- Providing world class service and value for employee benefit group plans since 1987

Getting proper medical care could be very expensive and may not be in reach for every citizen. Thus, as a result of not affording proper medical care, consequences could be severe. Hence, in 2010, under the Affordable Care Act (ACA) Health Insurance Marketplace was established. It is a life-changing platform that provides millions of Americans with the ability to access high-quality health insurance at a low cost.

Marketplace allows such an easy way to compare and purchase insurance when you do not have insurance, are changing jobs, or just want to have better offers than employer-sponsored insurance. This guide provides an explanation of what Marketplace health insurance is, how it operates, and how to enroll, making sure you know everything about it in 2025. We will address everything you need to know to make smart decisions on your health care, including who is eligible as well as how to utilize subsidies.

What does Health Insurance Marketplace mean? The health insurance marketplace is an online marketplace in which people can compare and buy personal health insurance plans according to the ACA regulations. It was created in order to simplify things and make them open. It ensures that strategies cover valuable health benefits and do not discriminate against persons with pre-existing diseases. In 28 states, HealthCare.gov is federally-run, and in 20 states have their own marketplace, such as California or NY State of Health, that is designed to meet the needs of residents.

The Marketplace is not a monolith, but a regulated market in which numerous insurance companies deal with identical products. They are divided into four metal levels: Bronze, Silver, Gold, and Platinum, depending on the amount paid by each individual. For example:

Some of the main benefits are:

Take an example, a Texas-based freelance graphic designer unable to obtain Medicaid can use HealthCare.gov to select a Silver plan with subsidies that will suit them and will not be costly.

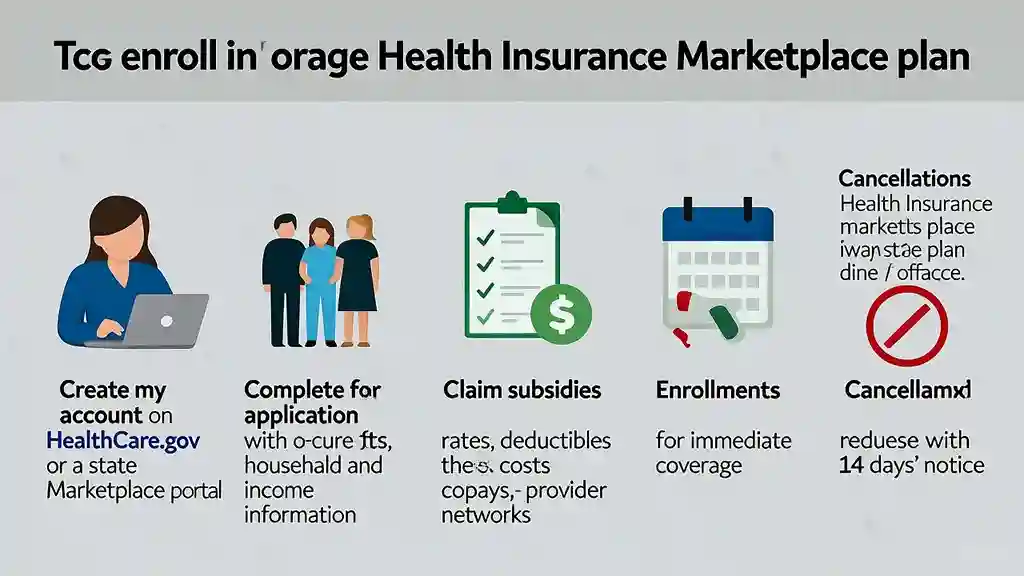

With the help of the health insurance marketplace, it is possible to read, compare, and enroll in health plans easily. Signing up would be the easiest option by using HealthCare.gov or the state website. To receive individual plan recommendations, you will be required to provide details regarding your household size, income, and existing coverage.

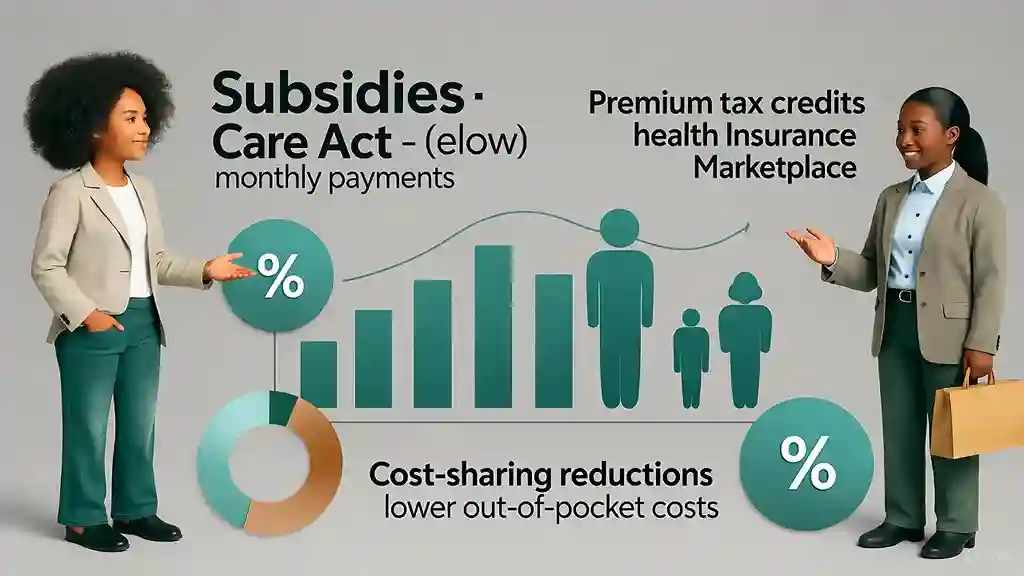

The system determines the eligibility of persons for subsidies such as premium tax credits (by reducing monthly payments) or cost-sharing (by reducing deductibles and copays). These can be afforded by even low-income earners.

