- Providing world class service and value for employee benefit group plans since 1987

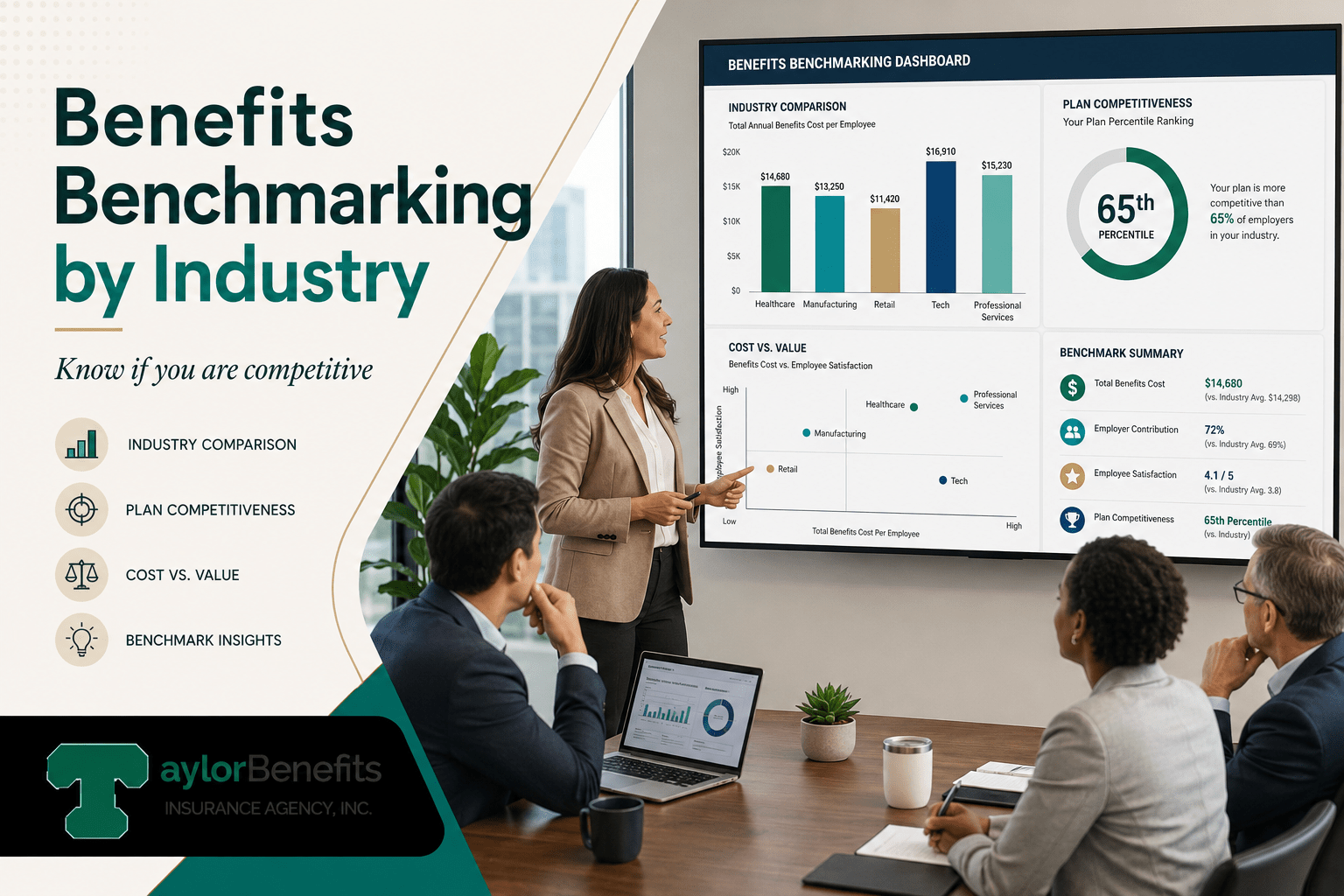

The generic benchmarking advice, 'compare to your peers, use SHRM data, survey your employees', is widely available and consistently insufficient for employers trying to answer a specific question: are our benefits competitive for the industry we're actually recruiting in?

