- Providing world class service and value for employee benefit group plans since 1987

Large group health insurance remains the backbone of coverage for millions of American workers. With rising premiums, shifting compliance requirements, and an ongoing debate over affordability, understanding the latest trends is critical for employers and HR leaders. This dataset-style roundup compiles the most authoritative sources — from the Kaiser Family Foundation, the U.S. Department of Labor, and other leading institutions — into one comprehensive resource for 2025–2026.

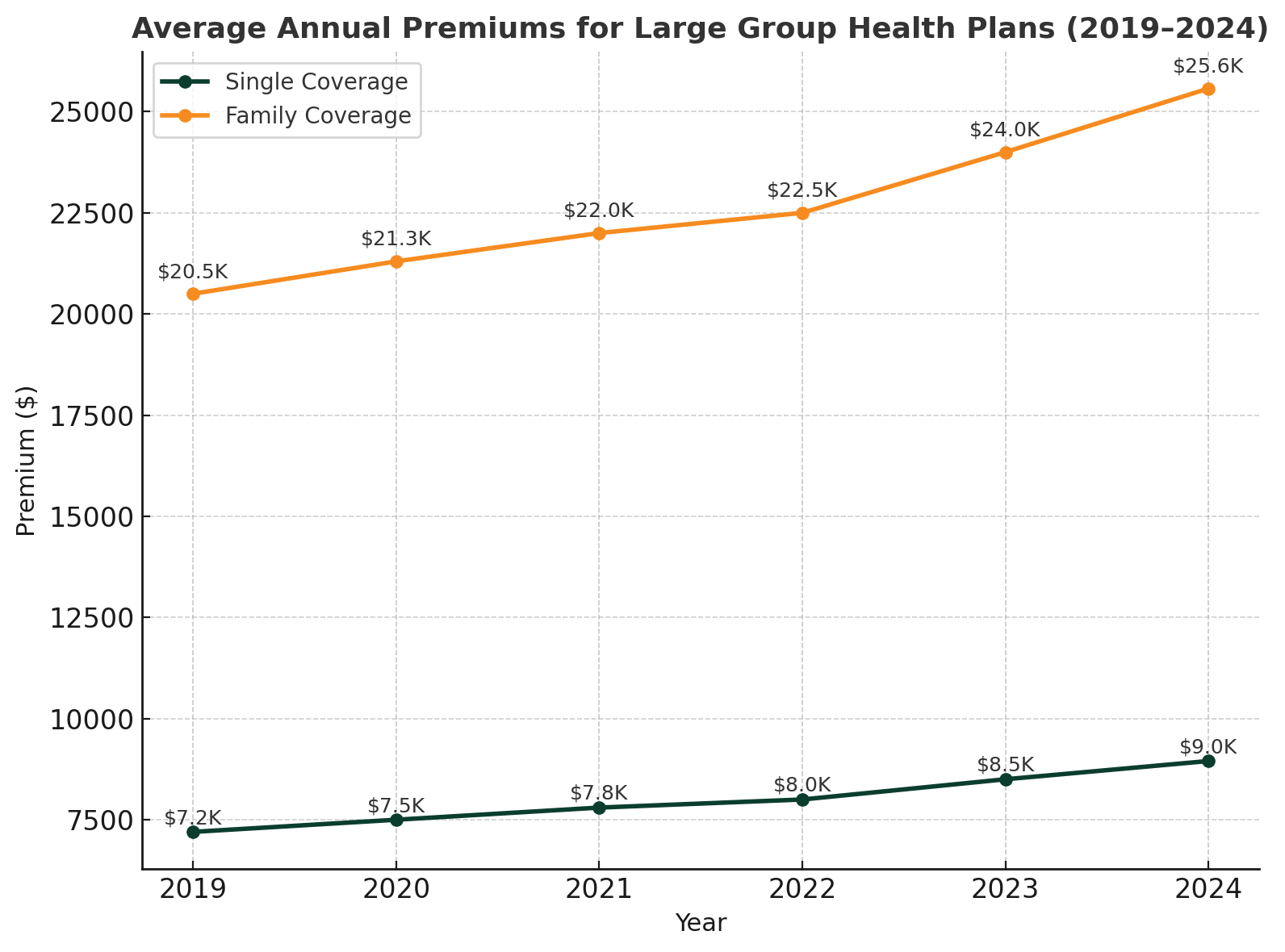

The cost of health insurance continues to rise for large employers. In 2024, the average annual premium reached $8,951 for single coverage and $25,572 for family coverage, reflecting year-over-year growth of 6–7% (KFF).

