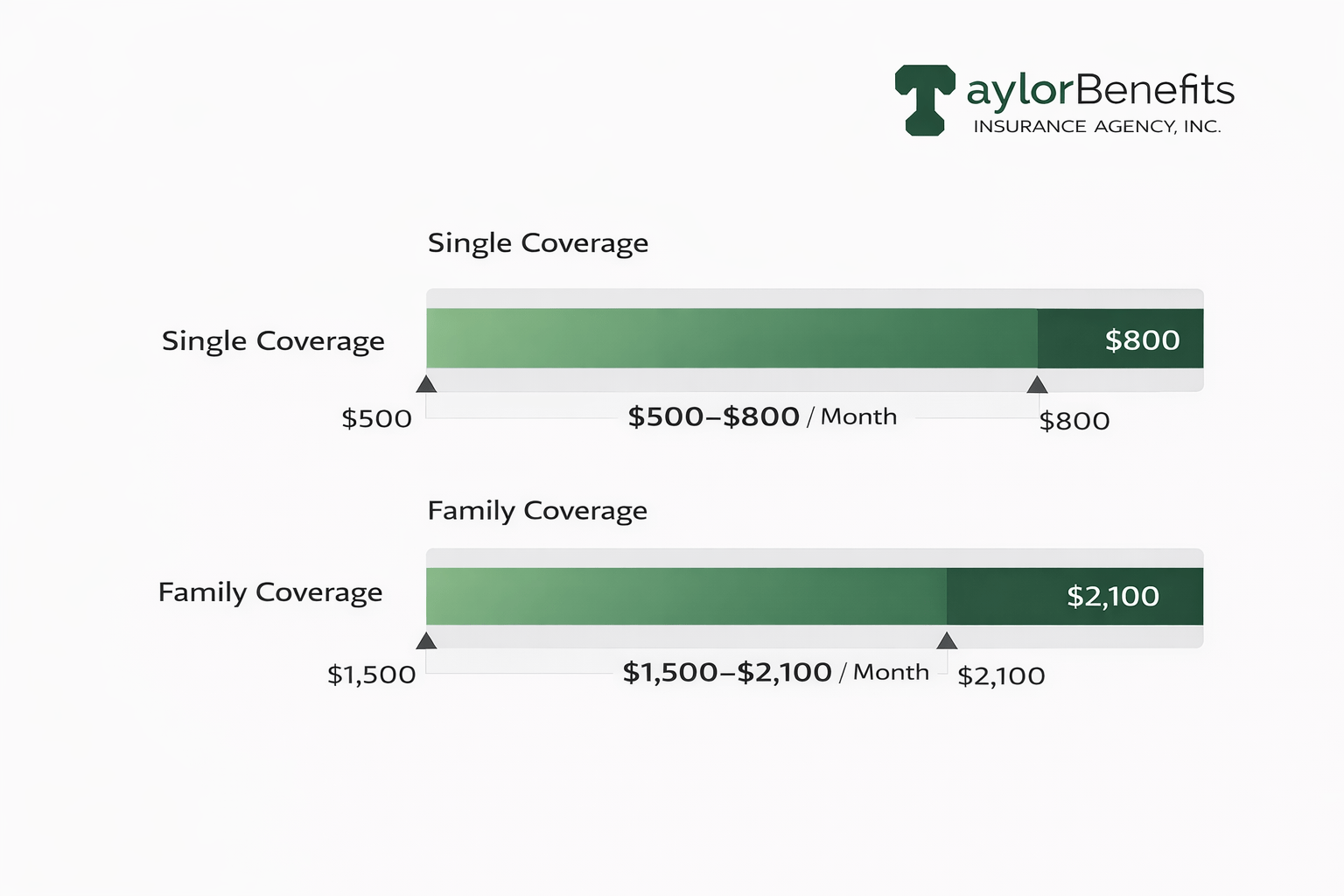

The average annual premium for small business health insurance is approximately $8,000–$9,000 for single coverage and $23,000–$25,000 for family coverage.