That question requires industry-specific data, not general market averages. A healthcare employer competing for clinical talent faces different benchmarks than a software company recruiting engineers, a manufacturing firm hiring skilled trades, or a

Read Full Article Here

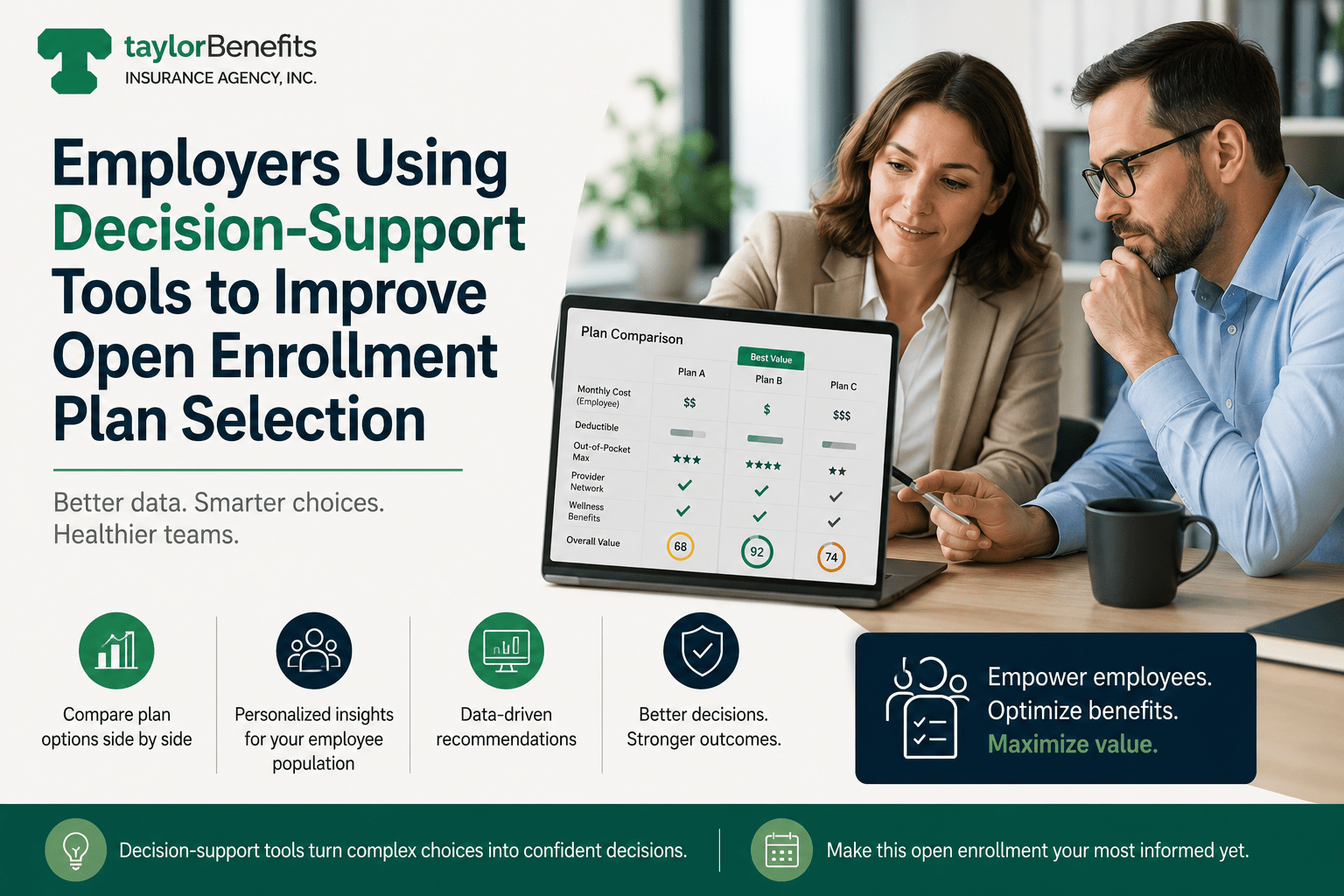

Choosing a health plan during open enrollment is one of the most consequential financial decisions employees make each year. The average annual premium for employer-sponsored family coverage has climbed to nearly $27,000, with employees now contributing approximately $6,850 out of pocket. A poor plan choice can mean thousands of dollars in unnecessary costs, limited access to the providers an employee depends on, or inadequate coverage at the moment it's most needed. Despite the stakes, most employees approach open enrollment with