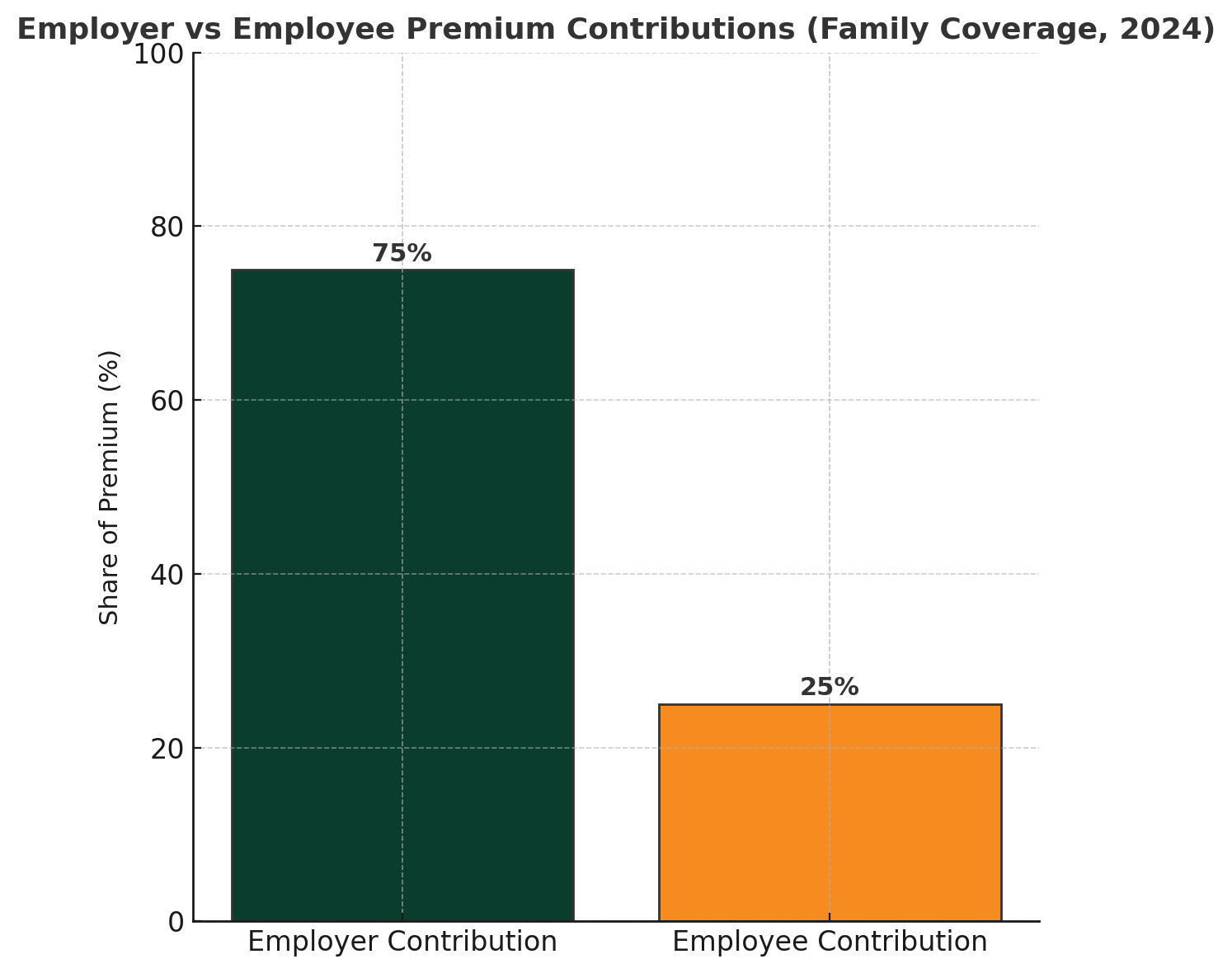

Employers cover the majority of costs, but workers still contribute significantly. Employees typically pay 16% of single premiums and 25% of family premiums on average.

At large firms, employees pay less out-of-pocket: about 23% of family premiums, compared with 33% at small firms.