Small employers typically pay 60–70% of the premium, leaving employees responsible for the remaining share through payroll deductions.

Employees at small businesses pay a higher average premium share than employees at large firms, especially for family plans.

Monthly employer costs commonly range from $500–$800 per employee for single coverage and $1,500–$2,100 for family coverage, depending on plan design and region.

High-deductible health plans (HDHPs) are widely used by small businesses to lower premiums, but often result in higher out-of-pocket costs for employees.

Rising deductibles and cost-sharing have become a primary strategy for small employers seeking to control premium increases without eliminating coverage.

Small businesses tend to prioritize cost control, simplicity, and predictability when selecting health insurance plans. As a result, plan choice among employers with 1–50 employees is more limited than at larger companies, with most small firms offering a single plan option rather than multiple tiers.

By 2026, plan selection trends indicate a clear preference for flexible network designs and higher deductibles, allowing employers to manage premiums while still offering comprehensive coverage.

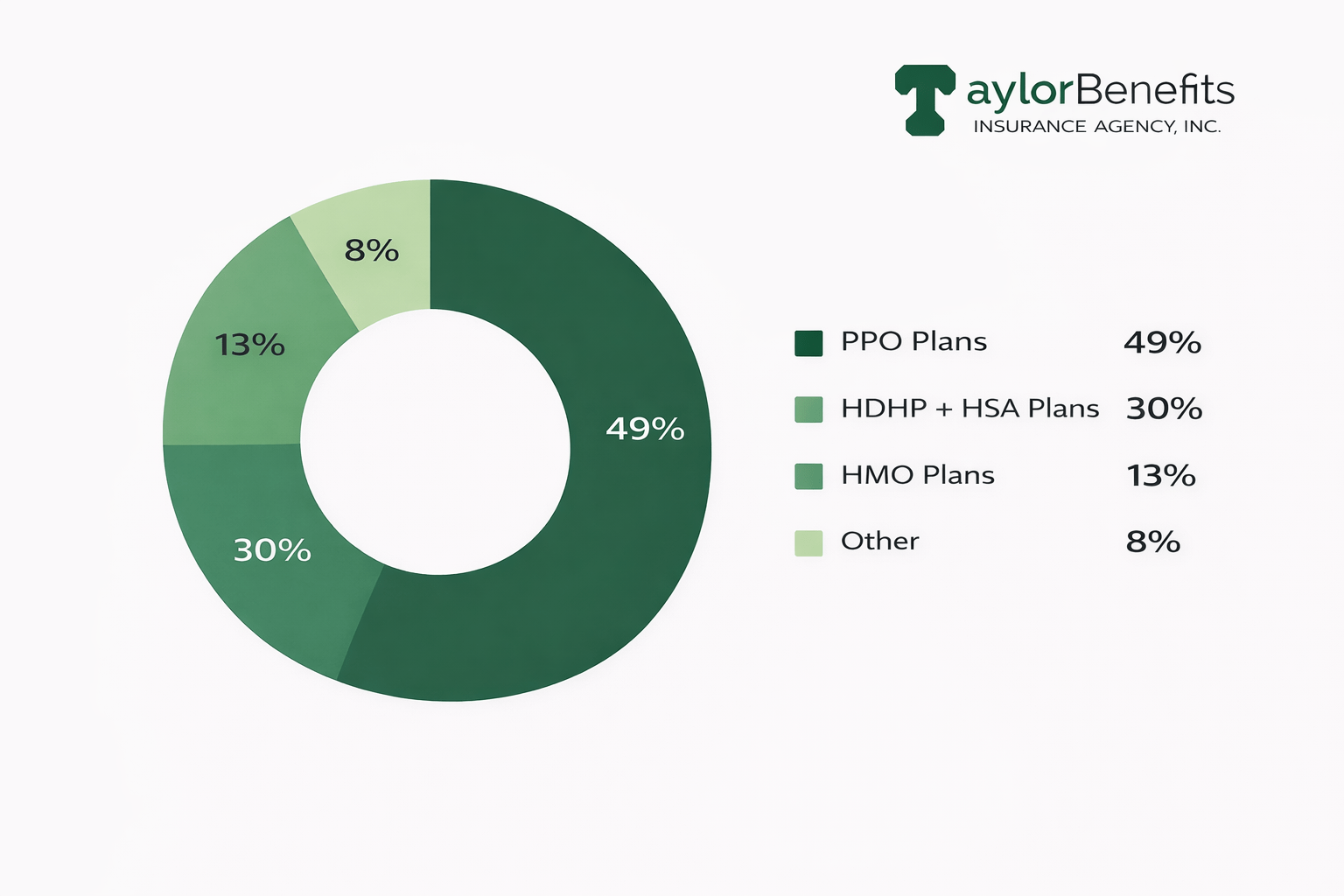

Key health plan types used by small businesses in the U.S.:

Preferred Provider Organization (PPO) plans remain the most common option, valued for network flexibility and out-of-network access.

High-Deductible Health Plans (HDHPs) are widely adopted by small employers to lower monthly premiums, often paired with Health Savings Accounts (HSAs).

Health Maintenance Organization (HMO) plans are used less frequently but appeal to cost-sensitive employers in regions with strong provider networks.

The majority of small businesses that offer health insurance offer only one plan, limiting employee customization.

Fully insured plans continue to dominate the small-group market, particularly among businesses with fewer than 20 employees.

Level-funded and partially self-funded plans are increasingly explored by larger small businesses seeking more control over claims costs.

Plan design decisions are often driven by premium affordability first, with deductibles and cost-sharing used to offset rising insurer rates.

Offering health insurance does not guarantee that employees will enroll. Among small businesses, eligibility rules, premium affordability, and plan design all influence workers’ participation in employer-sponsored health plans. As of today, participation rates remain meaningfully lower at small firms than at large employers.

For businesses with 1–50 employees, understanding participation dynamics is critical, as low enrollment can reduce the perceived value of offering coverage while still carrying administrative and compliance costs.

Key participation and eligibility statistics for small business health insurance:

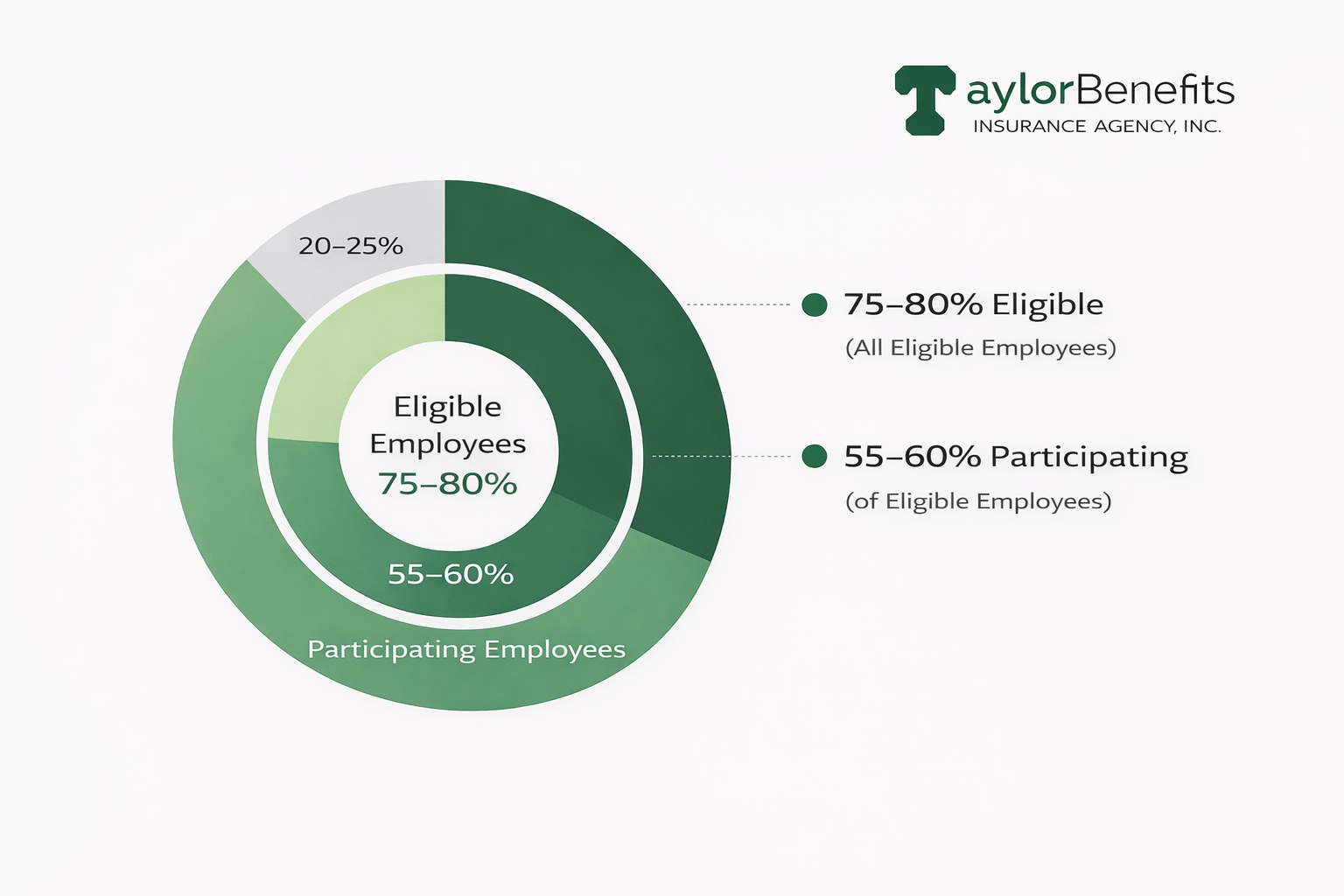

On average, about 75–80% of employees are eligible to enroll in health insurance at firms that offer coverage.

Of eligible employees, roughly three-quarters choose to enroll, leaving a sizable minority who decline employer-sponsored plans.

Participation rates are lowest among tiny businesses, where higher employee premium shares discourage enrollment.

Employee premium cost is the most common reason workers decline coverage, particularly for family plans.

Workers at small firms are more likely to opt out of employer coverage due to alternative coverage, such as a spouse’s plan or individual marketplace insurance.

High deductibles and cost-sharing requirements further reduce participation, even when monthly premiums are lower.

Small employers frequently report wide variation in participation, with some plans covering most employees and others enrolling fewer than half.