Read Full Article Here

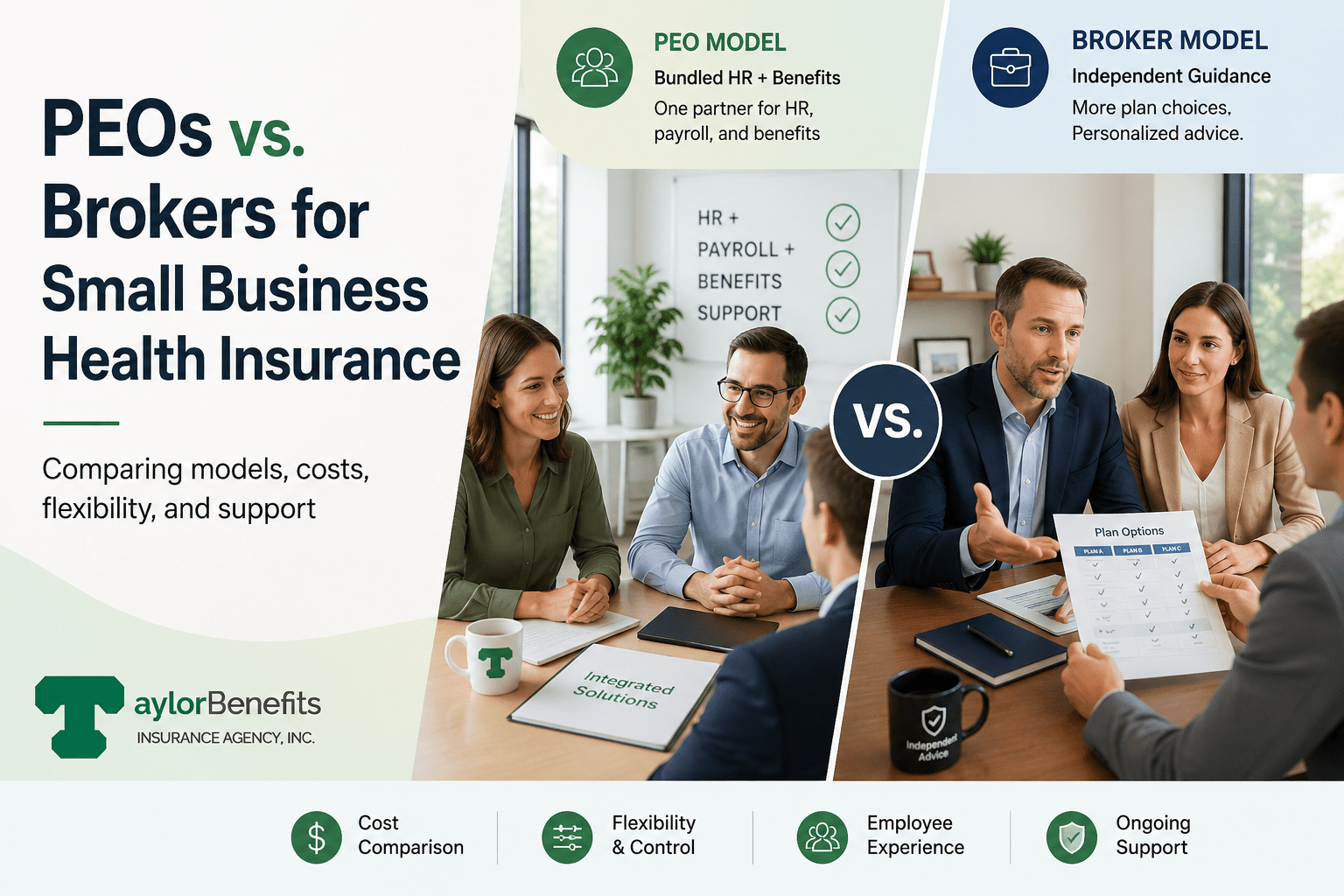

Small business owners shopping for group health insurance frequently encounter two distinct paths: working with a Professional Employer Organization (PEO) or working with an independent benefits broker. Both promise to simplify benefits for small employers. Both offer access to competitive coverage. And both are widely used.