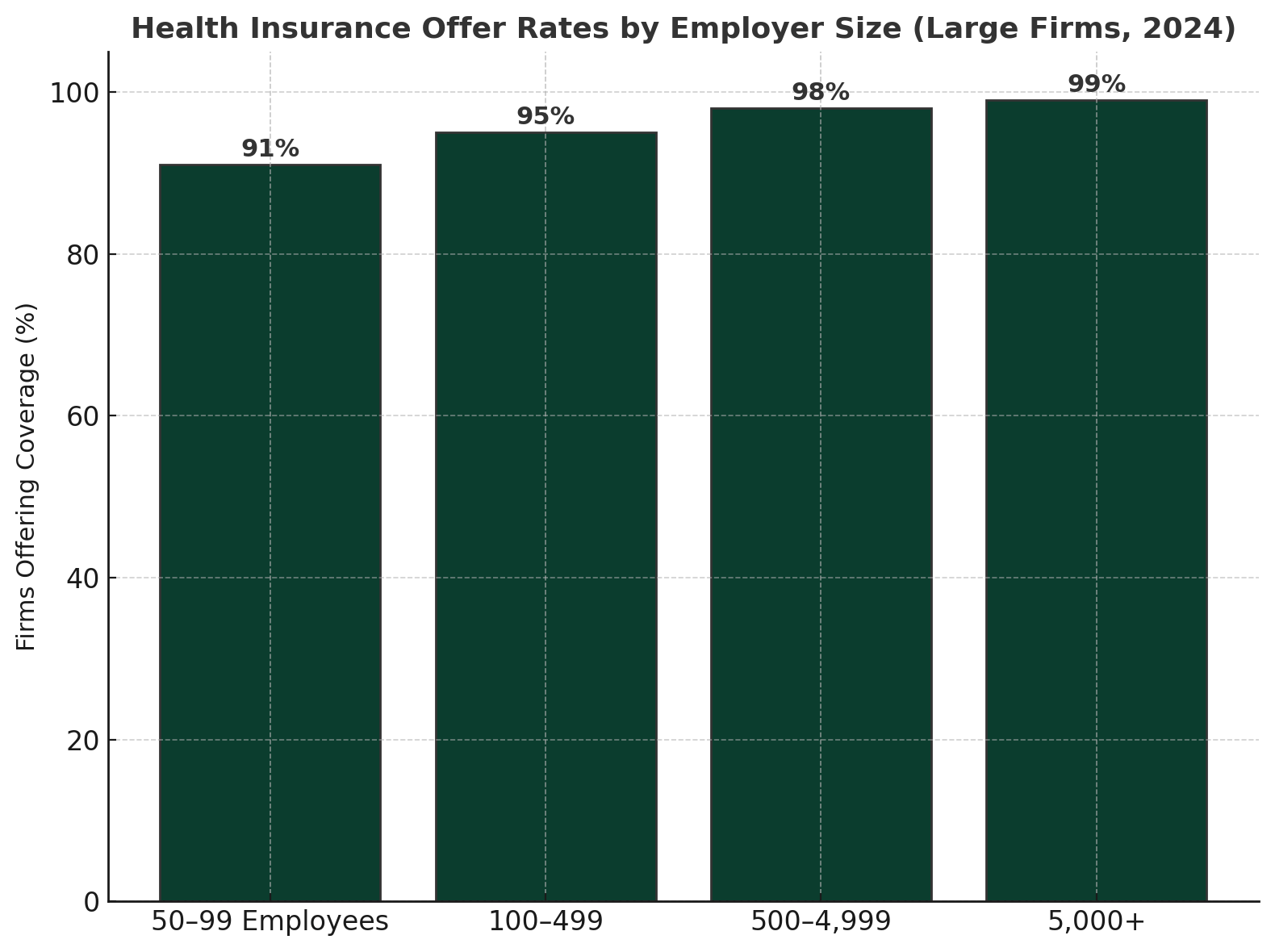

Virtually all large employers offer coverage. In 2023, 94% of firms with 50+ employees provided health benefits (KFF).