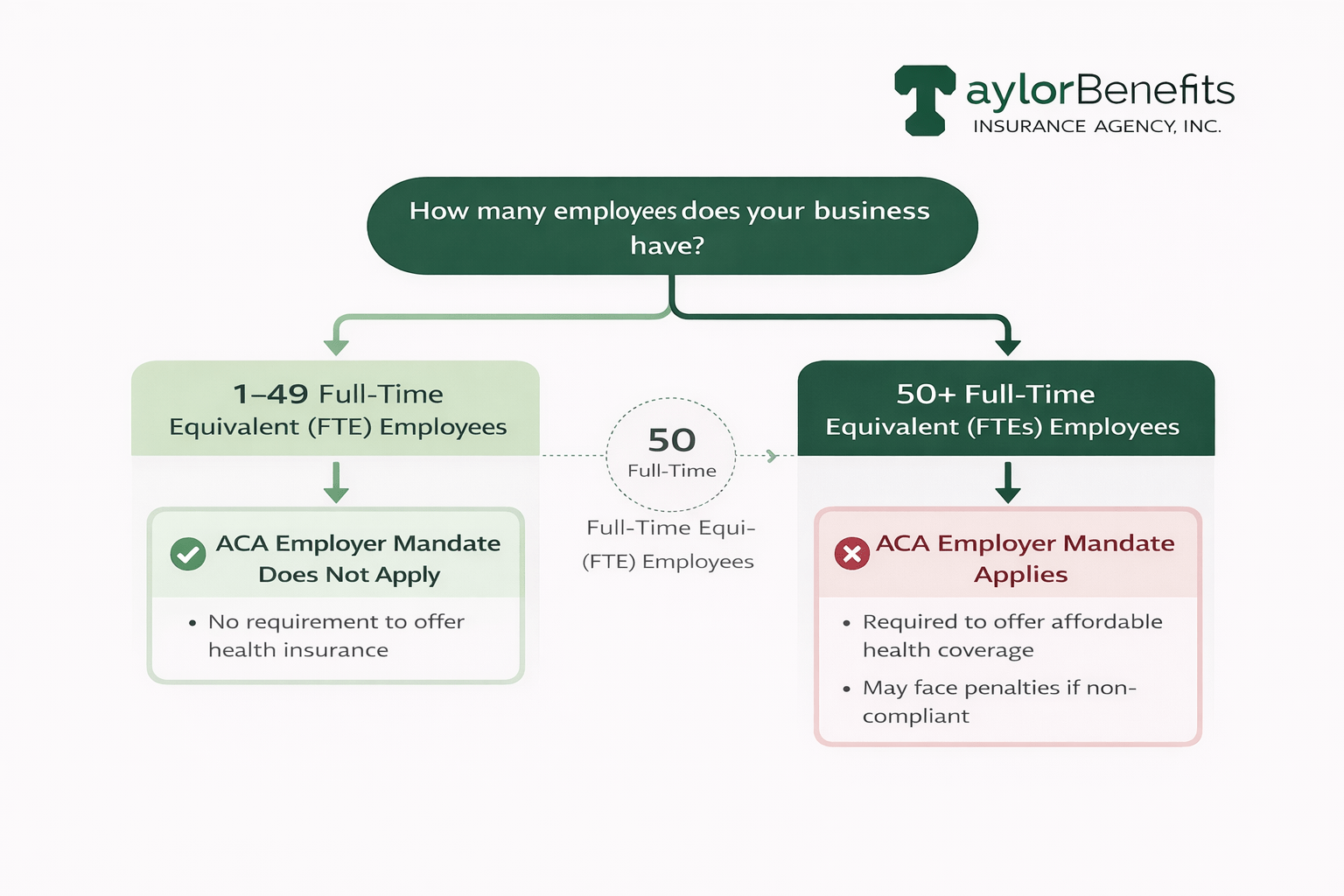

The Affordable Care Act (ACA) applies differently to small businesses depending on employee count, making company size the most critical compliance factor. As of 26, most small employers are not legally required to offer health insurance, but those near key thresholds must understand their obligations to avoid penalties and compliance issues.

For many small businesses, confusion around ACA rules continues to influence benefit decisions, even when no mandate applies.

Key ACA compliance facts for small business health insurance:

Businesses with fewer than 50 full-time equivalent (FTE) employees are not subject to the ACA employer mandate and face no penalties for not offering health insurance.

The employer mandate applies only to Applicable Large Employers (ALEs) with 50 or more FTEs, requiring them to offer affordable, minimum-value coverage to full-time employees.

Small businesses that do offer health insurance must still comply with ACA consumer protection rules, including coverage of essential health benefits and prohibition of pre-existing condition exclusions.

Small-group health plans are subject to community rating rules, limiting how much premiums can vary by age and other factors.

The SHOP marketplace, initially designed for small employers, has seen minimal adoption and is no longer a primary purchasing channel in most states.

Employers offering coverage must observe maximum waiting periods, generally limited to 90 days for new employees.

