- Providing world class service and value for employee benefit group plans since 1987

A health insurance subsidy would be essential in rendering healthcare accessible to millions of Americans. Such financial subsidies help individuals and families with no employer-paid plans, Medicare, or Medicaid to make ends meet in a world where healthcare costs are increasing.

This article discusses the fundamentals of health subsidies, including their nature, their beneficiaries, and their operation. It also incorporates such significant terms as medical care subsidy, health care subsidy, and healthcare subsidy. Knowing about such subsidies can make you save a lot of money, both as an individual who can find a cheap solution or a business owner seeking group insurance.

The simplest definition of a health subsidy is federal government money that assists individuals and families who qualify to pay a lesser amount for health insurance. It seeks to make health insurance schemes that individuals purchase via the Health Insurance Marketplace, typically under the Affordable Care Act (ACA), less expensive. It is the amount that will assist you in reducing your monthly premium, or the amount you have to pay; moreover, it doesn’t have to be paid monthly, as in the case of loans.

This is very favorable help to the people and families that have low income, and it ensures that these people also get proper medical attention regardless of money problems. To illustrate, a medical insurance subsidy can totally eliminate premiums to certain individuals who will enroll, or it may reduce sums of money significantly according to the money earned by the individual. It is also possible that without such assistance, many individuals would not receive the coverage they require, which would expose their health to more risk and prove more expensive in the long run.

What are health care subsidies? A health care subsidy refers to the financial assistance provided by the government to enable people to more readily obtain and access health insurance. Others are plans that reduce the price of the Marketplace plans, and others are larger plans such as Medicaid expansions or the Children’s Health Insurance Program (CHIP). They are supposed to assist people with low incomes to cover the insurance, which makes visits to doctors, time in the hospitals, and their preventive measures affordable.

Health care subsidies in the U.S. have been altered by the Affordable Care Act (ACA) and other legislation to be more affordable. To illustrate, the ACA introduced the sliding-scale assistance to seal the gaps. The Inflation Reduction Act (IRA) has temporarily increased subsidies, and this implies that the benefits are prolonged. Those benefits will, however, cease to exist after the year 2025 unless they are renewed. This is to say that additional individuals can have the opportunity to secure lower or no-premium policies by 2025.

The ACA is divided into two categories of healthcare subsidies, namely Premium Tax Credits (PTC) and Cost-Sharing Reductions (CSR). The two types address different spheres of insurance expenses:

Other subsidies are not included in the Marketplace, such as employer payments to group plans or state-specific programs. Nevertheless, individual coverage only has subsidies under the ACA.

Whether or not you will get a health insurance subsidy depends on your household income in comparison to the Federal Poverty Level (FPL), people in your family, and your other sources of income as well. Marketplace subsidies are unavailable to you in case you are incapable of receiving cheap employer-sponsored insurance, Medicare, or complete-scope Medicaid.

Overall, persons eligible to receive Premium Tax Credits have incomes ranging between 100% and 400% percent of the FPL. Nevertheless, the standards will become different starting in 2025 and provide more advantages to low-income individuals. Sharing Costs You are eligible to receive a discount provided that you earn between 100% and 250% of the federal poverty level (FPL) and you enroll in a silver plan. Medicaid is available in most states with an incomes that is below 100% of the FPL.

The following table represents the 2025 FPL regulations in the 48 contiguous states (greater in Alaska and Hawaii). These regulations are applicable in determining the people entitled to a subsidy:

| Household Size | 100% FPL | 138% FPL (Medicaid Expansion Threshold) | 250% FPL (CSR Upper Limit) | 400% FPL (Standard PTC Upper Limit) |

| 1 | $15,060 | $20,783 | $37,650 | $60,240 |

| 2 | $20,440 | $28,207 | $51,100 | $81,760 |

| 3 | $25,820 | $35,632 | $64,550 | $103,280 |

| 4 | $31,200 | $43,056 | $78,000 | $124,800 |

| 5 | $36,580 | $50,480 | $91,450 | $146,320 |

| 6 | $41,960 | $57,905 | $104,900 | $167,840 |

| 7 | $47,340 | $65,329 | $118,350 | $189,360 |

| 8 | $52,720 | $72,754 | $131,800 | $210,880 |

In case there are over eight individuals in a household, multiply the 100% FPL by $5,380 and multiply it.

To determine whether you are eligible, you can use such tools as the KFF Subsidy Calculator or enroll using HealthCare.gov.