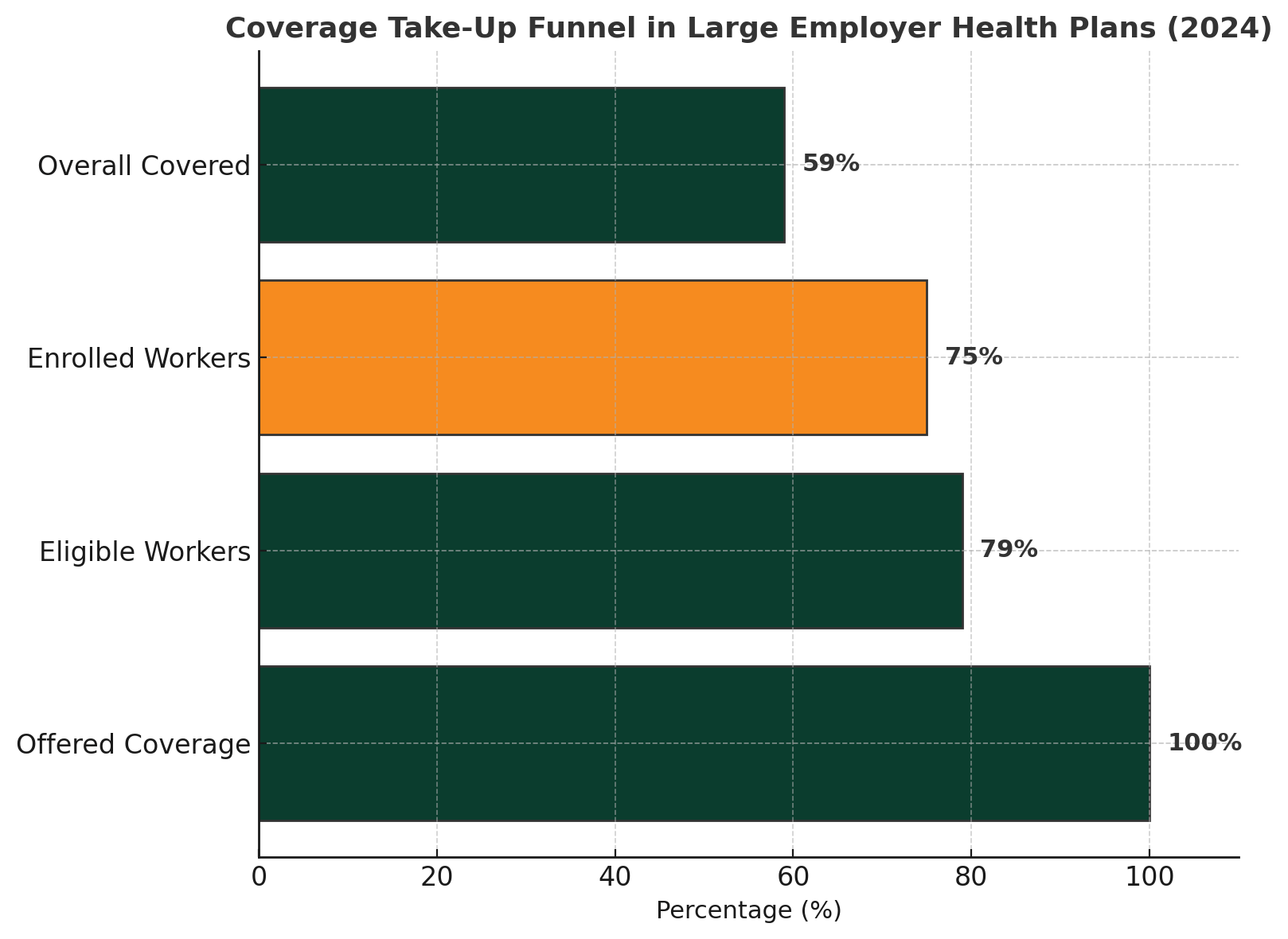

Among workers at offering firms, 79% are eligible, and of those, 75% enroll, resulting in a 59% coverage rate overall.

Accounting for firms that don’t offer, about 53% of the total U.S. workforce is covered by their employer’s health plan.