Small businesses using self-funded or HRA-based arrangements must meet specific reporting and documentation requirements, even if exempt from the employer mandate.

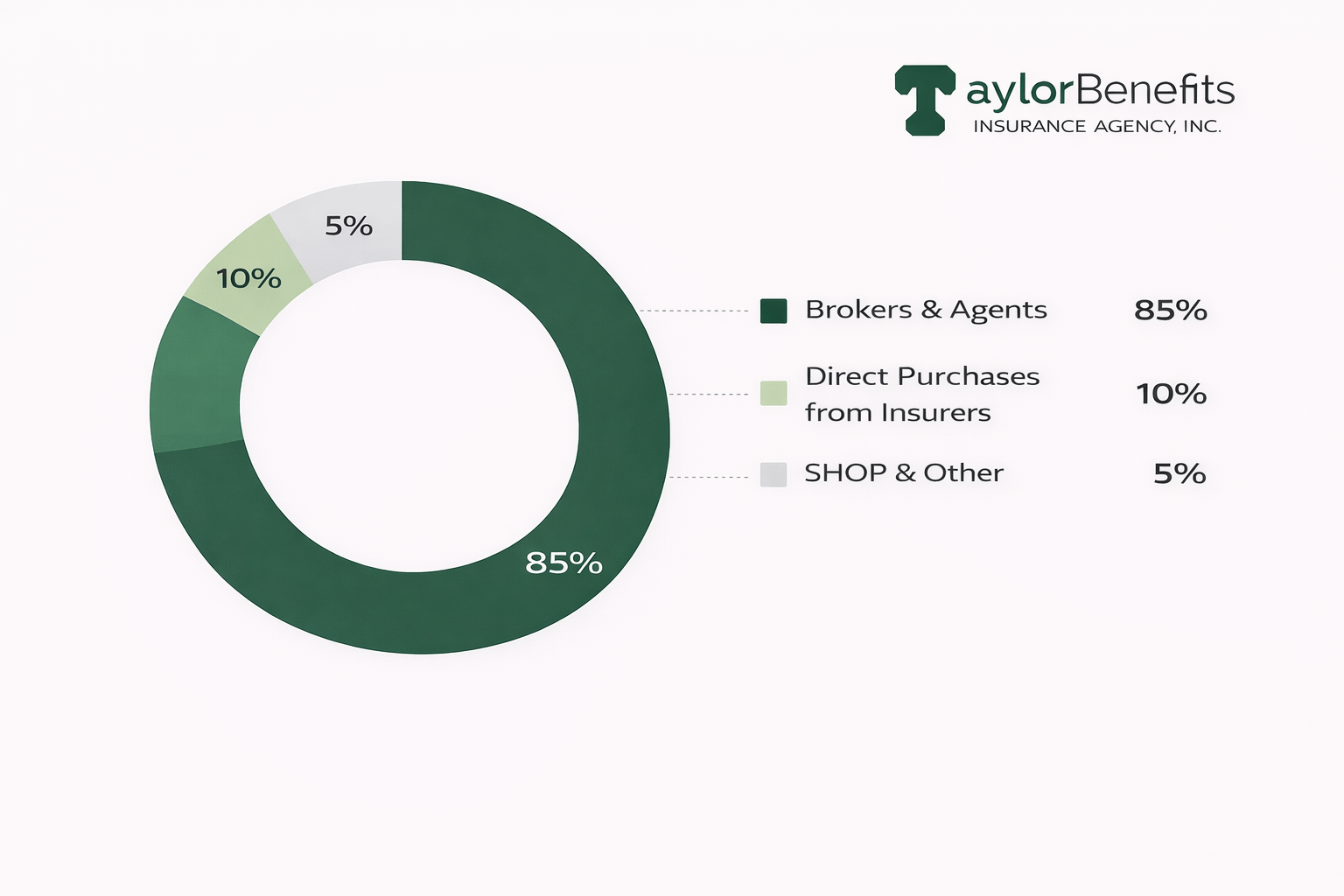

For most small employers, how health insurance is purchased is just as important as which plan is selected. As of 2026, small businesses overwhelmingly rely on insurance brokers and agents to navigate plan selection, pricing, and compliance, rather than purchasing coverage directly from insurers or government marketplaces.