They are, however, fundamentally different arrangements — different in how they work, what they cost, what control they give the employer, and what happens when the

Read Full Article Here

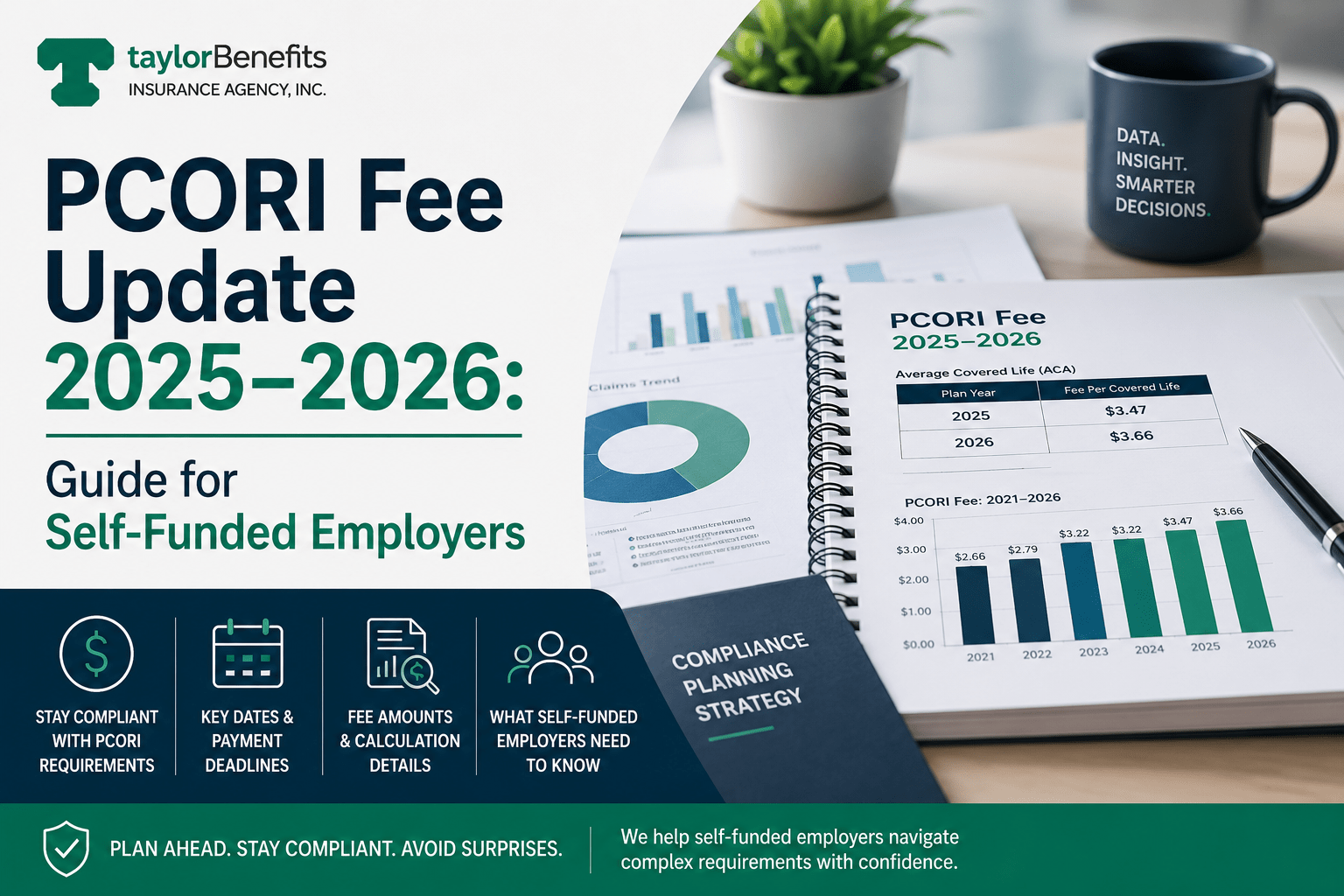

he Patient-Centered Outcomes Research Institute (PCORI) fee is one of the smaller but more consistently mishandled compliance obligations in employer-sponsored health plan administration. It applies to virtually every self-funded and level-funded group health plan, the filing mechanics are specific, the deadlines are fixed, and the fee amount adjusts annually — making it a recurring compliance item that benefits from clear annual review rather than being handled reactively.