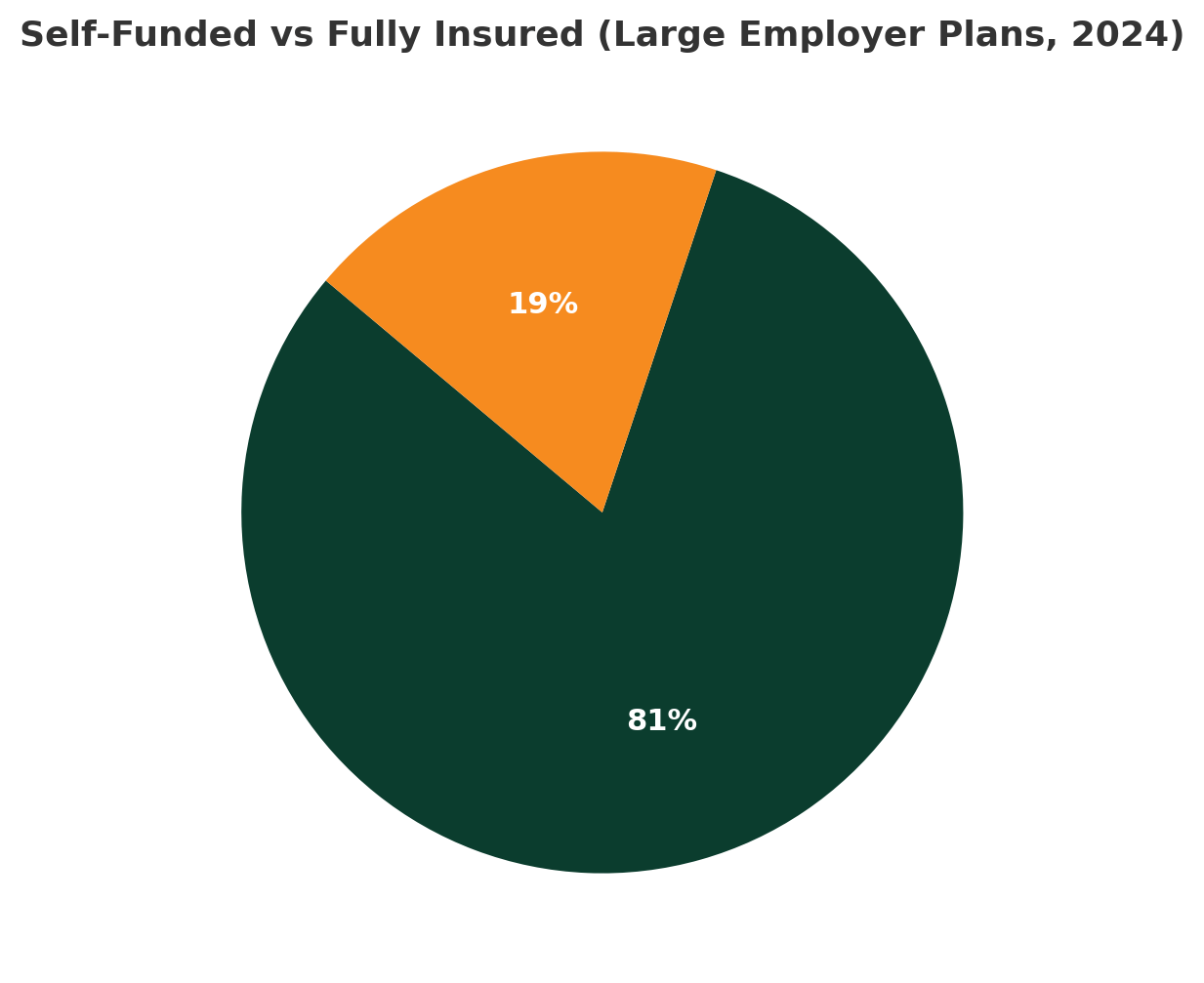

Self-funding dominates the large employer market. According to the Department of Labor, more than 80% of workers at large firms are in self-funded plans, compared to fewer than half at small firms (DOL).

Among employers with 5,000+ employees, 90% self-insure.

Smaller large employers (100–199 workers) are less likely, with only about 27% self-insuring.

Stop-loss insurance protects self-funded plans from catastrophic claims. Roughly 67% of covered workers in self-funded large firm plans are backed by stop-loss coverage (KFF).

Mid-size large firms (200–4,999 workers) have 90%+ adoption rates.

Jumbo firms (5,000+ workers) are less likely, with just 53% using stop-loss.

Large employers remain under pressure to comply with ACA, ERISA, and parity laws.

The ACA employer mandate ensures that nearly all firms with 50+ employees provide affordable coverage. In 2025, penalties for non-compliance are set at $2,960 per employee annually, rising to $3,340 in 2026 (IRS).

Enforcement of the Mental Health Parity and Addiction Equity Act intensified in 2023, with the Department of Labor citing multiple plans for violations (DOL).

