- Providing world class service and value for employee benefit group plans since 1987

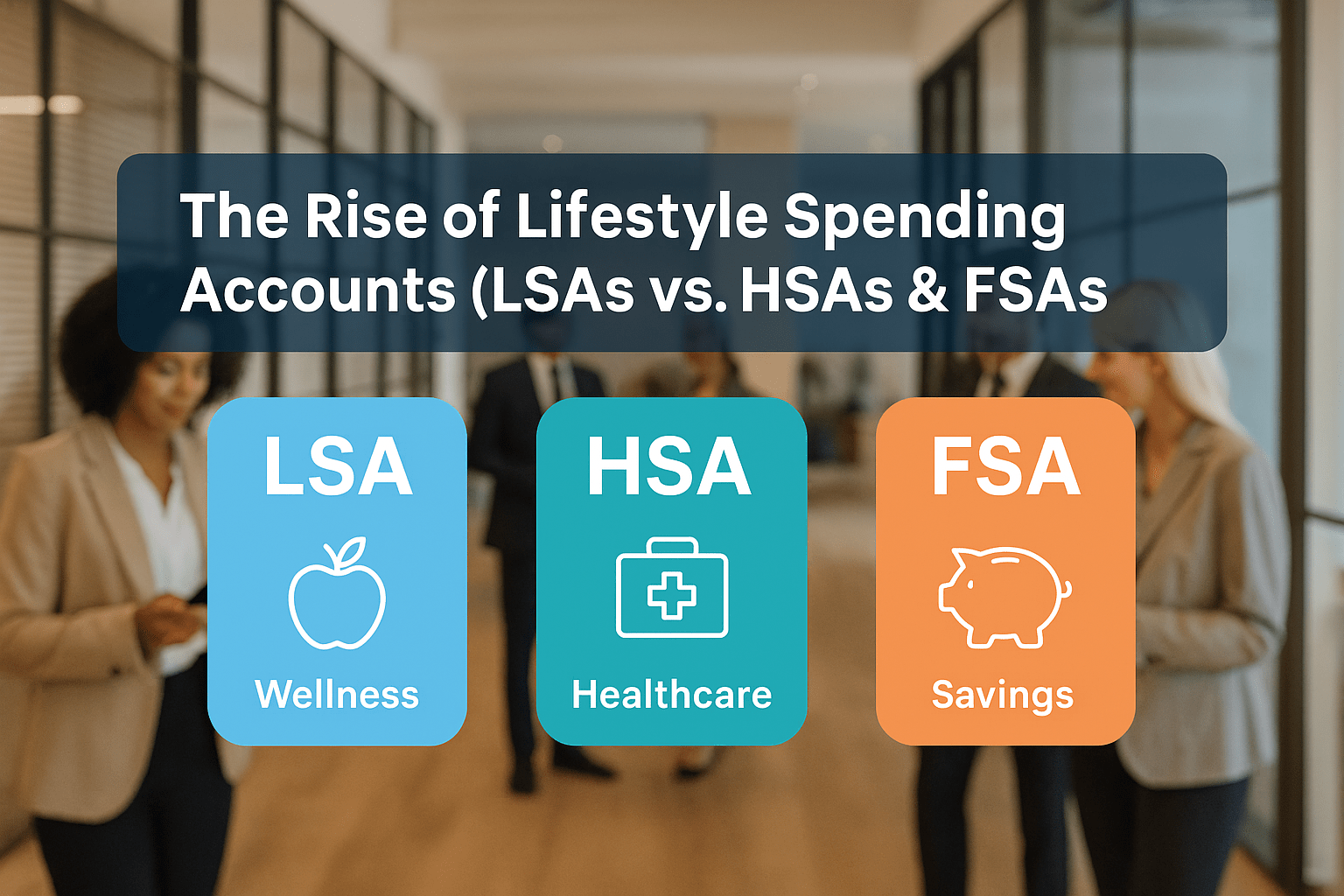

Employee benefits are rapidly evolving to meet the demands of a modern workforce. For decades, tax-advantaged accounts like Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) have been the backbone of employer-sponsored healthcare savings. But recently, a new type of perk has emerged: the Lifestyle Spending Account (LSA).

In 2025, LSAs are becoming one of the most popular ways for employers to offer flexible, personalized perks that support employee well-being beyond traditional healthcare. So how do LSAs compare to HSAs and FSAs? And which option makes sense for your business?

This guide breaks down the differences, advantages, and considerations for each type of account — and explains how Taylor Benefits Insurance Agency can help you design a benefits strategy that balances compliance, cost, and employee satisfaction.

An LSA is an employer-funded account that gives employees money to spend on lifestyle and wellness-related expenses. Unlike HSAs or FSAs, LSAs are taxable to employees, but they’re highly flexible.

Gym memberships and fitness classes

Mental health services (therapy, meditation apps, coaching)

Professional development or continuing education

Childcare or eldercare support

Nutrition programs or healthy meal delivery

Home office equipment for remote workers

Commuter or transportation costs

Why they’re trending: LSAs give employees the freedom to choose benefits that fit their unique lifestyles. Employers can set categories of eligible expenses but allow maximum flexibility.

An HSA is a tax-advantaged medical savings account available only to employees enrolled in a High-Deductible Health Plan (HDHP).

Funded by employee, employer, or both.

Triple tax advantage:

Contributions are pre-tax.

Growth is tax-free.

Withdrawals for qualified medical expenses are tax-free.

Balances roll over year to year (no “use it or lose it”).

Portable — the account stays with employees if they leave.

2025 HSA limits: $4,150 individual / $8,550 family (+$1,000 catch-up age 55+).

HSAs are powerful tools for both healthcare and long-term savings.