For plan years ending on

Read Full Article Here

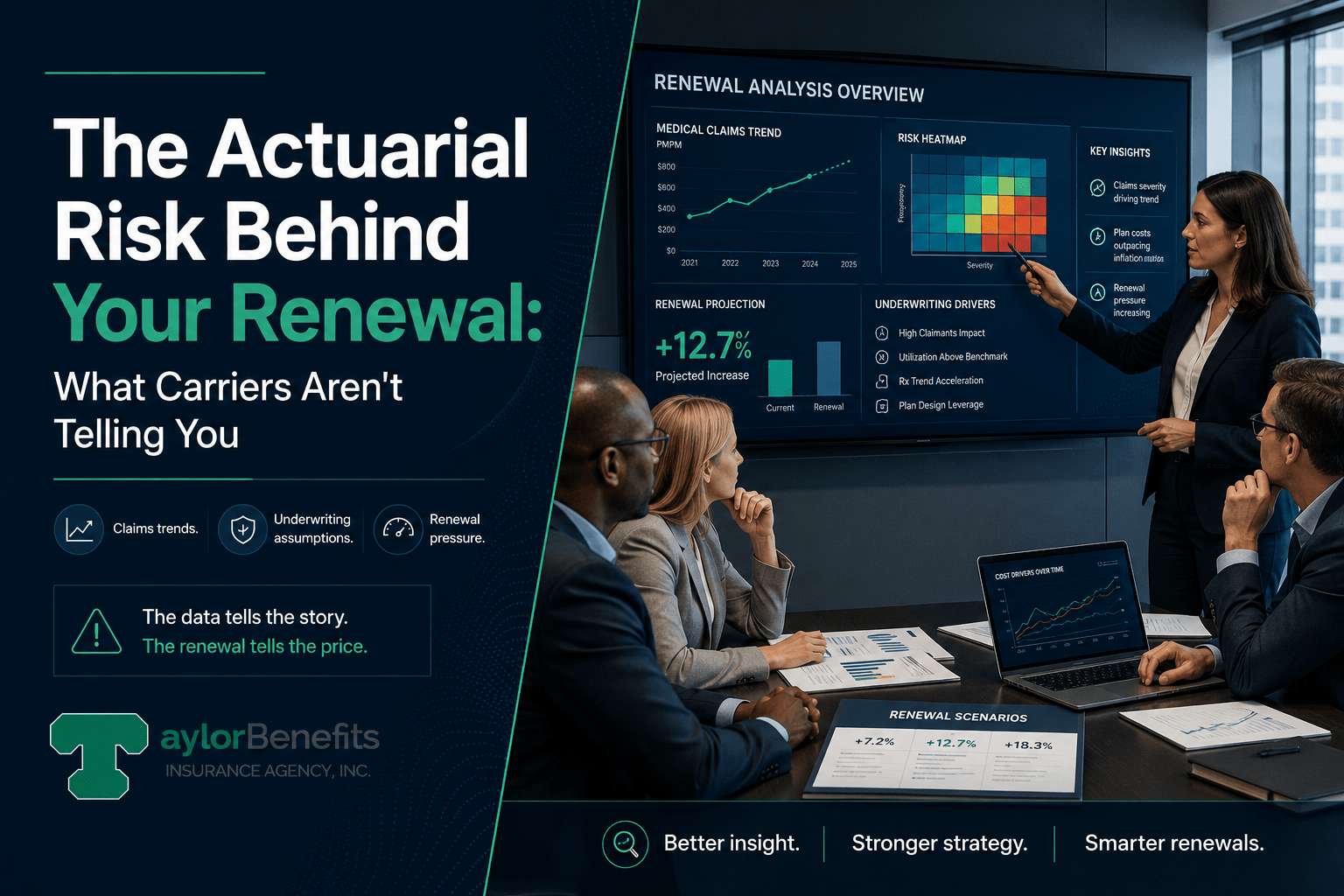

Every year, a renewal proposal arrives from the carrier or TPA. The document shows a rate increase — expressed as a percentage — alongside perhaps a brief explanation citing medical trend, claims experience, or plan adjustments. Most employers review the number, express some degree of frustration, and then proceed to negotiate within whatever margin the broker believes is available.