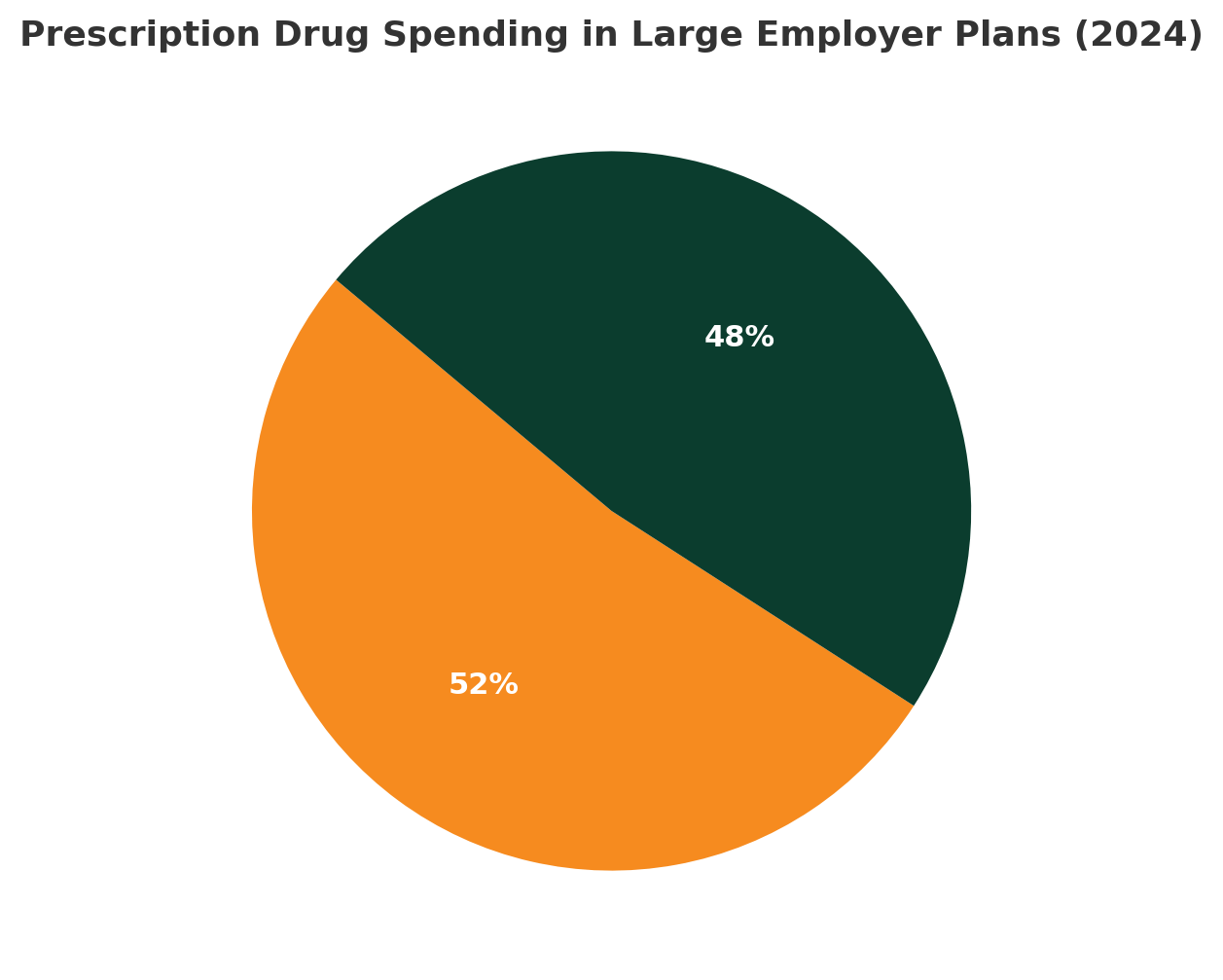

Pharmacy costs are now one of the fastest-growing components of large group health plans.

Employers report that 24–27% of total health plan spending goes to prescription drugs, up sharply in recent years (Business Group on Health).

Specialty drugs account for 50%+ of pharmacy spending, even though they represent a small share of prescriptions.

Telehealth has become a permanent fixture in employer benefits. By 2023, 97% of large firms offered telehealth or telemedicine services (KFF).

Telehealth is most used for behavioral health, routine primary care, and chronic disease management.

Many employers now offer $0 copays for telehealth visits to encourage adoption.

Employer size influences plan design and funding.

Self-funding: Only 27% of firms with 100–199 employees self-insure, compared to 90% of firms with 5,000+ employees (DOL).

Premiums: Premiums are similar across sizes, but large firms contribute more toward family coverage, making employee costs lower.