An FSA is an employer-sponsored account that allows employees to set aside pre-tax dollars for qualified healthcare expenses.

Funded primarily by employees (employers can contribute too).

Pre-tax contributions reduce taxable income.

Annual contribution limit for 2025: $3,300.

“Use it or lose it” — funds must generally be used within the plan year, though some plans allow a short grace period or small carryover.

Not portable — employees lose the account if they leave.

FSAs are a short-term tax savings tool but less flexible than HSAs.

| Feature | LSA | HSA | FSA |

|---|---|---|---|

| Tax Treatment | Employer contributions are taxable to employee | Contributions, growth, withdrawals all tax-free (for qualified expenses) | Contributions pre-tax; withdrawals tax-free for qualified expenses |

| Eligible Expenses | Broad (wellness, lifestyle, education, childcare, fitness) | Strictly qualified medical expenses (IRS-defined) | Strictly qualified medical expenses (IRS-defined) |

| Rollover | Employer decides | Yes, funds roll over | Limited (grace period or small carryover) |

| Portability | Employer decides (typically no) | Yes, employee owns account | No |

| Who Can Contribute | Employer only | Employer and employee | Employee (employer optional) |

| Plan Requirement | None | Must be enrolled in HDHP | None |

✅ Pros

Highly flexible, employee-driven.

Supports holistic well-being (beyond medical).

Enhances recruitment and retention, especially with Gen Z and Millennials.

Employer sets budget and eligible categories.

❌ Cons

Employer contributions are taxable income to employees.

Not tax-advantaged for employers.

Still a newer concept — may require employee education.

✅ Pros

Triple tax advantage.

Long-term savings potential (funds never expire).

Portable between jobs.

Helps employees manage high-deductible plans.

❌ Cons

Only available with HDHPs, which not all employees prefer.

Higher deductibles may discourage care.

Requires financial literacy for employees to maximize benefits.

✅ Pros

Pre-tax contributions lower taxable income.

Widely available and familiar to employees.

Employers save on payroll taxes.

❌ Cons

“Use it or lose it” rule creates risk of forfeiture.

Less flexible — only for medical, dental, and vision expenses.

Not portable if an employee leaves.

Many companies are now offering LSAs in addition to traditional tax-advantaged accounts.

Why? Because LSAs:

Appeal to younger employees who want flexible, lifestyle-oriented perks.

Enhance diversity and inclusion by meeting a broader range of needs.

Allow companies to differentiate their benefits packages in competitive industries.

For example:

A company might offer an HSA for healthcare savings, plus an LSA that covers wellness, learning, or lifestyle expenses.

Another employer may pair an FSA with an LSA stipend for home office equipment and mental health apps.

HSAs and FSAs: Governed by IRS rules, with strict compliance requirements.

LSAs: Not regulated by the IRS in the same way, giving employers flexibility — but also making employer design decisions critical.

Employers must decide:

Which expenses are eligible.

How much to contribute.

Whether funds roll over.

How accounts are administered (vendors or in-house).

At Taylor Benefits Insurance Agency, we help employers design comprehensive, modern benefits strategies that combine tax-advantaged savings with lifestyle-oriented perks. Our team supports you by:

Analyzing workforce demographics to understand which accounts make the most sense.

Negotiating with carriers and vendors to offer HSAs, FSAs, and LSAs cost-effectively.

Customizing LSA design — from eligible categories to contribution levels.

Educating employees so they understand how to maximize these benefits.

Ensuring compliance with IRS rules for HSAs/FSAs and best practices for LSA administration.

Whether you’re considering adding LSAs for the first time or need to optimize your current HSA/FSA setup, Taylor Benefits ensures your package is both competitive and sustainable.

LSAs are on the rise because they offer flexible, personalized perks that younger employees value.

HSAs remain the most powerful tax-advantaged tool for healthcare savings and retirement planning.

FSAs provide short-term tax savings but are less flexible.

Many employers are combining LSAs with HSAs or FSAs for a well-rounded strategy.

Partnering with an experienced broker like Taylor Benefits helps employers design plans that balance cost, compliance, and employee satisfaction.

The future of employee benefits is about choice and personalization. While HSAs and FSAs remain essential tax-advantaged tools, Lifestyle Spending Accounts (LSAs) are quickly becoming a powerful way to engage and support today’s diverse workforce.

At Taylor Benefits Insurance Agency, we specialize in helping businesses integrate these options into a seamless, competitive package. By offering the right mix of accounts, you can build a benefits strategy that supports every employee while strengthening your bottom line.

You can have an LSA alongside an HSA or FSA. Use the HSA or FSA first for eligible medical expenses to take advantage of tax benefits. The LSA is best for wellness and lifestyle expenses like gym memberships, mental health services, or professional development. Keep in mind that LSA contributions are usually taxable and may not roll over if unused depending on your employer’s policy. Understanding the rules for each account helps you get the most from your benefits.

Employers offering LSAs must track allocations and spending to ensure funds are used for eligible purposes, maintain transparency, and provide accurate reporting for both internal accounting and compliance purposes.

Most LSAs exclude personal loans, investments, non-health related entertainment, and general household bills. Employers provide a list of eligible expenses to ensure proper use of funds and maintain compliance.

Employees usually access LSA funds through reimbursement or prepaid benefit platforms. They pay upfront for approved expenses and submit proof for reimbursement, or use integrated systems that directly process eligible purchases for convenience and tracking.

Todd Taylor oversees most of the marketing and client administration for the agency with help of an incredible team. Todd is a seasoned benefits insurance broker with over 35 years of industry experience. As the Founder and CEO of Taylor Benefits Insurance Agency, Inc., he provides strategic consultations and high-quality support to ensure his clients’ competitive position in the market.

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066