What most Read Full Article Here

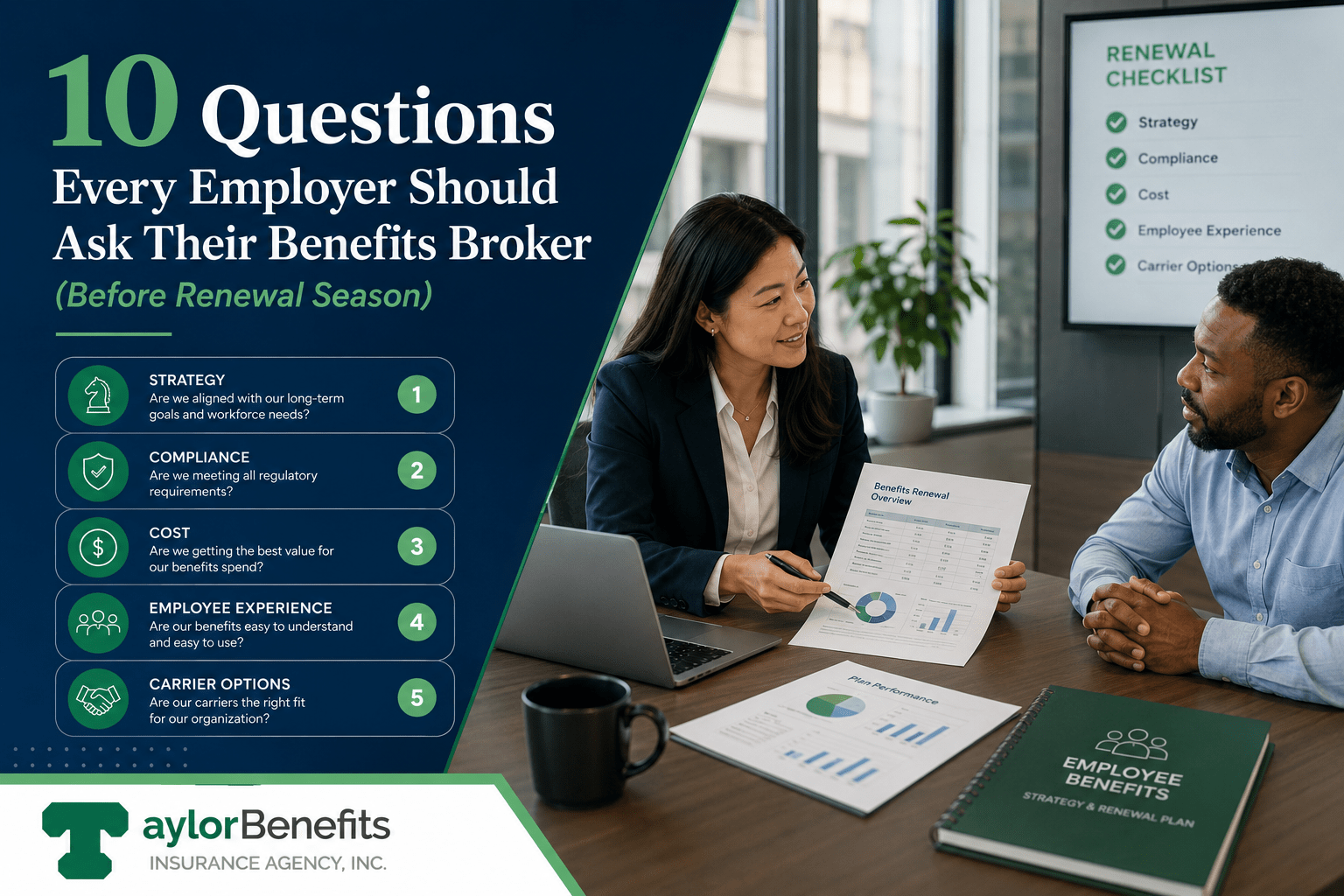

The benefits renewal conversation that most employers have with their broker is reactive: the broker presents renewal rates from the incumbent carrier, the employer asks how the rates compare to the prior year, and the conversation focuses on whether to accept the renewal or shop the market. This pattern produces predictable outcomes — modest year-over-year adjustments to a benefits program that drifts slowly from market norms, with limited strategic input beyond carrier negotiation. A more productive renewal conversation looks different.