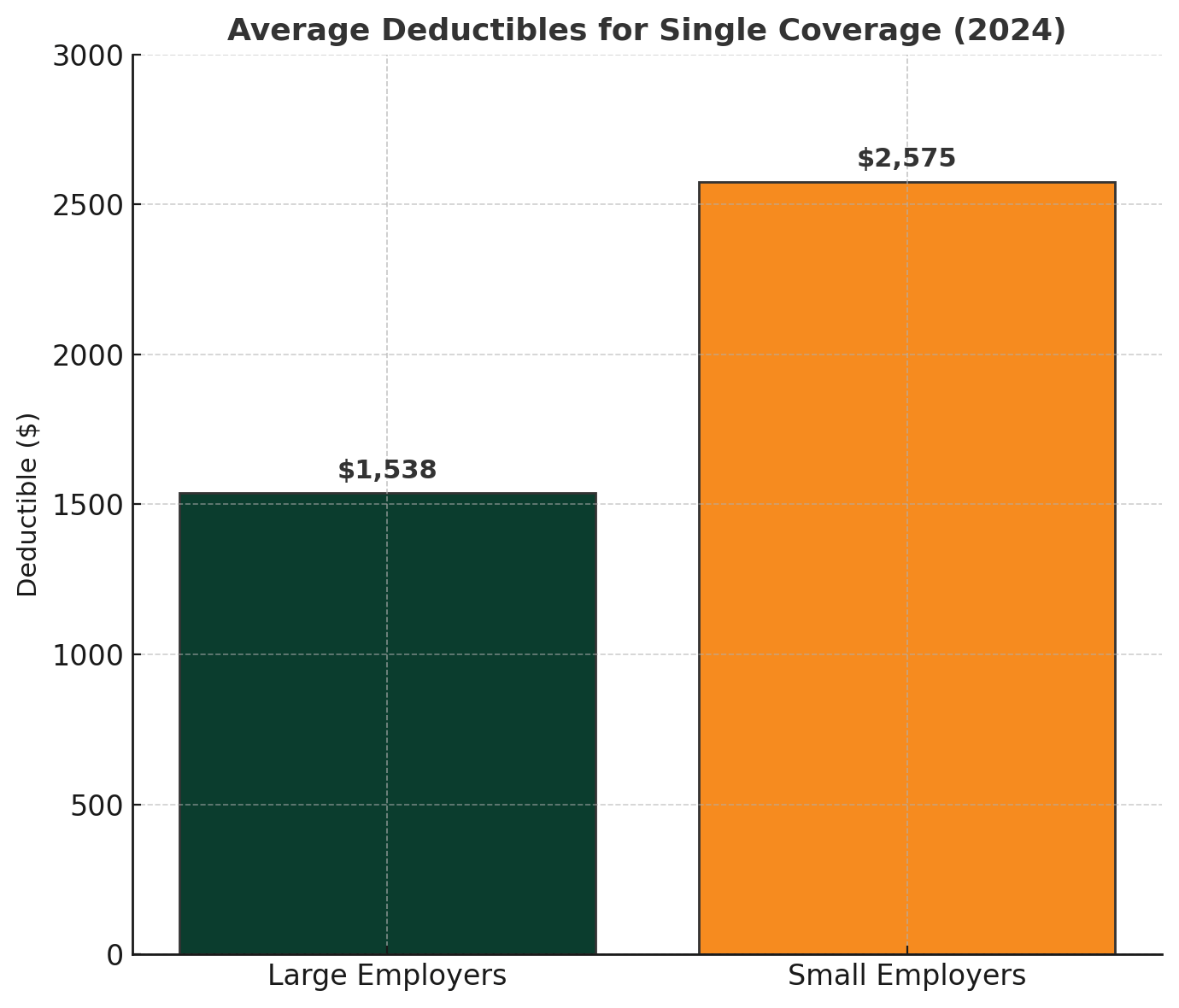

Employees at large firms face rising deductibles, though still lower than small firms.

The average deductible in large employer plans is $1,538 for single coverage, compared to $2,575 at small firms (KFF).

About 25% of large firm workers have deductibles above $2,000, versus 33% at small firms.