The complexity of plan options, renewal negotiations, and regulatory requirements has reinforced the role of intermediaries in the small-group health insurance market.

Key purchasing trends for small business health insurance:

The vast majority of small businesses use insurance brokers or agents to purchase and renew health insurance coverage.

Brokers remain the preferred channel due to their ability to compare multiple carriers, explain plan differences, and manage annual renewals.

Direct purchasing from insurers without broker assistance is relatively uncommon among small employers.

The SHOP marketplace has failed mainly as a purchasing channel and is no longer widely used by small businesses in most states.

Small businesses near the 50-employee threshold often seek professional guidance to manage ACA compliance risk.

Some small firms use professional employer organizations (PEOs) and group associations, but adoption remains limited compared to traditional broker-led purchasing.

As plan complexity and costs increase, advisor-led decision-making continues to dominate small business health insurance purchasing behavior.

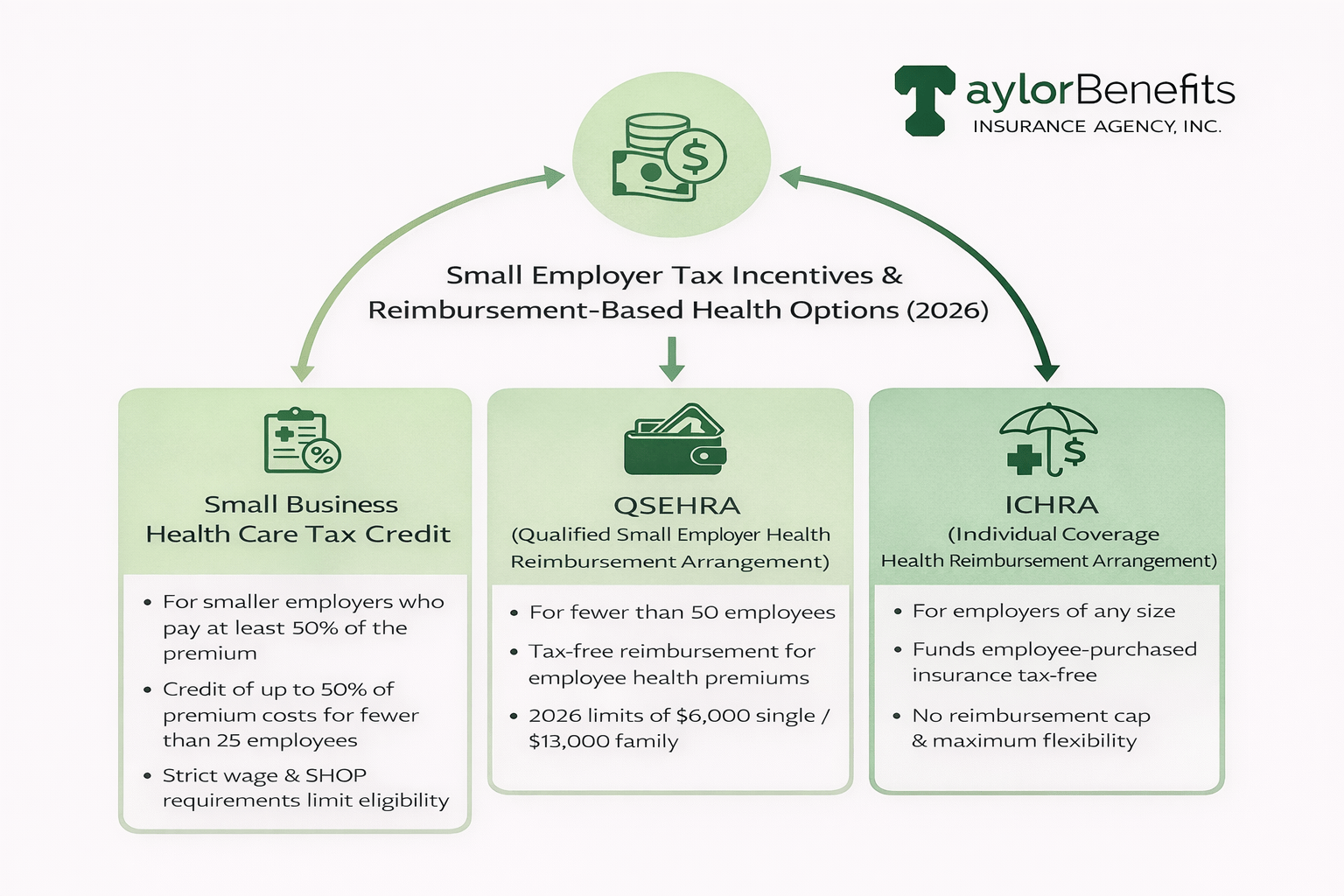

In response to rising health insurance costs, many small businesses explore tax incentives and reimbursement-based alternatives to traditional group health plans. As of 2026, these options play a growing role in how employers with fewer than 50 employees support employee health coverage while maintaining budget control.

Rather than replacing group insurance entirely, these programs offer flexible paths for businesses that cannot afford or do not qualify for traditional plans.

Key tax and reimbursement options available to small businesses:

The Small Business Health Care Tax Credit allows eligible employers with fewer than 25 employees to claim a credit of up to 50% of premium costs. However, strict wage and SHOP marketplace requirements limit adoption.

QSEHRA (Qualified Small Employer Health Reimbursement Arrangement) enables businesses with fewer than 50 employees to reimburse workers tax-free for individual health insurance and medical expenses.

For 2026, QSEHRA annual reimbursement limits exceed $6,000 for single coverage and $13,000 for family coverage, adjusted annually for inflation.

ICHRA (Individual Coverage Health Reimbursement Arrangement) allows employers of any size to fund employee-purchased individual insurance with no fixed reimbursement cap.