Read Full Article Here

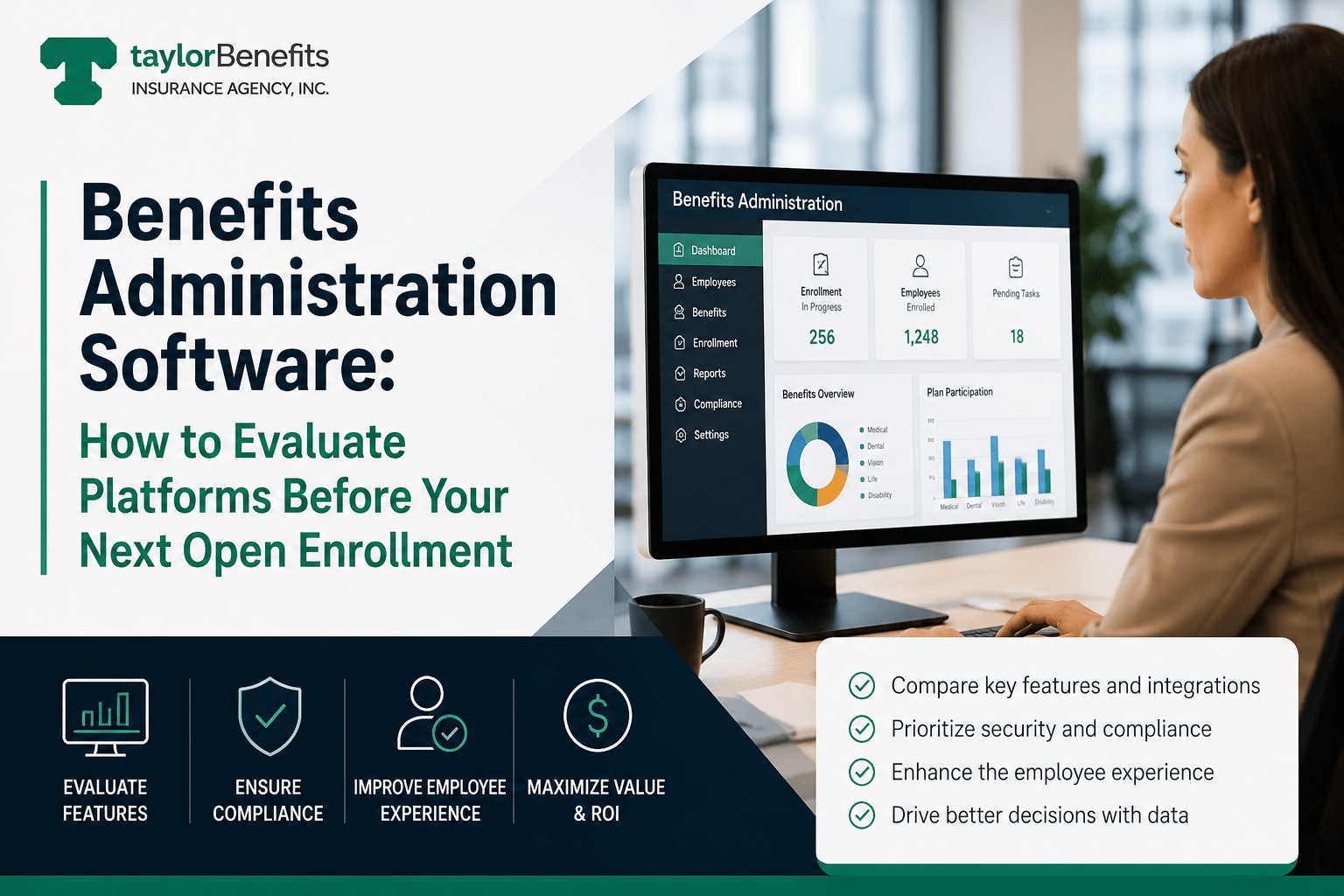

The benefits administration platform an employer chooses affects almost every dimension of how their benefits program functions: how employees enroll, how data flows to carriers, how compliance reporting is generated, how employees access plan information throughout the year, and how much administrative time the HR team spends on benefits versus other work. Despite this, many employers make benefits administration platform decisions reactively — typically in response to a carrier change, broker recommendation, or service problem with an