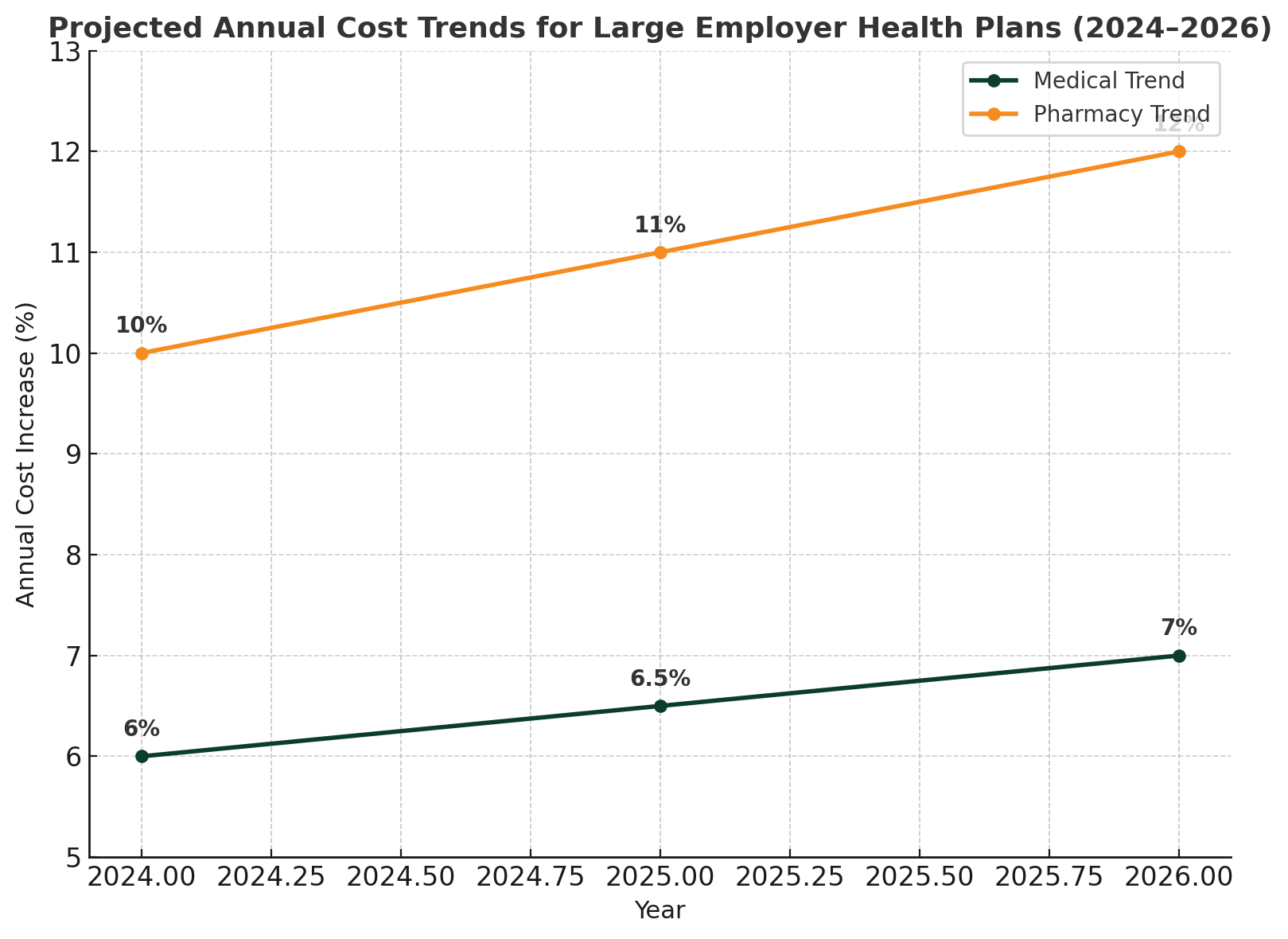

Employers anticipate rising health costs and a greater focus on affordability.

Pharmacy costs are projected to increase 11–12% annually through 2026, driven by specialty drugs and new therapies (Mercer).

Employers are also expanding mental health coverage, telehealth, and value-based cost-sharing to address employee affordability.

Large group health insurance plans are evolving under the weight of rising premiums, specialty drug spending, and stricter compliance oversight. Employers are adapting through self-funding, telehealth expansion, and cost-sharing innovations. For HR teams and business leaders, staying ahead of these trends is crucial to striking a balance between affordability and compliance.

As employees get older and more have chronic conditions, health care usage increases, which can drive up premiums. Employers often respond by adjusting plan design, such as introducing higher deductibles, offering wellness programs, or creating networks that focus on quality and cost efficiency. Managing these demographic trends helps keep plan costs more predictable.

Large employers often prefer self‑funded plans because they gain more control over plan design and costs and can benefit from risk‑sharing arrangements directly. This trend is especially strong among very large companies, where most covered workers are in self‑funded arrangements.

Prescription medications make up a significant portion of employer health spending. In many large group plans, about one quarter of total healthcare costs are related to pharmacy benefits. Specialty drugs account for a large share of these expenses despite being used by a smaller number of patients.

Recent statistics show rising premiums, increased employer spending, and growing use of self-funded plans among large organizations. Prescription drug costs and chronic conditions are driving much of the overall increase in healthcare spending.

HR departments often monitor enrollment rates, employee participation, claims costs, average premium increases, prescription drug spending, absenteeism, preventive care usage, and employee satisfaction. These numbers provide a clearer picture of whether the current plan is delivering value to both the business and its workforce.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066