HRAs give employers predictable, defined costs, shifting plan choice to employees while maintaining tax efficiency.

Adoption of reimbursement-based models remains highest among tiny businesses that previously offered no group coverage.

While HRAs increase flexibility, they also require careful compliance and documentation, particularly when coordinating with ACA affordability rules.

The outlook for small business health insurance beyond 2026 is shaped by continued cost pressure, evolving workforce expectations, and increasing interest in flexible benefit models. While traditional group health insurance remains the dominant option, small employers are adapting how they structure and fund coverage.

Rather than broad expansion or contraction, the market is expected to see incremental shifts toward predictability, cost control, and employee choice.

Key trends shaping the future of small business health insurance:

Health insurance costs are expected to continue rising, reinforcing affordability as the primary constraint for small employers.

Defined-contribution approaches, including QSEHRAs and ICHRAs, are likely to gain adoption as businesses seek budget certainty.

Employee expectations around benefits remain high, particularly in competitive labor markets, making health insurance a retention tool even for tiny teams.

High-deductible plans and cost-sharing strategies will continue to be used to offset premium growth.

Broker and advisor guidance is expected to remain central, as plan complexity and compliance considerations increase.

Technology-enabled enrollment, virtual consultations, and digital plan management are improving efficiency for small employers.

Regulatory stability around ACA small-group rules provides predictability, though future policy changes remain a long-term variable.

Businesses with 50 or more employees are more likely to provide insurance because larger groups get better rates and are often required to offer coverage under federal law. Very small businesses face higher per-employee costs.

Some very small firms may reconsider offering coverage because of rising costs, but most continue to offer at least basic plans. Many owners adjust contributions or plan types instead of eliminating benefits completely to retain employees.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066