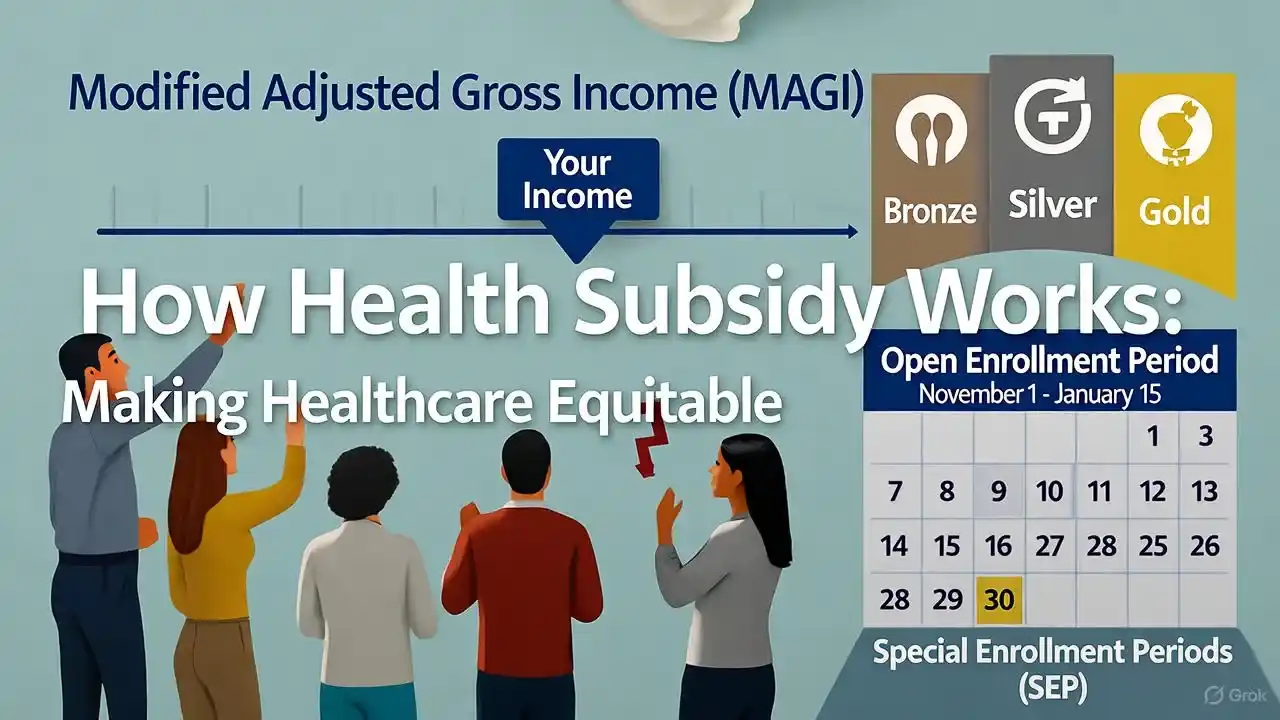

Now, let’s take a look at what is a health subsidy is, and how it works. It operates on the basis of a sliding scale in accordance with your Modified Adjusted Gross Income (MAGI). Premium Tax Credits will be paid by the government when you make contributions ranging between 0 and 8.5% of your pay to the default silver plan. This credit may be applied to any metal-level plan.

Sharing Costs With a silver plan, you are entitled to the discounts by applying them automatically. It would mean that your maximum out-of-pocket payments and copays would reduce, and you would not need to do anything to do that. You can be registered on Open Enrolment (November 1 to January 15) or Special Enrolment Periods in case of some change in your life, such as loss of employment.

In case your income varies throughout the year, inform the IRS about this so that you are not subject to paying back the taxes. Overall, these systems ensure that subsidies get adjusted according to real-life needs, and this approach contributes to making health care more equitable for all people.

A healthcare subsidy has numerous advantages:

A health subsidy refers to the government money that assists individuals who are low-income to middle-income to pay less in terms of health insurance via the Marketplace. In order to qualify, you have to earn between 100 and 400% of the federal poverty line (FPL) for a family size, and you should not possess any other affordable coverage, workplace-based plans, or Medicaid.

Similar to Premium Tax Credits, the medical insurance subsidies will restrict your premium to 0-8.5 percent of your salary, and the remainder of it will be paid by the government. You may use it in the pocket or reimburse it on your taxes on the Marketplace plans.

In case your firm provides cheap insurance (below 8.39% of revenue on self-only in 2025), you cannot be eligible to receive a Marketplace healthcare subsidy. Exceptions are to be looked at at the time of change of jobs or in Special Enrolment Periods.

You may apply during Open Enrollment or other eligible events, at HealthCare.gov or at your state’s Marketplace. Provide details regarding your income and household; subsidies will automatically be computed regarding your projected MAGI.

You are to inform the Marketplace about any changes immediately in order to have your health subsidy updated and not to pay the exceeding assistance as a tax deduction. You may need to pay taxes in case you do not earn a sufficient amount of money. And in case you indeed earn too much money, a refund can be given to you.

The companies are able to provide group health coverage to their employees. This may render them ineligible for individual subsidies, for which the premiums are tax-deductible. Firms such as Taylor Benefits assist one to get affordable plans that can complement their overall healthcare plans.

Healthcare subsidies through health insurance continue to play a significant role in making healthcare affordable. In the ACA, health care options such as medical insurance subsidies and health care subsidies enable one to pay more easily. One should keep track of the eligibility and changes due to the increased benefits that might terminate after 2025.

If you leave a job that provided health insurance, you may qualify for a special enrollment period to get a new plan and keep your subsidy. You need to report your job change and new income as soon as possible so your subsidy amount can be updated. If your new job does not offer affordable coverage, you can usually continue receiving the subsidy based on your current income and household size.

Eligibility for subsidies depends on whether employer-sponsored coverage meets affordability and minimum value standards. Coverage deemed unaffordable under federal guidelines may allow access to marketplace subsidies.

Once approved, the subsidy can be applied directly to your monthly premium, reducing the amount you pay right away. Many applicants choose to receive the credit in advance so their monthly insurance payment is lower rather than waiting to claim the benefit at tax time.

A medical insurance subsidy reduces employee costs by having employers or programs pay part of the monthly premium. This lowers out-of-pocket expenses, improves affordability, and helps more employees maintain consistent health coverage throughout the year.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066