Read Full Article Here

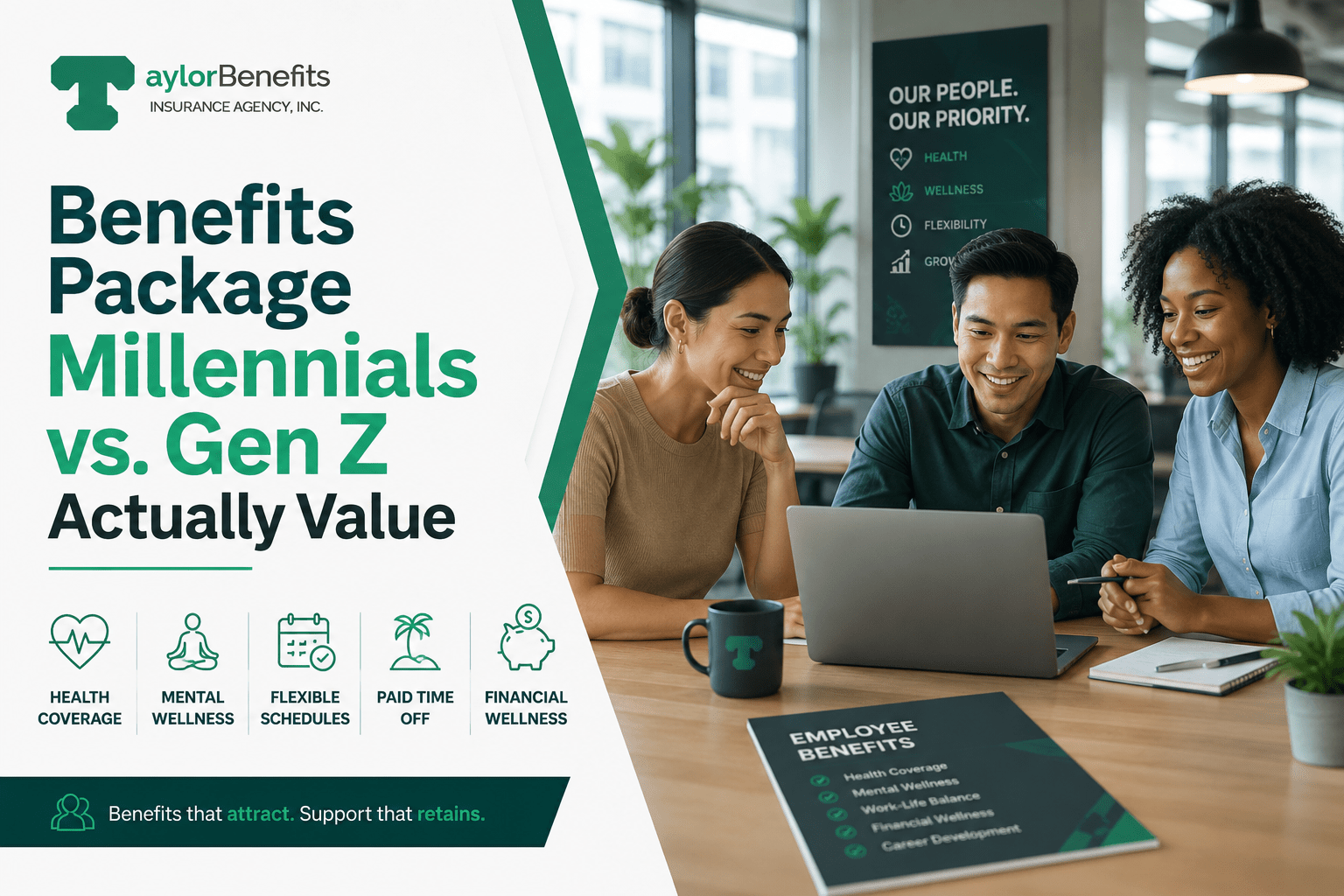

The "millennials and Gen Z want the same things" narrative that dominated employer benefits content for years is no longer accurate, if it ever was. The two generations now make up the majority of the U.S. workforce, and the differences between what each actually values from an employer benefits package have become significant enough to drive distinct design choices — particularly for employers competing for talent across both cohorts simultaneously. The differences are not about generational stereotypes or surface preferences.

Read Full Article Here

The U.S. workforce is aging. According to Bureau of Labor Statistics data, the share of workers age 55 and older has risen substantially over the past two decades and is projected to continue growing through the late 2020s and into the 2030s. Workers age 65 and older are the fastest-growing segment of the labor force in absolute terms. For many employers — particularly those in healthcare, manufacturing, professional services, education, and skilled trades — significant portions

Read Full Article Here

Most employees do not understand their employer-sponsored benefits. Research from industry sources including the International Foundation of Employee Benefit Plans, MetLife, and various academic studies has consistently found that significant percentages of employees cannot accurately define basic insurance terms like deductible, copay, coinsurance, and out-of-pocket maximum — let alone evaluate which plan option is right for their situation or how to use their benefits effectively once enrolled. The consequences of this knowledge gap are not abstract.

Read Full Article Here

We just started working with Taylor Benefits and could not be happier. Todd gave us quite the education as well as some time saving tools to help us manage our HR and save money too. We are looking forward to a long relationship!”

-Carol, Accounting Manager, recruitment marketing company, Campbell, CA

We’re ready to help! Call today: 800-903-6066