The steps are as follows:

The Marketplace also allows individuals to apply to Medicaid/CHIP throughout the year and Special Enrollment Periods related to qualifying events like a baby’s birth and relocation to make sure the coverage remains current. In case you relocate to Florida in the middle of the year, say in California, you can enroll in a new plan within 60 days, and this way, you are not left without a plan.

It is simple to obtain coverage through the health insurance marketplace. You are able to explore many options without making any commitment with HealthCare.gov. All you need to prepare a list of relevant documents, such as your Social Security number, recent tax filings, W-2 forms, and details on any existing employer-sponsored coverage. The software will assist you in determining the cost, file subsidies, and complete your registration. In this manner, you will be able to select the plan that suits you well within your health and financial requirements.

How to sign up:

What is open enrollment for Marketplace health insurance? As of 2026, it will be covered in the majority of states within the period between November 1, 2025, and January 15, 2026. Did you miss this window? Special Enrollment Periods can be signed up for in case something occurs in your life, such as marriage or loss of employment.

Who is eligible for Health Insurance Marketplace coverage? The Marketplace is free to all, although there are but a few rules:

One could be the example of a single mom in Colorado, who earns 30,000 a year, being able to afford a Silver plan with a subsidy and a consultant, who has a high fortune, being able to afford an unsubsidized Platinum one, which would take care of everything.

How to apply for Marketplace health insurance? The enrollment process can be easily understood and accommodate a number of needs:

Take an example, A couple in Ohio with an unborn baby may enroll in an open enrollment plan, the Gold plan. In case they get an increment at work, they are able to change their plan during the mid-year.

Follow these useful tips in order to maximize the value of the Health Insurance Marketplace ®:

Yes, subsidies are such a large component of the Marketplace that enable coverage. The premium tax credits reduce your monthly payment. You may either use them on the spot on your plan, or you can claim them on your tax return. The reduction of cost sharing includes deductibles, copays, and out-of-pocket maximum, mainly in Silver plans. As a rule, your income should range between 100% and 400% of the federal poverty line ($14,580-$58,320 an individual in 2025). However, now, there is the possibility that higher income earners can be assisted with the help of new laws like the Inflation Reduction Act.

How much is Marketplace health insurance? The prices vary depending on the plan, age and where one resides, and income earned. In 2025, an average 40-year-old will spend an average of $486 a month on an unsubsidized Silver plan, but households eligible will receive subsidies to reduce this to $0-$200. An example is that a family of four in Florida with earnings of $45,000 can spend $150 a month on a Silver plan after credits, compared to $600 a month without assistance.

All Marketplace plans cover 10 significant health benefits, ensuring that you are well covered:

Look into the provisions of the plan in detail since it might provide some additional benefits, such as telemedicine or gym memberships.

You can apply in several ways:

| Application Method | Pros | Cons | Best For |

| Online (HealthCare.gov) | It is quick, 24/7 available, and easy. | Internet and technology skills are required. | Fast-paced technology users, fast applications. |

| POS (1-800-318-2596) | You can get support in multiple languages | Wait time potentials under open enrollment. | Wait time potentials under open enrollment. |

| No technology required, easily available. | Delay of processing, delay of mails. | Residents of rural areas, people who are not fond of technology. | |

| In-Person | Customized service to complicated cases. | May require appointments or travel | Exceptional conditions, language interferences. |

The Health Insurance Marketplace is a terrific option to obtain quality and inexpensive full health insurance in 2025. To find health insurance that fits your needs and your budget, you can learn to apply to Marketplace health insurance, use subsidies, and compare the plans on HealthCare.gov. It is always better to begin the search now, to be sure that you will be well in your health and your finances.

If you move to a new state, your current Marketplace plan will no longer be valid. You can enroll in a new plan in your new state through a Special Enrollment Period. Make sure to notify the Marketplace of your address change and choose a plan before your current coverage ends to avoid any gaps. Coverage options and costs may be different in your new state, so review them carefully.

Individual ACA-compliant plans purchased in the Marketplace provide you with the basics and coverages as a consumer.

Go to HealthCare.gov and select your plan and request to terminate it with a 14-day notice. Other coverage is needed to cover the gaps.

Yes, but you will not receive any refund of the amount you paid earlier in premiums, and will only be re-enrolled during open enrollment or after a qualifying event.

Unsubsidized Silver plans will have an average cost of 486 per month in 2025, but with subsidies, the price is likely to drop to 0 -200 based on income.

No, it is commercial insurance; however, the Marketplace application will check to determine whether you are eligible to receive Medicaid or CHIP.

The Marketplace offers four main plan categories: Bronze, Silver, Gold, and Platinum. Each category varies in monthly premium costs, out-of-pocket expenses, and coverage levels, allowing individuals and families to choose plans that best suit their healthcare needs.

Coverage start dates depend on when you enroll. If you sign up during open enrollment, coverage typically begins at the start of the new plan year. During a special enrollment period, coverage usually starts the first day of the following month after your application is completed.

Income changes can raise or reduce your subsidy amount so reporting updates quickly helps keep premiums accurate If not updated you may owe money later or miss savings available during enrollment period coverage adjustments apply.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066